The monthly survey of construction purchasing managers for July 2019 also revealed a sharp drop in new order intakes, which survey respondents attributed mainly to a sluggish economy and political uncertainty.

This weaker demand was coupled with a business optimism falling to its lowest ebb since November 2012.

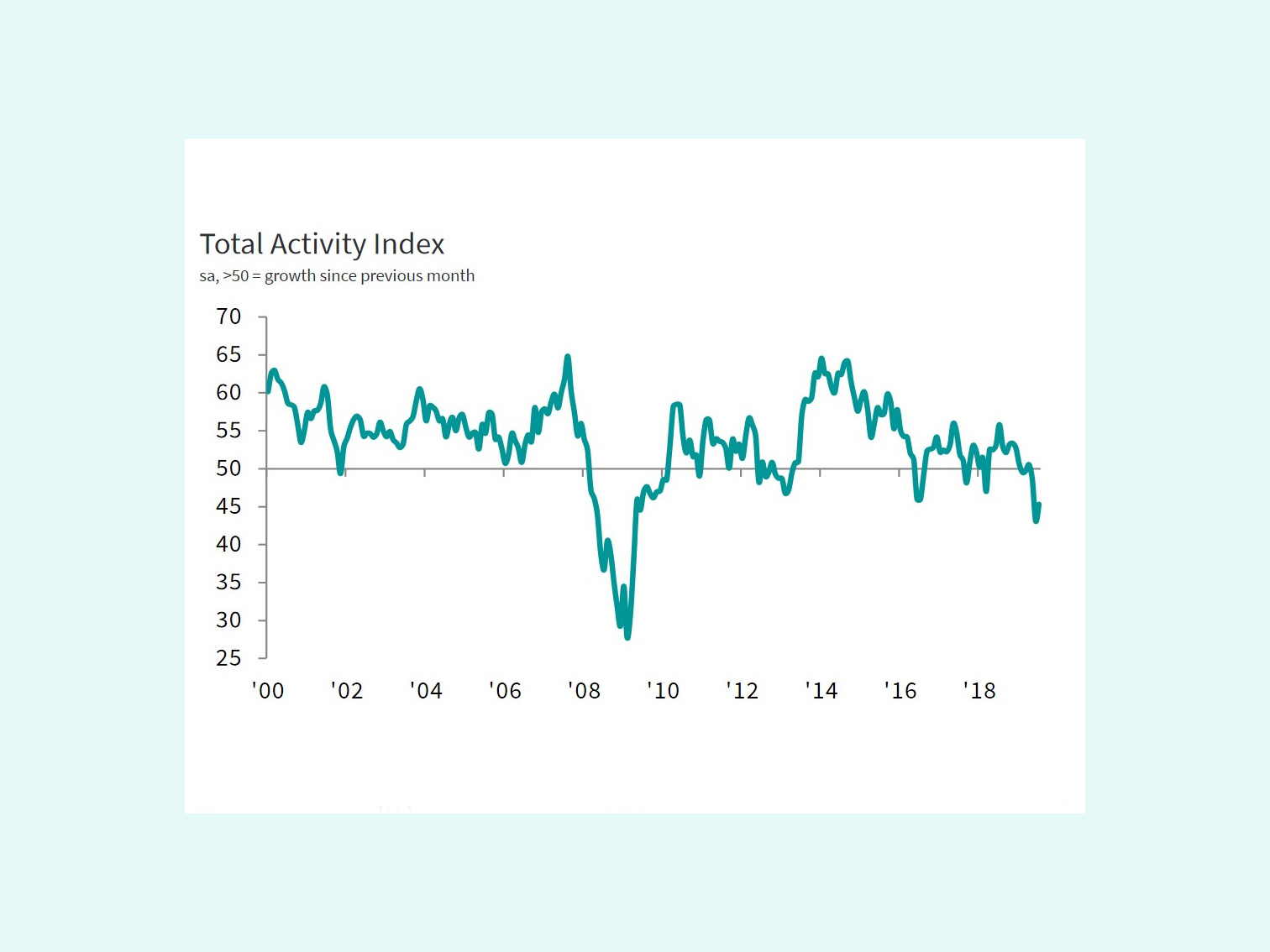

At 45.3 in July, the headline seasonally adjusted IHS Markit/CIPS UK Construction Total Activity Index posted below the 50.0 no-change value for the fifth time in the past six months. The latest reading was up from June's 10-year low of 43.1 but still indicated a clear downturn in total construction activity.

