Every month, using figures compiled by The Builders’ Conference, our Contracts League reveals who’s winning the most work. And every month no matter who comes out on top, by far the greatest volume of new work is let in the residential sector.

House-building is the industry’s biggest single sector and house-builders enjoy the highest profit margins. But this month’s Sector Focus paints an unusually disturbing picture of what’s happening at the top of the house-building tree.

As we noted this time last year, the residential sector’s vigorous growth trajectory was levelling off. Change was in the air, we suggested.

But as things turned out, it was more than just change in the air: there was also an especially virulent virus out there too.

This article was first published in the Dec/Jan 2021 issue of The Construction Index magazine. Sign up online.

There’s no doubt that Covid-19 has already had some impact on the UK’s house-building industry. All sites closed at the end of March when prime minister Boris Johnson delivered his first fateful briefing and announced a nationwide lockdown.

And unlike some other sectors, house-building was not considered “essential work” so housing developments were among the last sites to re-open in the summer.

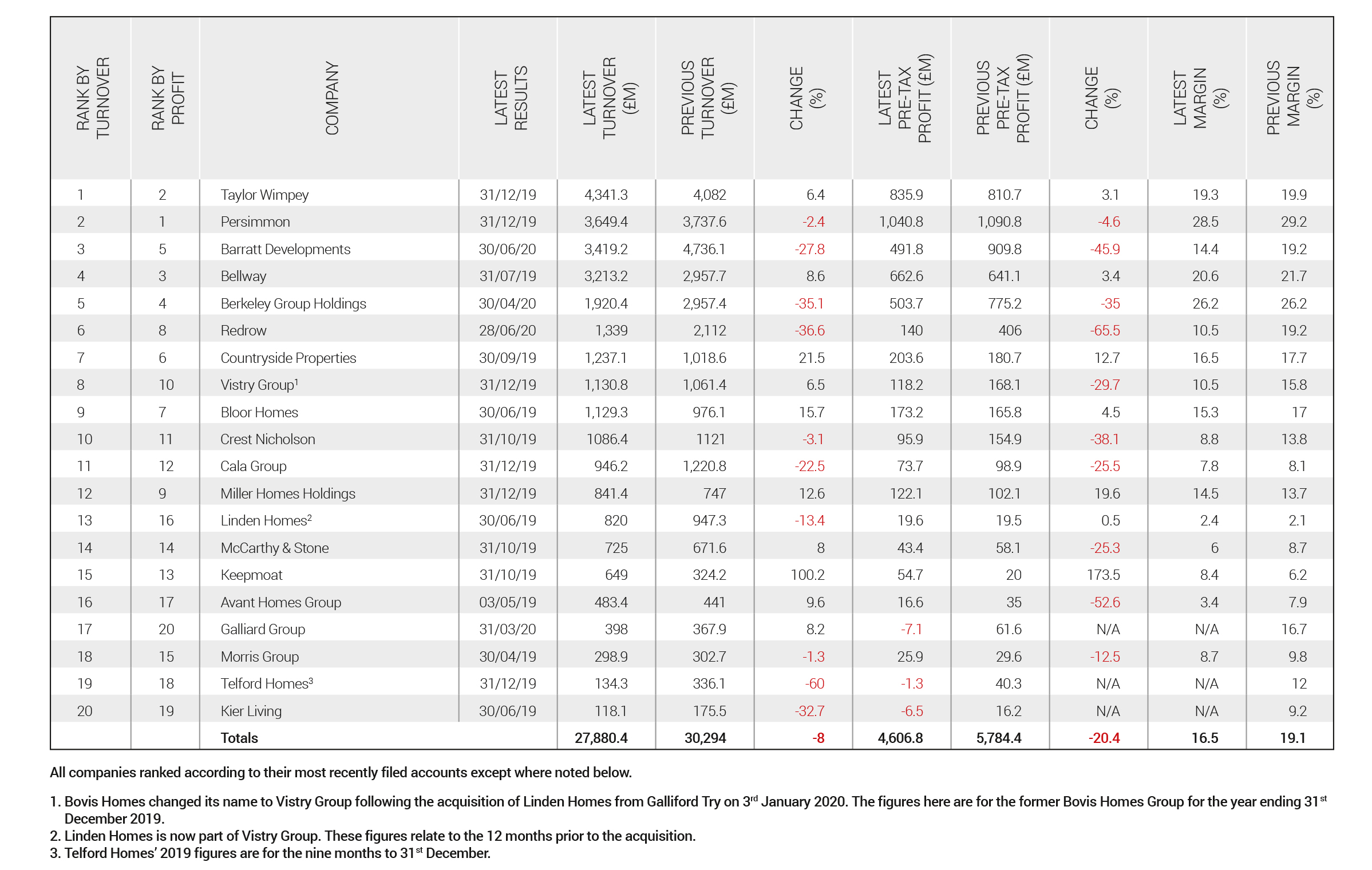

Ever since we started compiling our regular Sector Focus, five years ago, the same three house-builders have occupied the top three positions on the table: Barratt Developments at number one, Taylor Wimpey second and Persimmon third.

