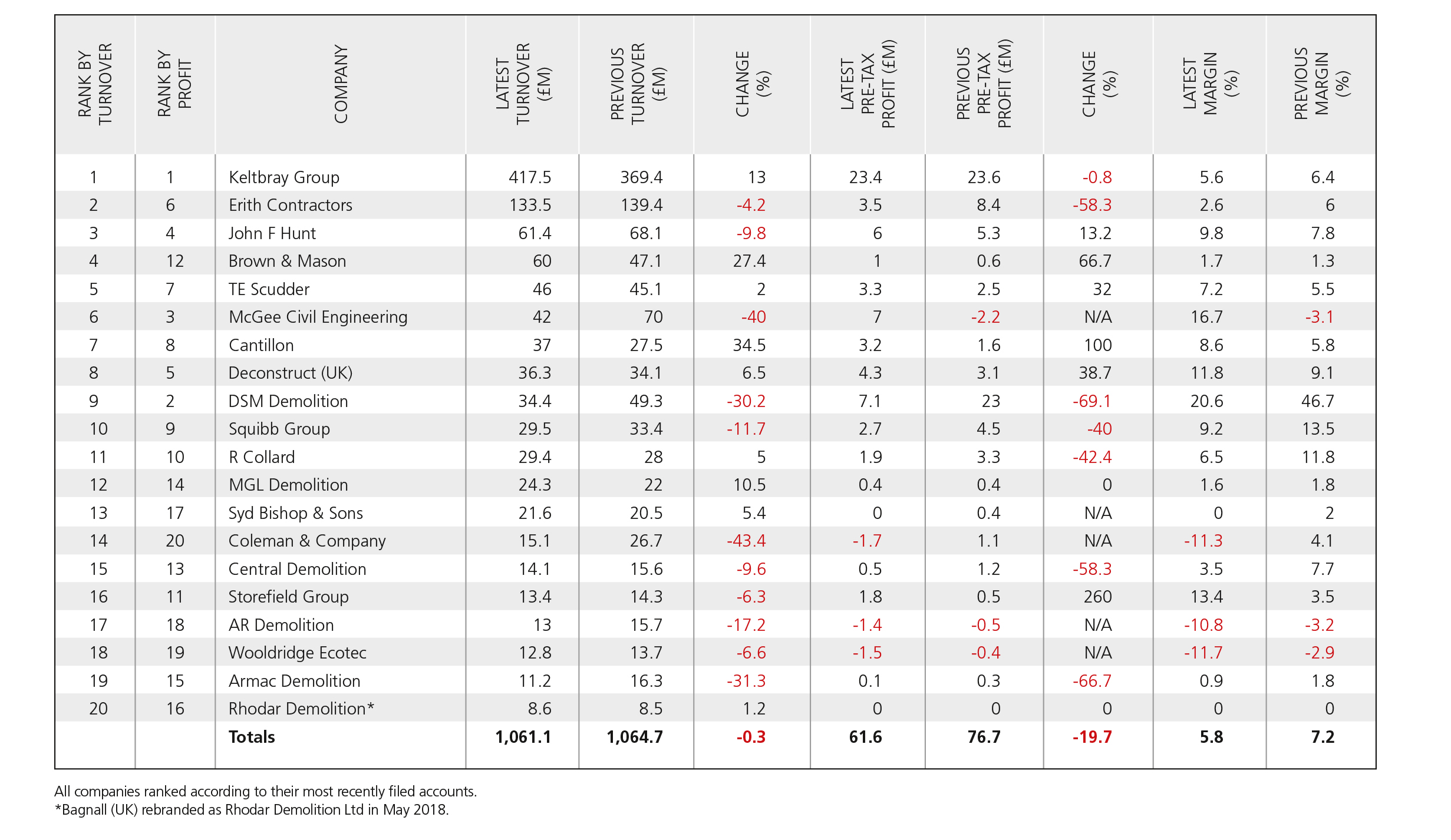

This time last year, the UK demolition industry was riding the crest of an economic wave. Combined revenues of the top 20 specialists in the sector grew almost 30% in 2016/17 and broke through the £1bn barrier for the first time. Pre-tax profits surged more than 70% on average. It was the second consecutive year of vigorous growth.

But this year’s picture is a very different one. Everything appears to be on the slide: total turnover for the same 20 contractors has levelled off at just over £1bn. And overall pre-tax profits have plummeted by almost 20%, from £76.7m to £61.6m.

Eleven of the top 20 demolition specialists have reported a decline in turnover in their most recent results and seven have seen pre-tax profits fall. Average margin has fallen from 7.2% to 5.8%.

Our snapshot of the demolition sector is in line with a more detailed analysis, published in January by market research specialist Plimsoll, which showed that 106 of the UK’s 433 largest demolition companies are “in danger” while 99 are making a loss. Although 174 have increased their value, 68 have lost over a quarter of their value in the past year according to Plimsoll.

“As a further sign of the intense competition within the UK industry, 37 companies continue to sell at a loss for the second year running,” said the Plimsoll report.

“These serial loss-makers are adding to the congestion in the market, often undercutting the rest of the market and driving down profit margins across the board,” it added. “The next 12 months represents something of a crossroads for these companies as they face two distinct choices: either they operate more responsibly or they run out of cash.”

