The latest PwC Deal Insights report on E&C sector shows a total value of US$12.9bn (£10.3bn) for mergers and acquision (M&A) activity with disclosed value greater than US$50m. This was 12% higher than the previous quarter and 106% higher than Q4 2015.

Deal value in 2016 was driven by activity in China, as eight of the ten largest deals throughout the year were announced by Chinese acquirers.

M&A activity remained strong in terms of deal volume and relatively stable from the perpective of value during in 2016. The year closed 4% lower than 2015 in total deal value but experienced a 23% increase in volume as buyers remained active with smaller acquisitions.

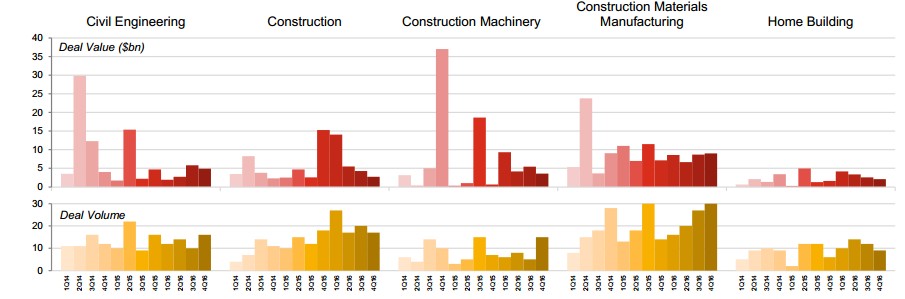

Most deal activity in 2016 was in the construction machinery and materials manufacturing categories, with notable influences from China, India and the United States. Asia & Oceania continues to be the region with the most M&A activity by volume, accounting for 62% of acquirers and 63% of targets in global transactions this year.

Moving into 2017, continued uncertainties around the globe are likely to influence M&A activity. PwC envisages more deals in the US, with potential legislation around infrastructure spend and corporate tax reform increasing interest in US assets both domestically and inbound from buyers looking for growth.

“Despite a strong US economy, there remain a number of unanswered questions around the globe, which will likely have far-reaching implications on how 2017 trends,” said Colin McIntyre, US engineering and construction deals leader at PwC.

The report says: “Carrying on trends from previous quarters, we expect E&C M&A volume to remain healthy with small and mid-sized deals, driving trends in the nearer term. We see the potential for upside in the US and select pockets around the globe but with greater uncertainty outside the US and particularly in Europe in 2017. With the US elections complete and transition of power in full swing, attention turns to the legislative agenda and what campaign speak will turn in to real policy. Two key areas of focus are the potential for meaningful US corporate tax reform and a new infrastructure spending bill in 2017, both of which we believe could further fuel both domestic and inbound M&A activity in the US.”

It continues: “Outside the US, 2017 will likely see formal notification to the European Commission (EC) of the UK’s intent to exit. This will be new territory unwinding and replacing decades of policies. The outcome of those discussions may be further influenced by the pending elections in three key European countries which are likely to not only impact the Brexit discussions, but could have an impact on the EC itself. We believe that all of this uncertainty is likely to continue to influence M&A activity and have far-reaching consequences that will play out in 2017 and beyond.”

In Q4 2016, M&A activity continued a trend seen all year: strength in small to medium-sized deals (reflected in a 23% increase in deal volume) with relatively flat (4% decrease) value.

Total deal value for deals with disclosed value greater than US$50m decreased by 4.5% in 2016.

The E&C sector saw 305 deals in 2016, 22% higher than 2015.

Deal volume increased by 18% in Q4 2016, to 87 deals. This is the fourth consecutive quarter with an increase in volume, indicating a positive trend.

Deal value in 2016 was primarily driven by China Vanke’s acquisition of Shenzhen Metro, a US$10.8 bn transaction.

The construction materials manufacturing category saw the highest deal value in Q4 2016 with 30% of the total deal value of the sector. The category also shows growing interest, as volumes have doubled in the last four quarters.

The construction and construction machinery categories followed closely with 24% and 21% respectively, however, volumes and value were relatively steady in these categories in 2016.

Got a story? Email news@theconstructionindex.co.uk