The latest monthly survey of construction purchasing managers confirms that the UK construction sector remained on a strong recovery path in May 2021, with output growth reaching its strongest since September 2014. Moreover, new order volumes increased at the fastest pace since the survey began more than 24 years ago.

Input cost inflation was also at a survey-record high during May, attributed to a surge in demand for construction materials that suppliers are increasingly struggling to meet.

At 64.2 in May, up from 61.6 in April, the seasonally adjusted IHS Markit/CIPS UK Construction PMI Total Activity Index registered above the 50.0 no-change value for the fourth consecutive month and signalled the strongest rate of output growth for nearly seven years.

House-building, scoring 66.3, was the best-performing category of construction activity in May, followed by commercial work at 64.4. The latest increase in work on commercial projects was the steepest since August 2007, reflecting strong demand conditions following the reopening of customer-facing areas of the UK economy after the latest Covid-19 lockdown.

Civil engineering activity (at 61.3) also increased sharply during May, although the pace of expansion was a little slower than in April.

The latest survey pointed to a rapid upturn in new business across the construction sector. Around 47% of the survey panel reported higher volumes of new work, while only 11% signalled a reduction. Construction companies attributed the surge in order books to strong demand for residential building work and high levels of confidence about the near-term economic outlook, the survey authors said.

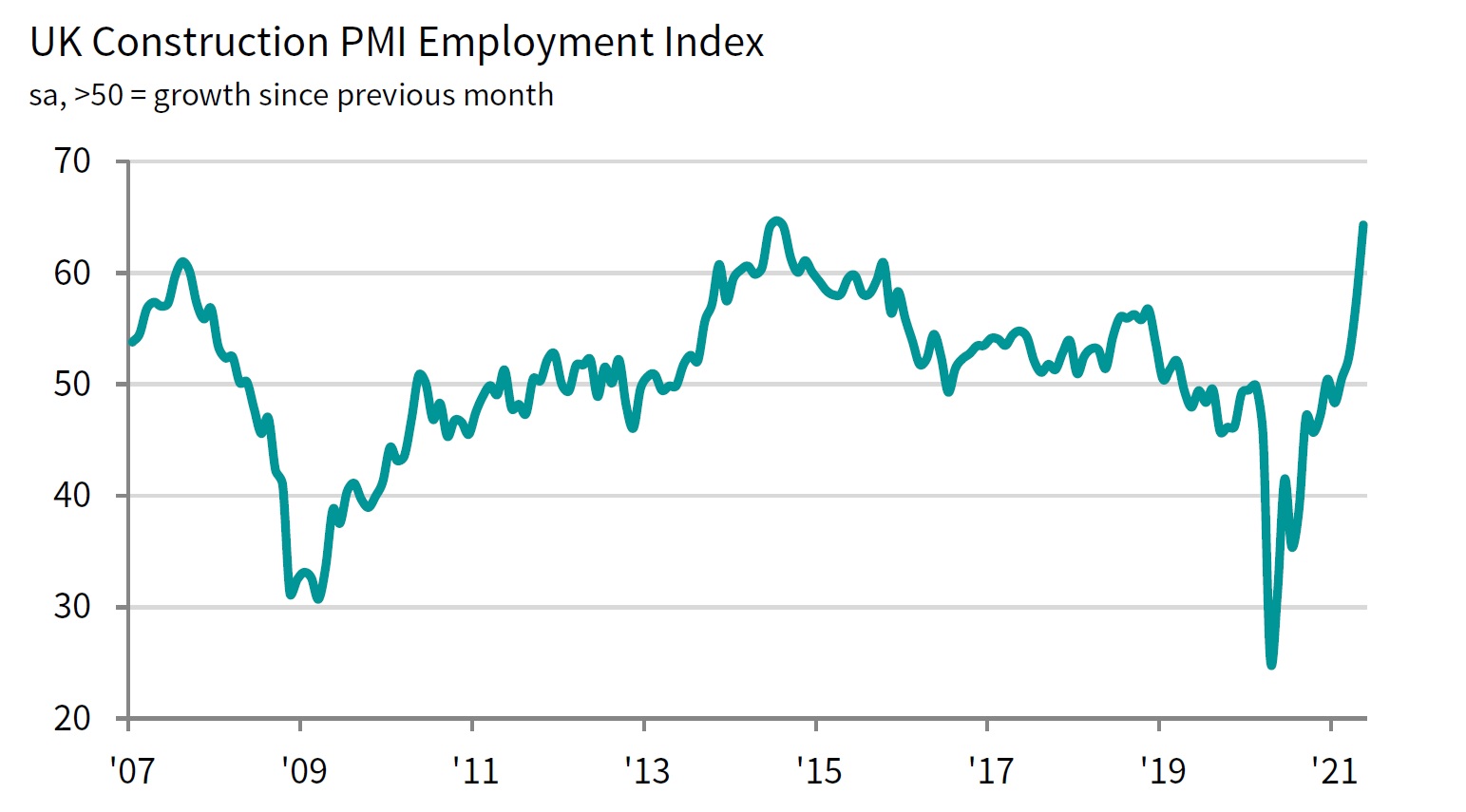

New project starts and a sustained recovery in construction workloads resulted in another marked rise in staffing numbers during May. The rate of job creation was the fastest since July 2014. Moreover, subcontractor usage increased at a pace not seen this century.