Commercial construction was the worst performing category in July, followed closely by civil engineering activity. Anecdotal evidence suggested that risk aversion among clients in response to Brexit uncertainty continued to hold back work on commercial projects. At the same time, some survey respondents noted that delays to contract awards for infrastructure work had acted as a headwind to civil engineering activity, the survey compilers said.

House-building fell for the second month in a row during July, although the rate of decline was only modest and eased from the three-year record low seen in June.

Total order books across the construction sector fell for the fourth successive month, which is the longest continuous period of decline recorded by IHS Markit since 2016. Lower volumes of new business were often linked to a lack of tender opportunities amid weaker domestic economic conditions and ongoing political uncertainty.

Employment numbers were cut back in response to deteriorating order books, although the rate of job shedding was only modest and largely reflected the non-replacement of voluntary leavers. Subcontractor usage decreased for the sixth consecutive month.

Demand for construction products and materials continued to soften, as signalled by a solid drop in purchasing activity during July. This helped to alleviate some of the pressure on supplier capacity, with lead times lengthening to the smallest extent since September 2016. With the diminished value of the pound, the increased cost of imported building products contributed to input cost inflation persisted. Shortages of certain materials, such as insulation and plasterboard, also contributed.

Tim Moore, economics associate director at IHS Markit, which compiles the survey, said: “UK construction output remains on a downward trajectory and another sharp drop in new orders has reduced the likelihood of a turnaround in the coming months.

"Total business activity declined at a softer pace than the ten-year record seen in June, but this should not detract attention from the challenges ahead for the construction sector. Customer demand has been squeezed on all sides in recent months, which has pushed down business expectations to the lowest since the second half of 2012.

"July data revealed declines in house building, commercial work and civil engineering, with all three areas suffering to some degree from domestic political uncertainty and delayed decision-making. "Construction companies have started to respond to lower workloads by cutting back on input buying, staffing numbers and sub-contractor usage. If the current speed of construction sector retrenchment is sustained, it will soon ripple through the supply chain and spillovers to other parts of the UK economy will quickly become apparent."

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, which sponsors the monthly survey, added: “The sector felt the pressure of challenging economic conditions and the impact of another disastrous drop in demand growth, as purchasing activity petered out and Brexit nibbled away at confidence and decision-making. Though the sector’s activity improved marginally on last month’s biggest fall in a decade, this third month of contraction in a row makes for gloomy reading.

“Cost pressures continued in July as the weak pound and short supply pushed up the price of materials and made progress on building projects more difficult still. In this turbulent month the impact was felt along all the supply chain with job seekers left out in the cold as employment opportunities dried up and hiring plans were frozen.

“Moving into the second half of the year it will take the sector some time to dig its way out of this deep hole. As the autumn and the potential negative impacts of a no-deal exit from the EU threaten, any significant recovery is unlikely to be on the horizon until 2020. Construction optimism is at its lowest since November 2012, so there’s no time to lose in injecting some stability and certainty into the economy and Brexit plans before a recovery of months turns into years.”

Blane Perrotton, managing director of the surveyors Naismiths, said: “Total construction activity is now only sliding rather than plunging. But behind the headline figure, the industry’s dashboard is blazing with warning lights. New orders are falling sharply, and order books are now thinner than the government’s parliamentary majority.

“The residential sector, which previously dragged the industry as a whole into growth territory, is retreating into its shell. With house-builders’ totemic ability to defy weakness elsewhere now gone, the mood on the frontline is getting steadily bleaker.

“With three months to go until Halloween, there is no sign of the stockpiling that propped up activity in the run up to 29th March – what should have been Brexit Day. With the pound holed below the waterline, imported materials are becoming more expensive by the day, and rising wage costs continue to slice into builders’ margins. Finance remains cheap and plentiful, but unfortunately this counts for little when business optimism is at its lowest level for almost seven years.

“With investors sitting on their hands until the angst of uncertainty ends, the best the industry can hope for during the final Brexit countdown is to batten down the hatches, complete existing projects and keep its capability up in hopes of a surge of deferred investment in the final months of the year.”

Got a story? Email news@theconstructionindex.co.uk