Construction output dropped for the fourth consecutive month in August 2019, according to the latest monthly survey of industry purchasing managers, suggesting an industry in recession.

Commercial work was again the worst performing area of activity in August, with survey respondents citing delayed decision-making among clients in response to domestic political uncertainty. At the same time, construction firms indicated that their business expectations for the year ahead weakened sharply since July and were the least upbeat since December 2008.

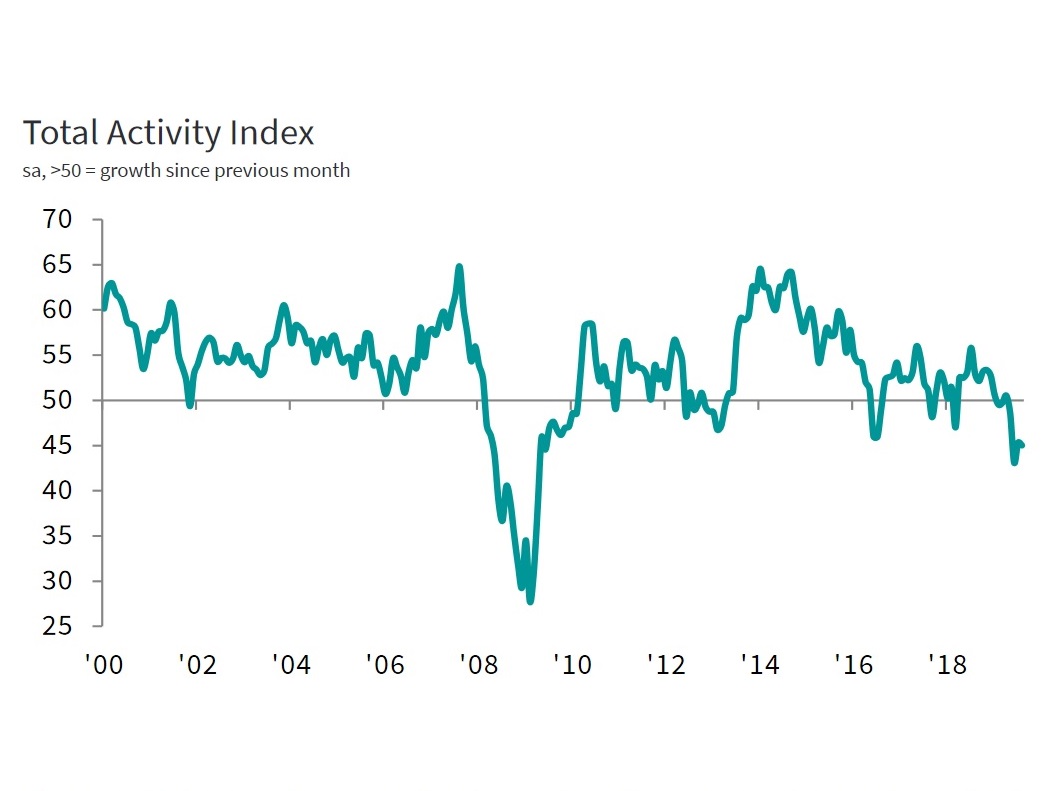

The headline seasonally adjusted IHS Markit/CIPS UK Construction Total Activity Index registered 45.0 in August, down slightly from 45.3 in July and below the 50.0 no-change threshold for the fourth consecutive month.

