.png)

That is one of the conclusions of the latest monthly survey of construction purchasing managers by IHS Markit and the Chartered Institute of Procurement & Supply.

The December 2016 survey reveals a positive end to the year, led by the fastest rise in new order volumes since January 2016. Stronger demand resulted in sustained job creation and a broad-based upturn in business during the month. However, the sector continued to endure rising costs as suppliers passed on higher imported raw material prices. The latest rise in overall input costs was the steepest for just over five-and-a-half years.

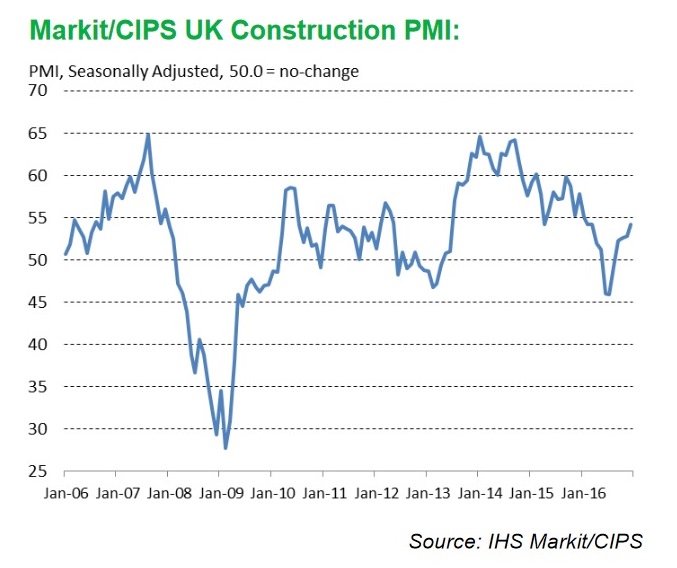

The seasonally adjusted construction purchasing managers’ index (PMI) reached 54.2 in December, up from 52.8 in November, indicating “a robust and accelerated expansion of overall construction output” according to the survey authors. The headline index has now posted above the 50.0 no-change mark for four months running, and the latest reading signalled the fastest pace of expansion since March 2016.

Anecdotal evidence suggested that improving order books and a general rebound in business conditions had helped to lift construction output in December.

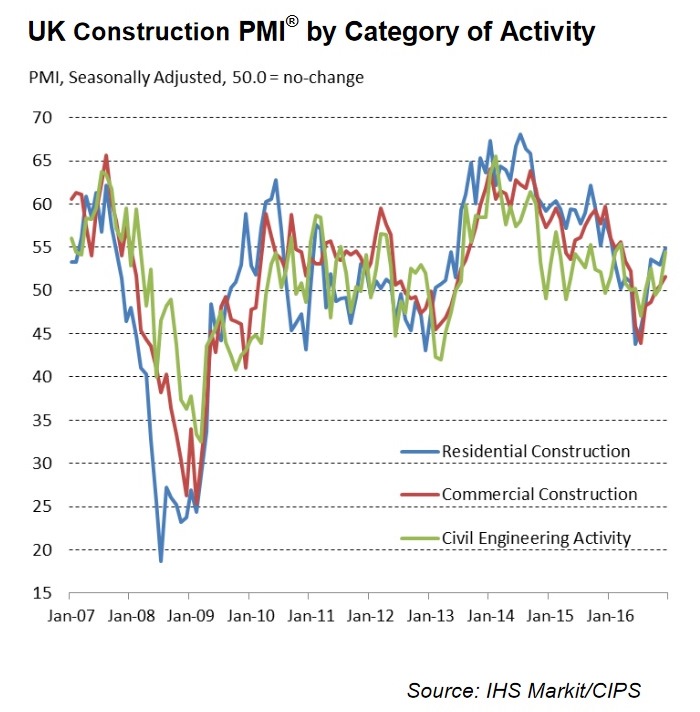

Residential building activity remained the best performing sub-category at the end of 2016 and the expansion of housing activity was the fastest since the first month of the year. Work on civil engineering projects also picked up in December, while commercial construction increased marginally.

New business volumes expanded at the strongest rate for 11 months in December, which marked a sustained recovery from the soft patch seen in mid-2016. Reports from survey respondents cited rising client demand and a resilient economic backdrop.

Greater workloads encouraged a further solid increase in staff recruitment across the construction sector. The latest rise in employment was the fastest since May, but still much weaker than seen on average since the jobs rebound began in mid-2013.

December data indicated that exchange rate depreciation continued to drive up input prices across the UK construction sector. The latest increase in average cost burdens was the fastest since April 2011. At the same time, supplier lead-times continued to lengthen, with the latest survey pointing to the most marked deterioration in vendor performance since June 2015. Some construction firms noted that forward purchasing had resulted in low stocks among suppliers.

Meanwhile, construction companies reported a reasonably upbeat assessment for their growth prospects in 2017. 48% of the survey panel anticipate a rise in business activity during 2017, while only 13% forecast a reduction.

This degree of business confidence edged up to a three-month high during December, with a number of construction firms citing optimism that strong order books would help alleviate Brexit-related turbulence in 2017.

.png)

Tim Moore, senior economist at IHS Markit, said: “December’s survey data confirmed a solid rebound in UK construction output during the final quarter of 2016. All three main areas of construction activity have started to recover from last summer’s soft patch, but in each case growth remains much weaker than the cyclical peaks seen in 2014.

“Housebuilding remains a key engine of growth for the construction sector, with the latest upturn the fastest for almost one year. Meanwhile, commercial activity was the weakest performing category in December, reflecting an ongoing drag from subdued investment spending and heightened economic uncertainty.

“The main negative development in December was a sustained acceleration in input cost inflation to its strongest since 2011. UK construction companies noted that the weaker sterling exchange rate had resulted in higher costs for a wide range of imported materials, while some also reported that forward purchasing of inputs had led to depleted stocks among suppliers.”

David Noble, chief executive of the Chartered Institute of Procurement & Supply, said: “The residential sector raced ahead this month, with the fastest pace of growth since January 2016. Strong pipelines of new work were reported across all sub-sectors, and construction firms showed improved confidence after the impacts of uncertainty around the EU referendum.

“Prices continued on their upward inflationary trajectory, at the strongest rate for five and a half years. In response, firms have increased their stock buying to not only fulfil new orders, but also to counteract anticipated price increases throughout the year, as inflationary pressures are set to continue and the weakness of the pound persists. Stock levels at suppliers were also under pressure, as vendor performance deteriorated to the greatest extent since June 2015.

“With these more resilient economic conditions, the sector also reported the fastest pace of job creation since May 2016, as companies developed their workforces to meet new projects.

“In the short-term at least, the sector looks set to enjoy these improved demand conditions for the coming months, which is positive news after many months of instability.”

However, Paul Trigg, construction specialist and assistant head of risk underwriting at trade credit insurer Euler Hermes, pointed out that Brexit hadn’t actually happened yet…

“Business confidence across construction remains high. But the industry is yet to feel the full brunt of Brexit and there are concerns the current work pipeline will only carry contractors in the short-term,” he said.

“Residential and civil engineering should remain buoyant heading into 2017, but we expect the fall in GDP growth to hit commercial property hardest. Plummeting levels of foreign direct investment are expected to curb office development, which will hurt contractors as competition ramps up and squeezes low industry margins even further. Pressure on cashflow will inevitably impact companies’ ability to pay on time across the supply chain and construction businesses will need to be extra careful when managing their credit books.”

Got a story? Email news@theconstructionindex.co.uk