The Budget 2021’s new super-deduction allows you to claim a 130% capital allowance against qualifying new plant purchases.

If new plant and equipment acquisitions are feature of your business plans for the next 10 months to April 2022, then chancellor Rishi Sunak’s new super-deduction could both save tax and, if you buy your new plant using hire purchase, optimise cashflow if you time your purchase right.

The super-deduction capital allowance is one of the many measures introduced in the March Budget designed to stimulate business investment as the UK economy opens up after the latest lockdown. Expiring in April 2022, it is designed to encourage qualifying businesses making qualifying purchases to invest quickly, boosting the plant and equipment supply chain, but also improving the productivity and competitiveness of UK firms. The keyword here is ‘qualifying’ – the small print specifies restrictions on the types of business and equipment that can be acquired using the new capital allowance.

What are capital allowances?

When you buy an asset that will be used by your business, such as a Case wheeled loader, a capital allowance enables you to deduct some of the value of the acquisition from your profits. This in turn generates a corporation tax saving for limited companies, or an income tax saving for partnerships and sole traders.

The basic capital allowance available to all UK businesses is the writing down allowance (WDA). This allows you to deduct 18% of the cost of the asset each year over the asset’s lifetime, until you stop using it. Here is worked example for year 1:

- If the asset cost your limited company £100,000, the WDA is £18,000 (18% of £100,000).

- Let’s say your pre-profit is £1m, then at the current 19% corporation tax (CT) rate, your CT tax liability would be £190,000.

- The £18,000 WDA can be deducted from your pre-tax profits, so for tax purposes your profit is reduced to £982,000 (£1m - £18,000).

- Apply the 19% rate to the new profit of £982,000, and you get a CT liability of £186,580, which represents a CT saving of £3,420.

- In practice, you could apply WDA to all your qualifying purchases. If you’ve invested significantly, then the tax saving is correspondingly significant.

- The standard WDA can be applied each year, to the reducing asset value as it is written down. There are no expenditure limits or qualification periods.

The next capital allowance is the annual investment allowance (AIA). All business types, including sole traders, partnership and limited companies, qualify. There is a qualification period of January 2021 to December 2021 and an expenditure limit of £1m, i.e. the first million pounds of your plant and equipment investment during the period will qualify. Most importantly, there is a 100% allowance on plant and machinery, both new and used, during the period. Here is a worked example for a limited company:

- You buy your asset, such as the Case wheeled loader example used above, for £100,000 in May, during the January to December 2021 qualifying period, and it is the only asset bought to date.

- The asset cost your limited company £100,000, so the AIA is £100,000 – remember, AIA is 100% of the asset value up to £1m in the period

- As above, your pre-profit is £1m, then at the current 19% corporation tax (CT) rate, your CT tax liability would be £190,000.

- The AIA can be deducted from your pre-tax profits, so for tax purposes your profit is reduced to £900,000 (£1m - £100,000).

- Apply the 19% rate to the new profit of £900,000, and you get a CT liability of £171,000, which represents a CT saving of £19,000.

- As there are restrictions on the timing of this allowance, when you buy your plant can impact on you tax and cashflow benefits. Professional advice from an appropriately qualified accountant is essential when taking this decision.

The restrictions are detailed above. The AIA was introduced in 2008 to stimulate investment during the recession of the time and has been renewed every year since. It may be renewed again as it has been in the past, but this is not confirmed. Something else to check with your accountant if you are considering asset purchases that may overlap into 2022.

How does the super-deduction work?

There is now a third capital allowance, the super-deduction. There are qualifying conditions:

- The 130% first year allowance only applies to new plant and machinery, not pre-owned.

- Only limited companies qualify, not sole traders or partnership. This means only corporation tax savings can be made, not income tax.

- There are no expenditure limits, unlike the AIA.

- The scheme ends on 31 March 2023.

- Cars, used equipment and assets subject to onward hire are excluded, so you can’t use the scheme to acquire plant and equipment you plan to rent out.

A major difference, and presumably why it is called a ‘super-deduction’, is that the allowance is worth more than what you paid for the asset. For comparison, here is the worked example for the wheeled loader above:

- Your limited company (remember only limited companies qualify) buys your asset for £100,000.

- Your pre-profit is £1m, then at the current 19% corporation tax (CT) rate, your CT tax liability would be £190,000.

- Here is where the super-deduction is different from the WDA and AIA: you can deduct 130% of the asset value, or £130,000, from your pre-tax profits

- This means for tax purposes your profit is reduced to £870,000 (£1m - £130,000).

- Apply the 19% rate to the new profit of £870,000, and you get a CT liability of £165,300, which represents a first-year CT saving of £24,700 (compared to the £19,000 under AIA, or £3,420 under WDA).

This allowance expires on 31 March 2023 and the basic rate of corporate tax is due to rise to 25% from April 2023. As a result, the timing of when you buy your plant is particularly important to optimise both tax savings and cashflow benefits, and the calculations are quite complex, so professional advice from an appropriately qualified accountant is essential.

Careful timing using higher purchase (HP) optimises tax and cashflow benefits

The super-deduction can also be applied to assets acquired via a hire purchase (HP) agreement, where the user owns the asset at the end of the agreement. Plus, there is an added benefit of the scheme as the super-deduction has both a capital and interest allowance. This means that there is a significant cashflow advantage of buying the asset using HP rather than paying cash.

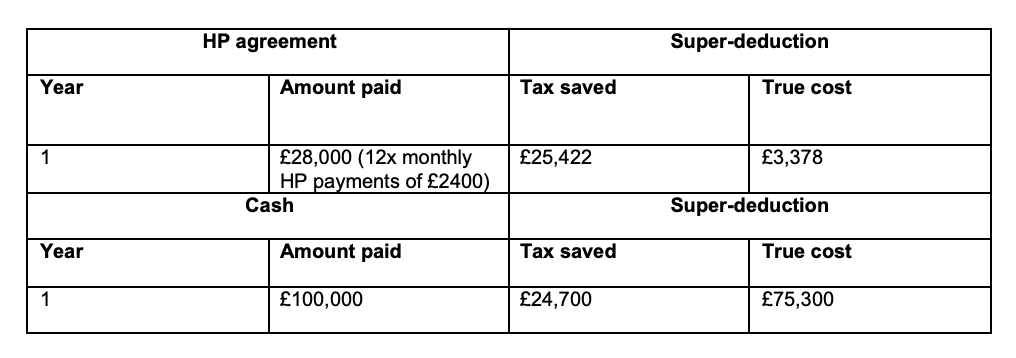

Let’s look at another example. Instead of buying the asset outright using cash, you’ve bought £100,000 of plant (including the deposit) over a 4-year HP agreement. The payments are £2,400 per month, totalling £115,200. Interest is £3,800 per year, totalling £15,200.

Crucially, the super-deduction applies in year 1, so even though you have not paid out £100,000 in cash on your asset, you still get the corporation tax saving of £24,700 (see the worked example in section above for the calculations).

The comparison is shown in the table below.

What’s immediately clear is that your ‘true cost’ in year 1 is only £3,378 if acquiring the asset using HP, rather than £75,300 if using cash. And you get to use the machine to generate income right from the start. Once again, when making any investment decisions always consult a qualified accountant first.

If timed correctly, and if right for your company, the combination of the new super-deduction scheme and hire purchase could enable you to buy machinery and plant that might not have featured in your business plans before the Budget.

This article was paid for by Case Construction Equipment

Got a story? Email news@theconstructionindex.co.uk

.gif)