.png)

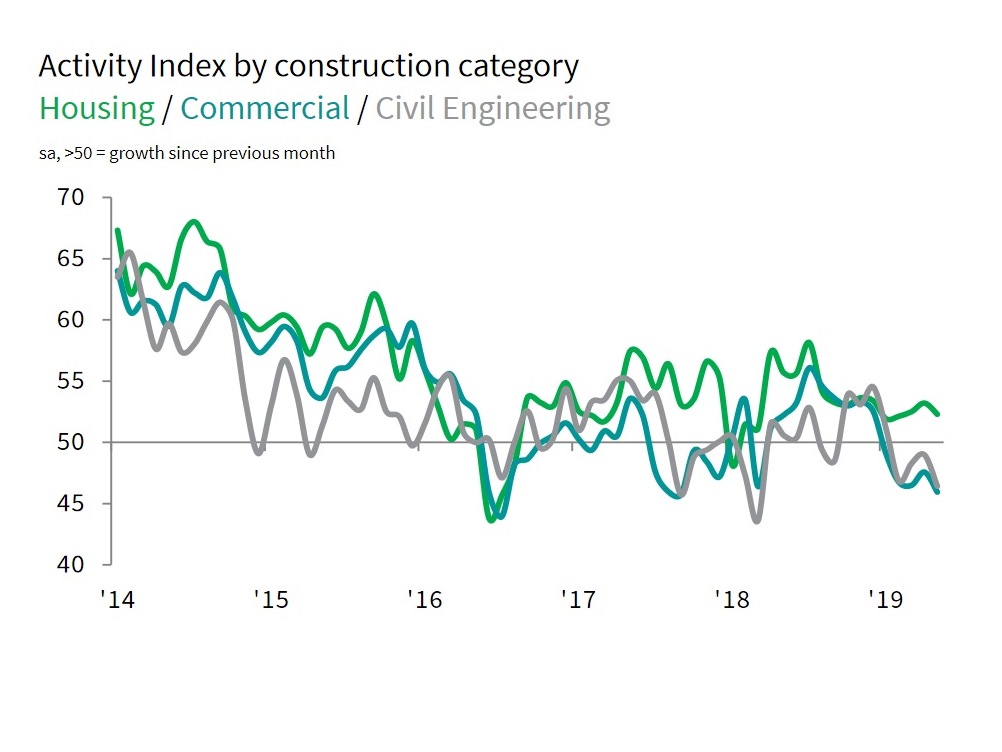

Only house-builders saw any growth in May, according to the latest monthly survey of construction purchasing managers but this was not enough to offset the industry-wide impacts of lower volumes of commercial work and civil engineering activity.

New orders also decreased across the construction sector, with survey respondents noting that subdued domestic economic conditions had led to project delays and fewer tender opportunities.