Mirroring the trend for order books, latest data indicated a steep upturn in purchasing activity across the construction sector. Some firms also noted that input buying had been boosted by efforts to build inventories in response to supply shortages.

Suppliers' delivery times lengthened sharply in May, with the downturn in vendor performance the second-steepest since the survey began (exceeded only by that seen in April 2020). Stretched supply chains and steep rises in raw material prices contributed to a rapid increase in average cost burdens.

Around 61% of the survey panel predict a rise in business activity, while just 8% anticipate a decline. Positive sentiment was mostly attributed to resurgent customer demand, alongside optimism about the UK economic outlook following the vaccine roll out.

Tim Moore, economics director at IHS Markit, which compiles the survey, said: "UK construction companies reported another month of rapid output growth amid a surge in residential work and the fastest rise in commercial building since August 2007. Total new orders increased at the strongest rate since the survey began more than two decades ago, but supply chains once again struggled to keep pace with the rebound in demand.

"There were widespread reports citing shortages of construction materials and wait times from suppliers lengthened considerably in comparison to those seen during April. Imbalanced supply and demand led to survey-record increases in both purchasing prices and rates charged by sub-contractors.

"Despite severe challenges with materials availability, construction firms remain highly upbeat about their near-term growth prospects. Nearly two-thirds of the survey panel forecast an increase in output during the year ahead, while only one-in-thirteen forecast a decline."

.png)

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, said: "The construction sector continued its expansion programme with a phenomenal acceleration in growth and the strongest for seven years as new orders filled in at the fastest rate for almost a quarter of a century.

"Busy purchasing managers were under pressure to keep up and buying up at the fastest rate since April 1997, changing sourcing strategies to find depleting essential materials and stocking up just as supply chain problems continued to mount along with prices. With inflation for goods and raw materials at a 24-year high, companies will be concerned that much-needed profits will be eaten away as building projects take shape and could be held up by some of the longest delivery times on record.”

Brian Berry, chief executive of the Federation of Master Builders, commented: “Rising material prices are continuing to limit the ability of local builders to build back better from the pandemic. It’s incredibly worrying to hear that the overall rate of input price inflation was the highest on record. This is consistent with FMB State of Trade data that shows 93% of builders reported material price increases in Q1 of this year. Against the backdrop of high levels of inquiries for building work, it’s imperative that smaller businesses have the same access to materials as the larger firms during these difficult times.”

Fraser Johns, finance director at construction contractor Beard, said: “The headline figures tell a great story about the construction sector’s recovery, which suggests a rapid rise in new business and orders at the highest level since 1997.

“It’s clearly very welcome to be talking up prospects and seeing the trends going in the right direction, but there has to be a reality check taken as the ongoing crisis in materials shortages threatens to undermine the fast-paced recovery we’re seeing.

“Supply chains are stretched like never before as the drop in factory output across Europe due to the coronavirus is really biting into delivery times, coupled with the ongoing difficulties at our ports due to Brexit.

“Confidence is returning to the economy and customers are forging ahead with plans that have been put on hold, our own head of work reflects the buoyancy of the market in that sense. But in order to keep confidence high, contractors must work smart and take a collaborative approach with suppliers and customers, to mitigate for the long lead-in times. Strong relationships with suppliers all the way down the line are going to be crucial to get through what is likely to be a difficult second half of the year in terms of the materials issue.”

Brendan Sharkey, head of construction and real estate at surveyors MHA MacIntyre Hudson, worried that the construction sector might be in a bubble, with strong but temporary demand, looming prices rises and the imminent end of some government support. He said: “Today’s PMI shows that demand in the construction sector remains strong and everyone has plenty of work. However, in truth many developers would prefer a steadier, slower recovery. This heated market is accompanied with the spectre of a coming bust to end the boom.

“A bust is far from being a foregone conclusion but it is a danger to watch out for. Hopefully the sector will have a softer landing and we will just see the housing market quieten down, possibly by September, rather than crash and burn.

“One potential pitfall comes from demand. With the current stamp duty land tax (SDLT) holiday reducing at the end of June, and with some of the current interest in moving house perhaps liable to fade away as the country reopens, demand could start to stutter.

“The other potential problem is inflation and the rising costs of construction materials, such as timber, cement and plasterboard. Some firms might not have priced this into their current contracts and could be caught out. They might think they have taken on lots of work only to find it is not actually profitable, an easy mistake to make in an industry that usually operates on thin margins at the best of times. The bigger firms are liable to weather this much better than smaller contractors, as they usually have better contracts and more influence with suppliers.

“Land scarcity is also a related problem. Getting viable land at the right price for smaller building ventures is becoming more of a problem, and might be another snare for smaller developers. Overall we’re in strange times and it is exuberant periods of expansion like this that test the industry as much as the downturns.”

Got a story? Email news@theconstructionindex.co.uk