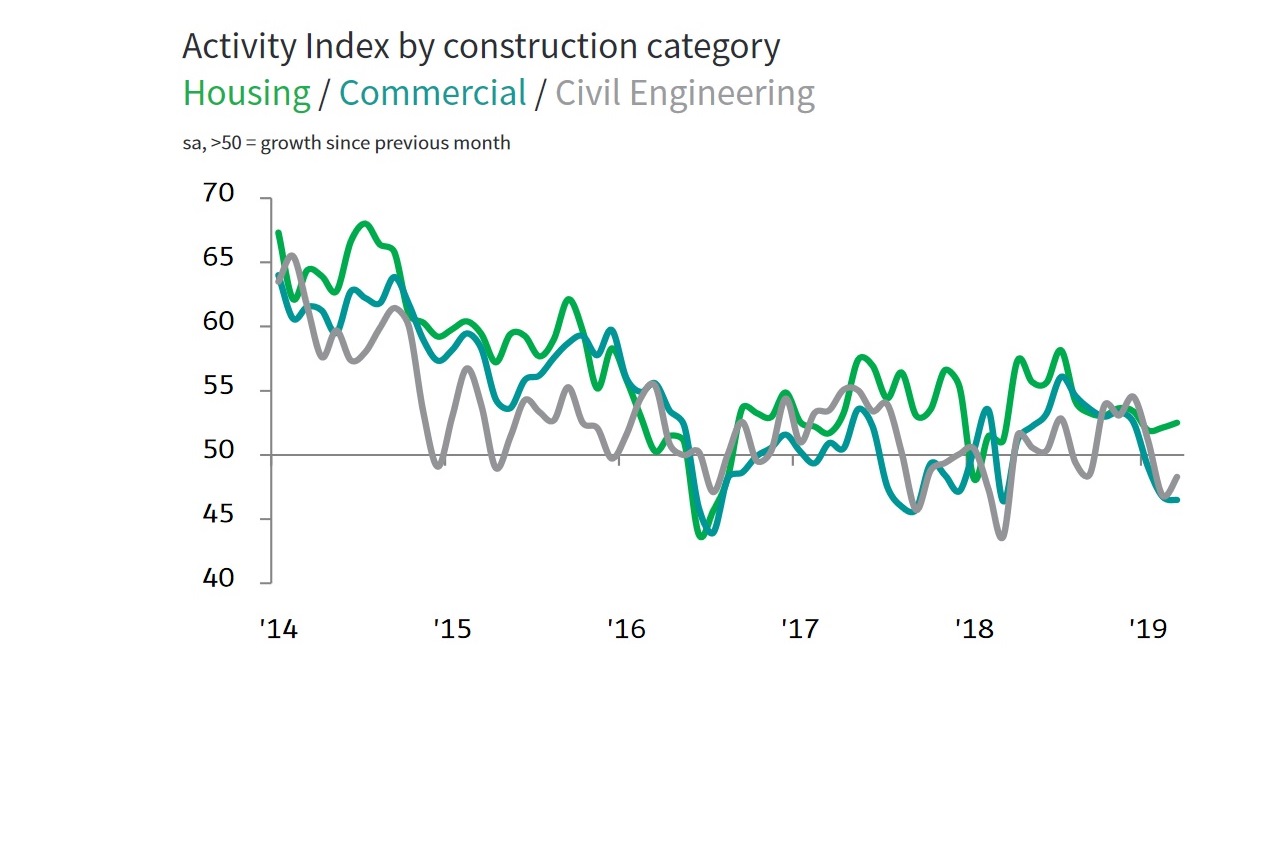

While house-builders were a little busier than they had been in February, this was not enough to offset the effects of a further slowing in commercial work and civil engineering activity.

As the first quarter of 2019 came to end, new business and employment numbers increased only a little, suggesting subdued underlying demand and delays to decision-making among clients.

That is the analysis of the economists who put together the monthly survey of construction industry purchasing managers.