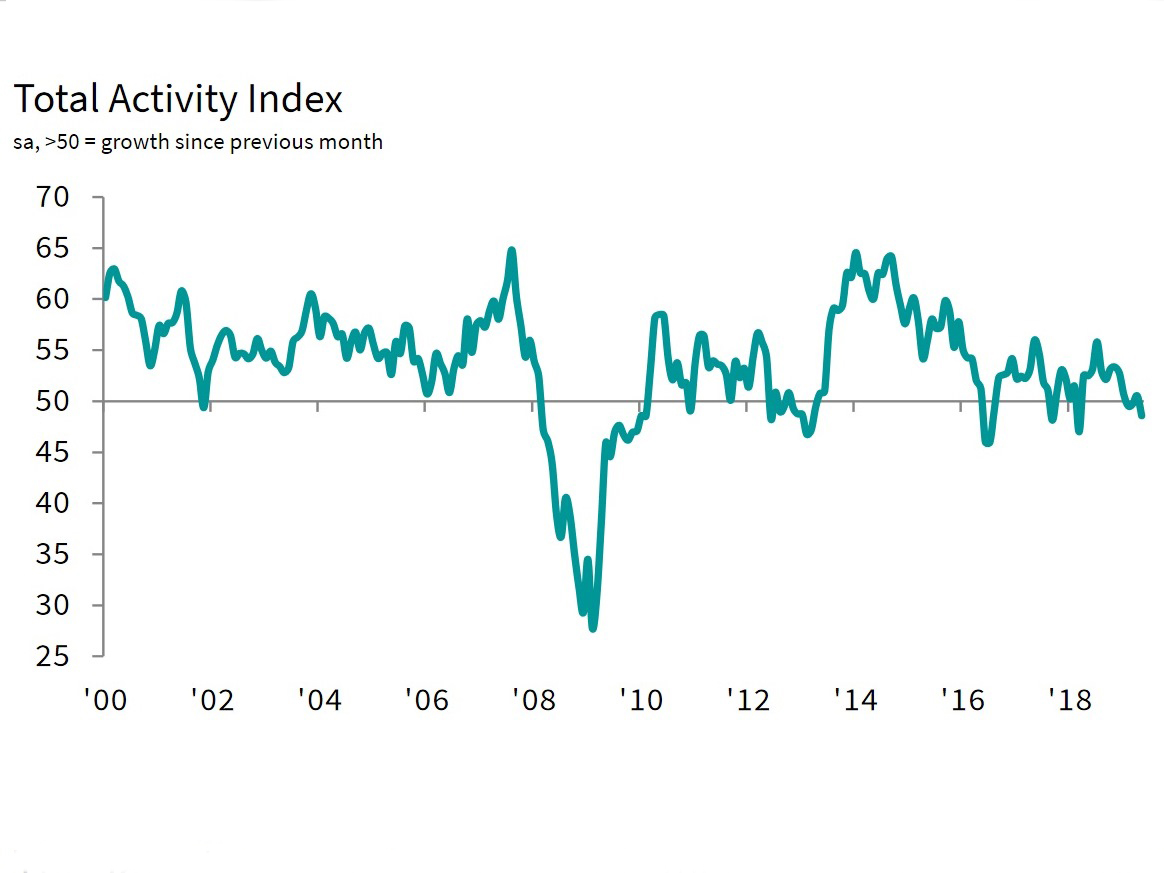

At 48.6 in May, down from 50.5 in April, the headline seasonally adjusted

IHS Markit/CIPS UK Construction Total Activity Index (what used to be known as the purchasing managers index, or PMI) registered below the 50.0 no-change mark for the third time in the past four months. The latest reading was the lowest since the snow-related downturn in construction output during March 2018.

Commercial building was the weakest area of construction activity in May, with output falling to the greatest extent since September 2017. Survey respondents widely commented that clients had opted to hold back on major spending decisions in response to Brexit uncertainty and concerns about the economic outlook.

May data also revealed a decline in civil engineering activity for the fourth consecutive month. Construction companies cited constrained client budgets and a headwind from domestic political uncertainty.

Residential work continued to expand in May, albeit at the weakest pace for three months. Higher levels of house building have been recorded in each month since February 2018.

The latest survey pointed to a modest reduction in new orders received by UK construction companies, with the rate of decline the steepest since March 2018. Construction companies reported strong competition, hesitancy among clients and longer sales conversion periods, largely reflecting subdued demand conditions in May.

Reduced workloads led to more cautious recruitment strategies and the non-replacement of departing staff in May. As a result, the latest survey pointed to the sharpest drop in construction employment for six-and-a-half years.

Construction companies reported another decline in their purchasing activity. Although only marginal, the latest reduction was the largest since September 2017. Supply chain pressures persisted in May, which led to another sharp lengthening of average lead times among vendors. There were a number of reports citing low stocks and shortages of materials (particularly plasterboard).

Although fuel and energy costs pushed up average input prices, the overall rate of input price inflation eased to its softest since June 2016.

Meanwhile, construction firms signalled a fall in business optimism to its weakest since October 2018. Survey respondents widely cited concerns that domestic political and economic uncertainty would dampen business activity growth over the next 12 months.