Keltbray remains the largest player in the market as well as one of the more stable. In the year to November 2017, the company’s turnover breached the £400m barrier for the first time. Pre-tax profit remained about the same, with the result that its margin dropped a percentage point to 5.6%.

Most of Keltbray’s 2017 growth came from its specialist contracting division – encompassing demolition, structural and geotechnical engineering, concrete and temporary works – which saw turnover grow from £269.4m to £311m.

The company says that its success here is due in large part to clients’ increasing desire to engage contractors capable of delivering a broad range of complementary services in-house.

Keltbray forecasts a reduction in turnover by the specialist contracting division in the year to 31st October 2018 due to a “slowing-down in new early-works opportunities”. However, it hopes this will be offset to some extent by more activity in its reinforced concrete frame business.

Other strong performers during 2017/18 include Brown & Mason, up two places to the number four position on the table this year, and Cantillon – also up two places.

Both companies recorded a solid increase in both turnover and pre-tax profits last year. Cantillon, rather like Keltbray, attributes this to the ability to offer an integrated turnkey service of complementary skills, combining demolition with groundworks, substructure and superstructure construction.

Managing director Paul Cluskey said the business has “a strong pipeline [of work] for 2019-2020 as well as a significant workload ongoing”. He added that Cantillon is “well-placed to win and deliver significant works for the coming 12 months and beyond”. Cantillon grew turnover almost 35%, from £27.5m to £37m, in the 12 months to 30th June 2018 and doubled its pre-tax profits from £1.6m to £3.2m.

Brown & Mason turned over £60m in the year to May 2018, more than 27% more than the previous year. Pre-tax profit was also up, though at £1m it represents a very slender margin of just 1.7%.

The company’s directors acknowledge that margins are very low and say that this “highlights the ongoing pressures to manage costs and resources effectively and prudently on multi-year customer contracts”. Cashflow is a priority for the company.

Earlier this year, figures published by industry body BuildUK, a signatory to the Construction Supply Chain Payment Charter which set a 30-day payment target, revealed that Brown & Mason is its slowest-paying member, averaging 103 days.

Few of the leading demolition specialists are doing as well as these two companies, and several are doing much worse.

Coleman & Company has suffered particularly badly since the Didcot tragedy three years ago and continues to pay the price. The company ran up a pre-tax loss of £1.7m last year, partly due to ongoing exceptional costs of £348,000 related to the Didcot disaster.

This is only the second time in 56 years of trading that Coleman & Company has fallen into the red; the previous occasion was a result of the 2008 global financial crisis.

But it says it has also been hit by the ever-present Brexit uncertainty which “has impacted in the marketplace generally”. More specifically, two major contracts worth in excess of £11m and originally earmarked for a 2017 start were delayed and will only now get underway this year.

Coleman’s turnover in the year ended 30th April 2018 was down more than 43% to £15.1m (2017: £26.7m) which not only affected gross profit but also put a squeeze on margins as the company tried to hang onto market share.

“Actions to stem the losses and reduce overheads had been delayed in the optimistic belief that the pipeline contract opportunities would materialise,” said the company. “This did not happen in the desired timescale.”

After the appointment of a new group managing director, James Howard, in February 2018, plans were put in place to close certain loss-making recycling operations and “take out £600,000 overheads in a top-to-bottom restructure which the company hopes will underpin a return to profitability”.

Another contractor to file less-than-sparkling results for the year to January 2018 was AR Demolition. In its annual report the company said that 2017 was a “very challenging year” which resulted in a loss of £1.4m before tax.

The firm’s directors were further unsettled when it emerged that “material errors” had been made in previous financial reports which had to be re-stated and which resulted in a further loss of £748,711.

The company said that its misfortune was the consequence of four significantly loss-making jobs and two hefty bad debts.

A knock-on effect of the mis-reported financial situation was that certain investment decisions had been made based on wrong information and were not as beneficial to the business as had been believed.

In late 2017, once the true financial picture had emerged, AR Demolition’s directors embarked on a programme of restructuring and brought in specialists to help them turn the business around. The result has been a “dramatic” improvement in performance, says managing director Richard Dolman.

“Loss-making jobs have been concluded and the negotiation around the bad debt positions finalised,” he said. “Today the directors are very pleased with the progress made and the resulting financial picture.”

While 2017 had been a struggle, Dolman said that AR Demolition had seen a “record first six months” to 2018. The appointment of a new finance director and a new commercial director had “delivered a significant improvement in every aspect” of the business.

“Turnover for the first half of 2018 is at a record level and the company is today profitable,” commented Dolman.

Surprisingly (and with the exception of Coleman & Company) few demolition specialists seem to be unduly troubled by the ongoing Brexit debacle. Cantillon acknowledges that it has potential to disrupt the sector, describing it as “a new and unprecedented challenge”. But it adds that it “hasn’t to date impacted the flow of work”.

It’s hard to imagine that they’ll be saying that this time next year.

This article was first published in the April 2019 issue of The Construction Index magazine

UK readers can have their own copy of the magazine, in real paper, posted through their letterbox each month by taking out an annual subscription for just £50 a year. Click for details.

Got a story? Email news@theconstructionindex.co.uk