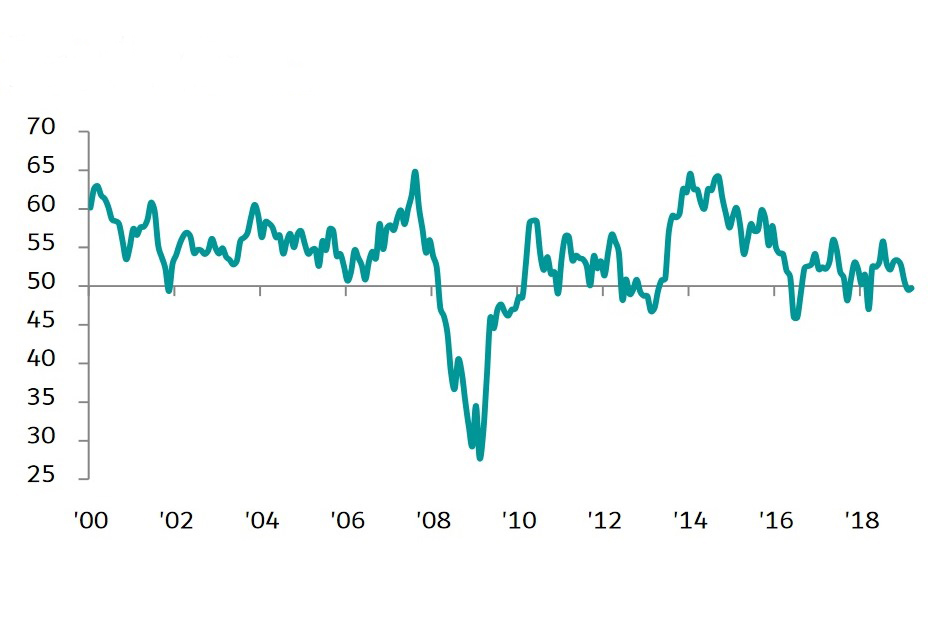

Adjusted for seasonal influences, the headline IHS Markit/CIPS UK construction total activity index (what used to be called the PMI or purchasing managers’ index) for March 2019 posted 49.7. This was up fractionally from 49.5 in February but still below the 50.0 no-change threshold.

The sustained decline in total construction activity represented the first back-to-back fall in output levels since August 2016, although the rate of decline remained only marginal in March.

Commercial construction was the worst performing area during the latest survey period, with business activity dropping to the greatest extent since March 2018. There were widespread reports that Brexit uncertainty and concerns about the domestic economic outlook had led to risk aversion among clients. Civil engineering activity also fell in March, although the rate of decline eased since February.

Residential building once again bucked the downward trend seen across the wider construction sector in March. The latest upturn in housing activity was only modest, but still the strongest seen so far in 2019.

March data revealed a marginal increase in new work received by UK construction companies, with the rate of expansion remaining subdued in comparison to the long-run survey average. Survey respondents commented on intense competition for new work and a reluctance among clients to commit to major spending decisions in March. Mirroring the trend for new orders, latest data also highlighted only a modest rise in staffing levels at UK construction companies.

Input buying rebounded slightly in March, followed a decline during the previous survey period. Some firms commented on stock building efforts as part of their Brexit preparations, which helped to boost purchasing activity. Meanwhile, suppliers' delivery times lengthened markedly in March, which survey respondents attributed to low stocks and stretched capacity among vendors.

Average cost burdens increased at a sharp and accelerated pace during March. The rate of input price inflation was the fastest since November 2018. Higher raw material costs were attributed to the weak sterling exchange rate and, in some cases, shortages of available items among regular suppliers.

Meanwhile, business optimism edged up from the four-month low seen during February. However, the degree of positivity remained much weaker than the long-term survey average. A number of construction companies noted that economic and political uncertainty had weighed on business expectations for the next 12 months.

Joe Hayes, an economist at IHS Markit, which compiles the survey, said: “Fears that the recent weakness of the UK construction sector may not be just a blip, but a sustained soft patch, were further fuelled by latest data. Amid subdued inflows of new work, a first back-to-back decline in output since August 2016 was recorded. Brexit-related uncertainty continued to generate indecisiveness, ultimately hitting order book volumes. Strong competition for contracts was also reported by some [survey] panel members. The outlook was subsequently underwhelming by historical standards, with the unsettled political and economic environment keeping business confidence below its long-run average.

"Nevertheless, UK construction businesses ramped up their purchases of materials and other inputs, reflecting efforts to build safety stocks ahead of any potential Brexit-related disruptions. As such, supply chain constraints persisted and average input lead times lengthened once again."

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, which sponsors the survey, added: “The situation in the UK construction sector was broadly unchanged from February, with PMI data posting a second consecutive month in contraction. The fault of this continuing inertia was placed squarely at the feet of Brexit.

"Not a small rise in job creation, optimism and new orders, nor resilient house building, were enough to buck the underlying downward trend in a sector suffering from client hesitation and consumer gloom. There was also intense competition from other sectors, with the stockpiling of supplies increasing delivery times again and creating raw material shortages, all adding to the pressures. Given the lack of warehousing space in the UK and the difficulties of storing bulky items, it is evident the sector has pressed the panic button in its attempt to keep projects moving during the political impasse.

"It is unlikely that next month will bring about any positive news given the challenges of a weaker UK economy, volatile pound and intense competition for new orders, as Brexit continues to cast a long shadow over the sector’s future."

Brendan Sharkey, head of construction and real estate at MHA MacIntyre Hudson, said that London’s housing market had so far taken the worst of the Brexit headwind.

“The general feeling is of an industry ticking along, with enough business to get by but with no immediate prospects of growth,” he said. “London’s stagnating housing market is feeling the Brexit chill more than the provinces. The capital’s rental market has declined and the day-to-day competition that drives a flourishing housing market has gone. In contrast Birmingham and Manchester are faring considerably better. Brexit will only bite those areas after it actually happens.

“The collapse of Interserve does not threaten the industry in the same way as Carillion’s demise. However, there is not much sign other players are moving away from the low-profit high-turnover model that lies behind Interserve’s fall. Balfour Beatty is still leading the way in showing you can make money out of construction.

“The industry needs a stimulus in the form of some big projects from the government; currently it is getting by on the tailwind provided by Hinkley Point and the Elizabeth line but it is to be hoped the pipeline fills up once Brexit is out of the way.”

Got a story? Email news@theconstructionindex.co.uk