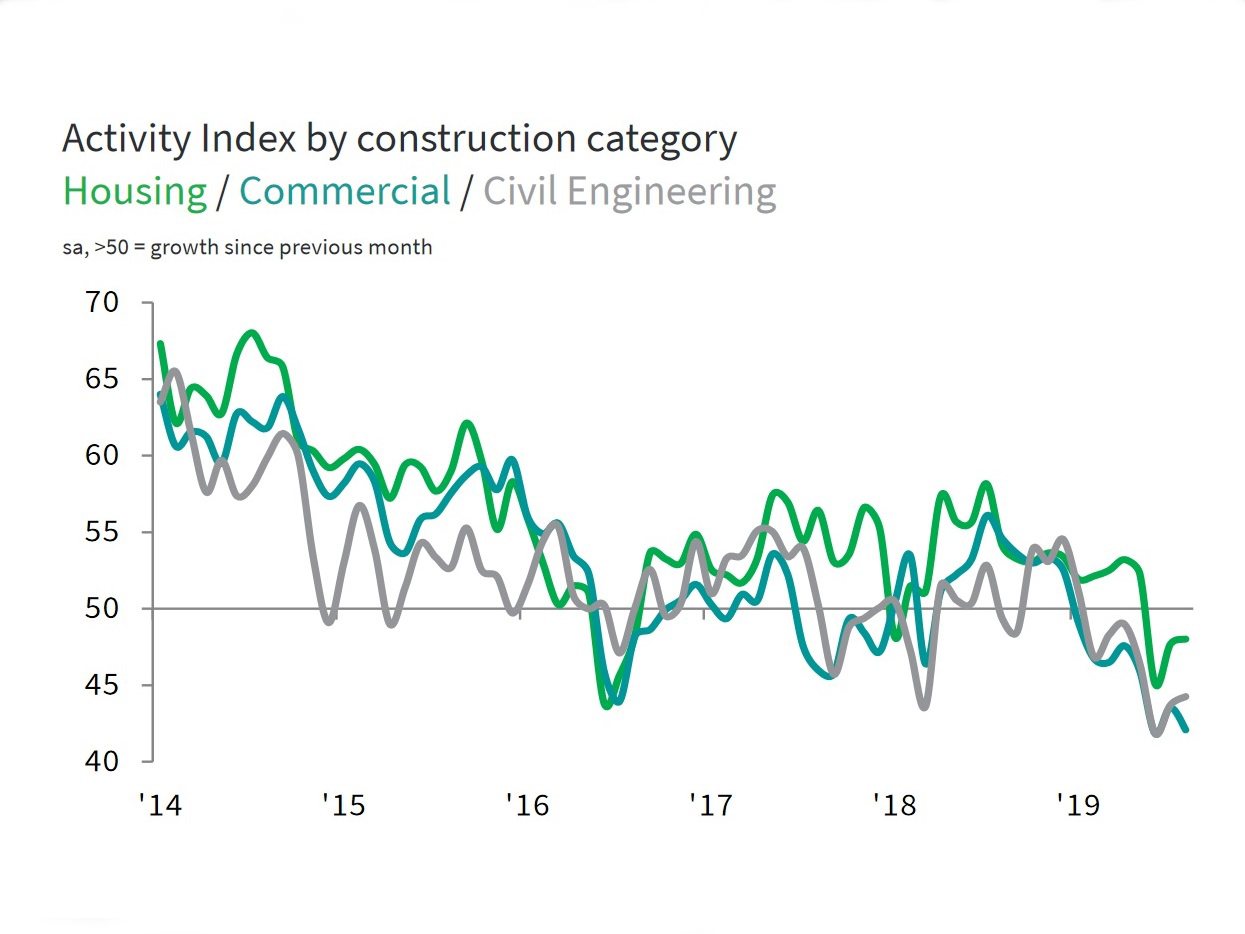

Lower volumes of construction output were attributed to worsening order books and a lack of new projects to replace completed contracts. All three broad categories of construction work decreased in August, led by commercial building. Survey respondents continued to cite Brexit-related uncertainty discouraging investment. Civil engineering activity also dropped at a relatively sharp pace during August. Even house-building fell, although only slightly and its rate of decline was the least marked since the downturn began in June.

According to data gathered by this survey series, new orders received by construction companies have now dropped in each month since April. Latest data signalled a sharp decline in new work, with the rate of contraction the fastest since March 2009.

Softer demand for construction products and materials helped to alleviate pressure on supply chains, however, with delivery delays from vendors among the least widespread for three years. Thus input cost inflation moderated to its lowest since March 2016.

Meanwhile, construction companies indicated a slide in business optimism, with the degree of positive sentiment the weakest since December 2008. Concerns about the business outlook were overwhelmingly attributed to domestic political uncertainty and a corresponding drop in client spending.

Tim Moore, economics associate director at IHS Markit, which compiles the survey, said: “Domestic political uncertainty continued to hold back the UK construction sector in August, with survey respondents indicating that delays to spending decisions had contributed to the sharpest fall new work for over 10 years.