This year, for the first time, Barratt has slipped and is now in third place; Persimmon moved up to second place and Taylor Wimpey is on top.

It is probably significant that Barratt Developments is one of only four companies in our selection of the top 20 house-builders to have reported results for a period ending in 2020.

Barratt’s turnover for the 12 months to the end of June this year was £3.4bn, down 27.8% on last year’s figure of £4.7bn. Pre-tax profit was almost halved, down 45.9% to just £491m (2019: £909.8m).

In his commentary to the financial statements published in September, Barratt chairman John Allan said: “The onset of Covid-19 and the subsequent lockdown has caused significant disruption to our business and had a substantial impact on our financial performance.”

The business had coped with the shock of Covid-19 by suspending land purchases, freezing all recruitment and postponing all capital investments to manage cash-flow and ensure resilience.

Things will get better next year, promised Allan: “The government recognises the importance of house-building in achieving their ‘levelling-up’ agenda. The stamp duty holiday is an important intervention that will save many of our customers thousands of pounds which they can put towards the deposit for their new home.”

In his annual statement, chief executive David Thomas said that there had been a “significant reduction in completion volumes” as a result of Covid-19. The pandemic also incurred additional costs including £45.2m in “safety costs, non-productive site costs and site-based employee costs” as well as £29.1m related to an expected increase in site durations.

This almost halved the profit figure and reduced operating margin to 14.8% from 19% in 2019.

The latest figures for both Taylor Wimpey and Persimmon relate to the 12 months to 31st December 2019 – before Covid-19 had a name and before there was any knowledge of its existence outside of China.

But although Taylor Wimpey notched up a record number of completions and rose to pole position on our table (with turnover up 6.4% to £4.3bn and pre-tax profit up 3.1% to £835.9), chief executive Pete Redfern said that 2019 had not been without its challenges. “In fact, I would say that, in many ways, it has been one of the toughest we have faced in our recent past.

“In an environment where the political and economic outlook has been uncertain, sales prices have remained flat but build cost inflation has increased,” explained Redfern.

Persimmon would probably agree that 2019 had been a challenging year, but at least the company appears to have risen to that challenge. In the past couple of years, Persimmon’s reputation has taken a battering, largely resulting from the unhealthy disparity between the huge bonuses paid out to its executives and the shoddy standard of its work.

In his annual statement, published in June, group chief executive Dave Jenkinson placed huge emphasis on the lessons learned from the independent review of its operations which Persimmon commissioned in April 2019. Under the headline “Putting our customers before volume”, Jenkinson explained that Persimmon introduced a new customer care plan at the beginning of 2019 with the aim of improving the group’s performance “on all aspects of build quality and customer experience”.

The company has made a “significant investment in our customer care resource which has increased by 52% year on year, with a 70% increase in site-based customer care staff,” continued Jenkinson.

Persimmon also introduced a new Homebuyer Retention Scheme – “a first for the UK housebuilding industry” – in July 2019 with the aim of “[driving] behavioural change throughout the business and [reinforcing] the Group’s objective of delivering higher levels of build and finish quality”.

In February Jenkinson notified the board of his intention to step down as CEO. He finally departed in September after having sold almost £7m-worth of Persimmon shares awarded to him as part of the controversial bonus scheme a couple of years earlier.

Persimmon’s new priority – to put its customers before profit – does seem to be paying off, though. While the company still made more profit before tax than any other house-builder in the top 20 last year, that profit figure of £1,040m was about 5% below the previous year’s on slightly reduced turnover of £3.6bn (2018: £3.7bn).

House-building is a very profitable business compared to other sectors of the construction industry, but our analysis of the top 20 companies this year reveals that no fewer than 10 of them saw profits decline last year, while a further three actually made a pre-tax loss. Overall, there was a more than 20% decline in pre-tax profits and average margin fell from 19.1% to 16.5%.

Galliard Group was the biggest loss-maker with a pre-tax loss of £7.1m in the year to March 2020. Chairman Stephen Conway said:

“The effects of the pandemic were not felt until the end of our financial year which limited the impact on the results we are now publishing. The housing market was, as we anticipated, showing signs of recovery after the long period of uncertainty caused by Brexit’s political stalemate just as the next crisis hit. The resultant delays in sales completions and downward pressure on site values have, inevitably, affected us adversely and in consequence the profit I was expecting to report for the year has been turned into a pre-tax loss of £7.1m.”

If the Covid-19 pandemic (which hadn’t closed any sites until the fourth week of March) could have such a profound effect on Galliard’s profitability, the lockdown that followed must have wrought havoc in the sector.

We’ll see the full effects of that this time next year.

This article was first published in the Dec/Jan 2021 issue of The Construction Index magazine. Sign up online.

Got a story? Email news@theconstructionindex.co.uk