Economist Tim Moore, associate director at IHS Markit, which compiles the survey, said: “May data reveals another setback for the UK construction sector as output and new orders both declined to the greatest extent since the first quarter of 2018. Survey respondents attributed lower workloads to ongoing political and economic uncertainty, which has led to widespread delays with spending decisions and encouraged risk aversion among clients.

"Commercial building remained hardest-hit by Brexit uncertainty, with construction firms reporting the steepest fall in this category of activity since September 2017. Civil engineering work also dried up in May and a fourth consecutive monthly fall in activity marked the longest period of decline since the first half of 2013. Construction companies often commented that recent tender opportunities for civil engineering work had been insufficient to replace completed projects.

"House building was the only sub-category of construction output to buck the downward trend in May, but growth remained softer than on average in 2018.

"The soft patch for construction work so far this year has started to impact on staff hiring, with some firms cutting back on expansion plans and others opting to delay the replacement of voluntary leavers. May data revealed that the latest fall in employment numbers was the steepest for six-and-a-half years. Survey respondents once again noted concerns that the subdued domestic economic outlook and delays related to Brexit uncertainty had curtailed their near-term growth prospects."

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, which sponsors the survey, said: “A fragile dreariness descended on the sector this month with lower workloads leading to the fastest decline in purchasing of construction materials since September 2017. With the continuing uncertainty around Brexit and instabilities in the UK economy, client indecision affected new orders which fell at their fastest since March 2018 and particularly affected commercial activity.

"The previously unshakeable housing sector barely kept its head above water, growing at its weakest level since February as residential building started to lose momentum. The biggest shock however, came in the form of job creation as hesitancy to hire resulted in the largest drop in employment for six and a half years. Not much to be happy about it seems though an easing in some input costs for raw materials offered some relief while energy and fuel prices continued to rise.

"This is unlikely to be nearly enough to turn around the sector’s fortunes, as optimism about the strength of the sector’s future was the lowest since October 2018. Policymakers will need to pull a large rabbit out of the hat, and fast, to improve these difficult conditions and prevent a further entrenchment of gloom and contraction this summer."

Blane Perrotton, managing director of the surveyors Naismiths, said: “The weekend heatwave made no impact on the construction industry, which is still frozen in a bitter winter. Not since March 2018, when subzero temperatures froze many construction projects to a halt, has output slid this quickly.

“Apart from a brief flurry of stockpiling in advance of March 29th – what should have been Brexit Day – many in the industry have had a pretty wretched start to the year. There is precious little to cheer in this altogether bleak PMI report. New orders, confidence levels and recruitment are all down. Housebuilders have managed to keep growing, just. But their modest expansion in output has been dwarfed by the declines in commercial property and infrastructure building.

“While the residential sector is stoically grinding on, the industry as a whole is running to stand still. With investor confidence being pummelled by a double whammy of Brexit and political uncertainty, what work there is dominated by the completion of existing projects rather than new ones. Britain’s army of smaller residential developers provides one of the few bright spots. Fuelled by lenders who are still keen to offer finance, the smaller scale players have no choice but to keep building, even if their margins are being squeezed by rising material costs and slow sales. Despite some green shoots elsewhere in the economy, on this evidence the climate in the construction industry remains stuck in the Ice Age.”

Jonathan White, UK head of infrastructure, building and construction at KPMG, said: “A dip in PMI reading is symptomatic of the cloud of uncertainty currently enveloping the sector. The steady stream of infrastructure work across the UK had strengthened order books – and buoyed confidence – but there is a clear sense that the market is slowing down in the commercial sector as the Brexit impasse puts a halt on decision-making.

“The problem is that when the industry struggles, its structural issues become even more evident. Operating margins are still stubbornly low and this makes the investment needed to improve productivity even less likely. Meanwhile, the sector continues to rely heavily on housebuilding to drive growth. The hope is that the forthcoming Infrastructure Finance Review, for which the consultation closes later this week, will offer some clarity on how to finance the projects that will feed contractors’ pipelines in the future.”

Got a story? Email news@theconstructionindex.co.uk