"Construction companies noted that rising risk aversion and tighter budget setting by clients in response to Brexit uncertainty had held back activity, particularly in the commercial sub-sector. Commercial construction activity fell at a steep and accelerated pace during August, which more than offset the softer rates of decline in house building and civil engineering work.

"Concerns about softening demand for new projects resulted in a fall in business optimism across the construction sector to its weakest since December 2008. This provides an early signal that UK construction companies are braced for a protracted slowdown as a lack of new work to replace completed contracts begins to bite over the next 12 months."

Duncan Brock, group director at the Chartered Institute of Procurement & Supply, which sponsors the survey, added: “The sector fell deeper into contraction as continuing uncertainty and a weakened UK economy took a sizeable bite out of this month’s construction activity. Inevitably business confidence followed suit, dropping like a brick to its worst since December 2008 and close to the lowest depth seen in the previous recession.

"As Brexit creeps closer and confusion still reigns, this will undoubtedly heap more pressure on the UK government to create much-needed clarity in the market. The commercial sector particularly has been devastated by reluctant clients fearful of taking a wrong turn in a confusing landscape and delaying project starts, resulting in the fastest drop in new orders since March 2009.

"In contrast, job creation remained fairly steady as companies strived to retain talent and the anxieties of further price rises for materials eased slightly which offers some respite for construction margins.

"The reality is, if a revival of confidence and a flood of new orders return to the construction sector in the coming weeks, much like a large tanker turning in a dock, there is little room for the sector to improve in the last quarter of the year. It’s likely September’s data will be even more discouraging."

Industry reaction

Jonathan White, UK head of infrastructure, building and construction at KPMG, said: “Another consecutive month of declining outputs paints a bleak picture of the sector. It’s likely we’re going to see a muted pipeline of projects until we have a clearer vision on what the country’s economic and political future will look like, given some large-scale plans are being halted, preventing shovels from going in the ground.

“There is still a pool of eager investors and demand for new work, but it’s currently a case of hanging fire until the mist clears. Only then, when people feel surer about the months ahead, will we see some momentum build.”

Gareth Belsham, director at surveyors Naismiths, said: “The flow of new orders has dried up from a drip to a desert. We’re fast approaching the critical point where the pipeline of new work isn’t close to keeping up with the pace at which projects are being completed.

“This worsening shortfall is slicing into contractors’ margins and decimating confidence. Little wonder that business sentiment has slumped to its lowest level since the dark days of 2008.

“While the pain is being felt most acutely in commercial sector construction, the residential sector is also retreating into its shell. With housebuilders’ ability to mitigate the weakness elsewhere now gone, the mood on the frontline is getting steadily bleaker.

“Finance remains cheap and plentiful, with several challenger banks stepping up to keep developers’ wheels turning. But the brutal truth is many investors have decided to sit on their hands until Britain’s political paralysis ends.

“Whether the Brexit endgame brings an election, a ‘no-deal’ or both remains largely moot. For now all the construction industry can do is to batten down the hatches, complete existing projects and retain its capability in the hope that the final months of the year see an unblocking of three years of deferred investment.”

Scape Group chief executive Mark Robinson said: “Today’s data paints a gloomy picture of the industry. The problem is that both the public and private sector are delaying spending in the run-up to the Brexit crunch date and business optimism has been knocked down to levels not seen since towards the end of the 2007 recession.

“The bad news is that the outlook is likely to deteriorate further in the coming weeks. However, tomorrow’s spending review provides the Government with an opportunity to inject a feel-good feeling back into business. UK plc needs bold decision making, clear commitments, and guaranteed funding. Especially in a no-deal scenario.”

“But, unless the chancellor pulls something out of the bag, the industry will be holding its breath for a Brexit bounce after October 31st. That could help turn things around by the end of the year.

“On a positive note, it is promising to see that a serious loss in momentum has not affected employment trends – although that might have a lot to do with the ‘Builder Brexodus’ of EU workers heading home. Despite domestic political uncertainty, we continue to need new schools, roads and hospitals. Business will brighten up again, and we must have the manpower in place to build for when it does.”

Got a story? Email news@theconstructionindex.co.uk