.jpg)

Point-of-sale data collated for the Builders Merchant Building Index (BMBI) shows the value of sales was up by 6.2% in September 2021 compared to August and by 14.9% compared to September 2020.

However, with inflation pushing up the price of building products, these numbers do not mean that builders are necessarily buying any more products and thus doing more work, as we might expect. It just means that they are spending more money on their materials.

Year-on-year sales of Timber & Joinery Products were up 38.7% by value in September. Sales of Kitchens & Bathrooms rose 11.8% on the year to recorded its highest-ever BMBI monthly sales (although BMBI only started in 2015).

Compared with pre-Covid times, the total value of sales in September 2021 was 24.5% higher than September 2019, with one more trading day this year. Much of this growth is owed to Timber & Joinery Products (54.1%) and Landscaping (40.2%). Without these two categories in the calculations, the two-year growth is 13.3%.

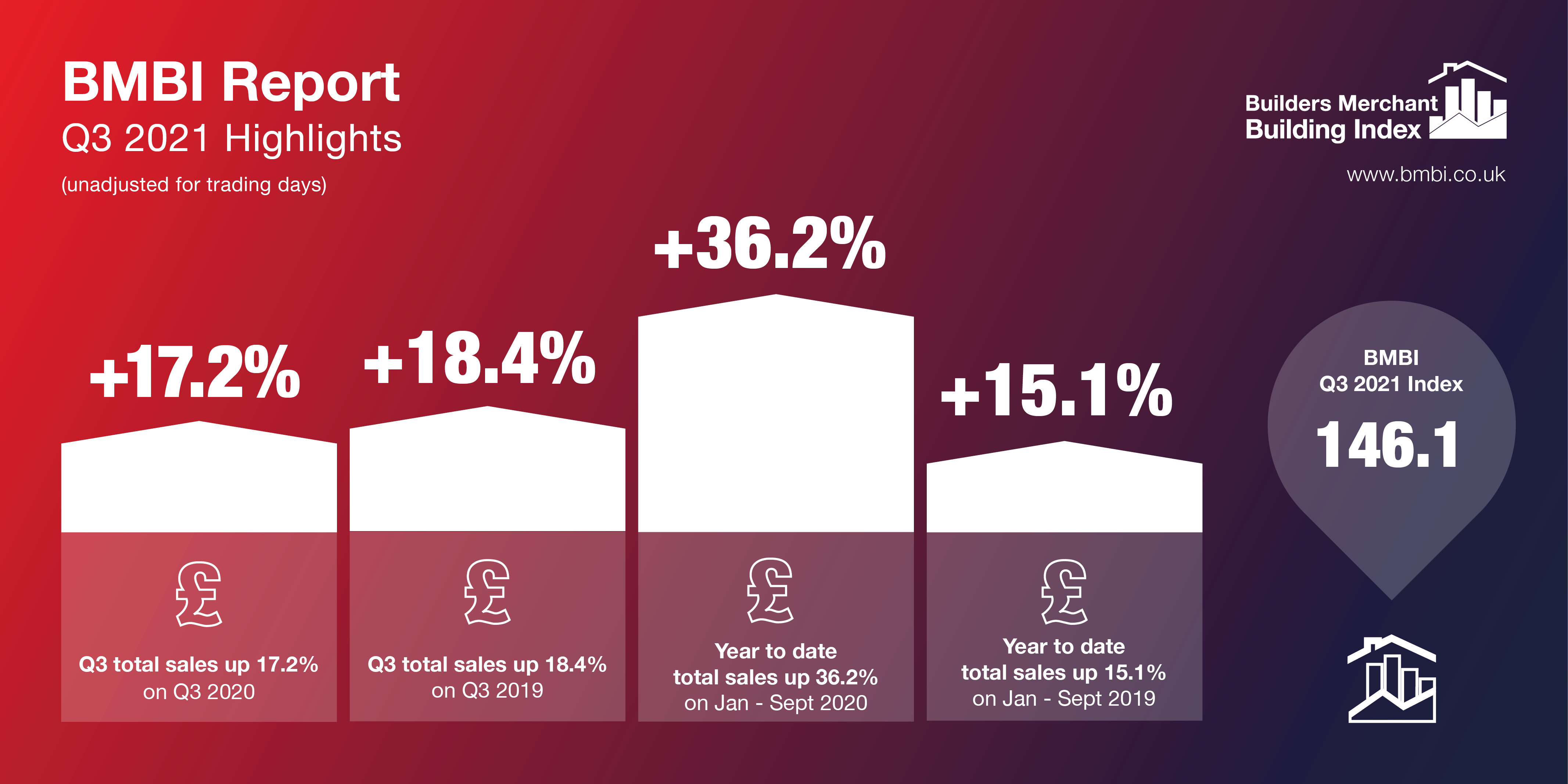

After sales softened in August, the bounce-back in September made the third quarter of 2021 the second best for builders’ merchants since the record keeping began six years ago. Only the previous quarter, Q2 2021, has seen higher sales.

Total value sales in Q3 2021 were 17.2% higher than Q3 2020, with one less trading day this year. Timber & Joinery products led the field, growing 43.9%. Excluding Timber, total merchant sales still grew by 9.6%. Like-for-like-sales increased by 19.1%.

Comparing Q3 2021 with pre-Covid Q3 2019, the overall value of sales was up 18.4% with one less trading day this year. Timber & Joinery products were up 48.9% and Landscaping products were up 30.2%. Like-for-like sales were up 20.2%.

Quarter-on-quarter, sales were down 2.4% in Q3 2021 compared to Q2, despite the three extra trading days in Q3. Kitchens & Bathrooms and Timber & Joinery were up modestly but Landscaping was down nearly a quarter. Like-for-like sales were 7.0% lower than in Q2.

Mike Rigby, chief executive of MRA Research that produces the report, said: “This year has been just as unexpected as 2020 for merchants, but for more positive reasons, with the most recent quarter showing a continuation of the strong growth experienced throughout 2021. Year-to-date, the sector is up by 36.2% in value over 2020, and 15.1% ahead of the same period in 2019. That’s way ahead of growth forecasts made at the beginning of the year. However, the sector is now starting to see the first signs of easing as price increases take over from volume sales to drive value growth.

“Housebuilding and infrastructure projects continue to boost sales, with heavy-side activity – such as the astounding growth of timber and landscaping sales and the strong performance of heavy building materials – driving growth.

“The final quarter of the year is likely to see a slowdown in demand, as merchants’ sales return to more manageable levels after an exceptionally busy year. Supply chain problems seem to be easing, but a consensus in the market suggests these could persist until 2023 so we are not out of the woods. But it’s safe to say, that end of year figures will be noticeably ahead of initial forecasts in an exceptional year.”

Jim Blanthorne, managing director of Keylite Roof Windows, said: “The last quarter brought more of the same for roof windows; more demand, more material challenges and more cost increases. The cost of containers from the Far East shows no sign of normalising. Perhaps the current rates are the new normal, however we assume competitive forces will return once global supply chains find an equilibrium. Most commentators have given up predicting when this will be, but it won’t be before Chinese New Year. At our manufacturing and distribution locations, statutory changes and market forces are resulting in wage costs continuing to rise above the rate of inflation. Timber prices have softened, yet availability remains a challenge on certain specifications. Aluminium and PVC prices are up significantly. All in all, a shortage of good news stories when it comes to supply and cost.”

Got a story? Email news@theconstructionindex.co.uk