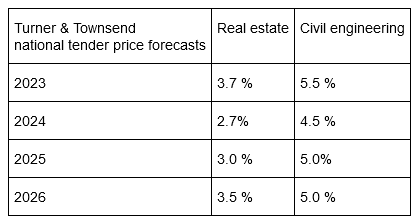

Turner & Townsend is forecasting that tender price inflation will remain stubbornly high over the next three years, with real estate forecasts at 3.7% and 2.7% for 2023 and 2024, respectively, and 5.5% and 4.5% for infrastructure.

Turner & Townsend’s forecasts are largely unchanged since its last report in June although it has become less pessimistic about real estate tender price inflation in 2025 and 2026, cutting its forecasts from 4% to 3% and from 4.5% to 3.5% respectively.

Martin Sudweeks, UK managing director of cost management at Turner & Townsend, said: “Our industry is currently managing an incredibly complex landscape as we experience both softening demand and the continued input cost inflation. This is driven in large part by an endemic skills shortage that is pushing up labour costs – sector must work with government and education bodies to tackle the jobs market crunch.

“In the face of immediate cost challenges, it may appear an attractive option for clients to dedicate their efforts to firefighting the issues of ‘today’, while losing sight of commitments to policies like net zero. However, clients should instead be prioritising their long-term strategies, and understanding how profitability, project performance and sustainability can be complementary goals. By doing this, clients will be able to achieve both short-term stability and future, strategic success.”

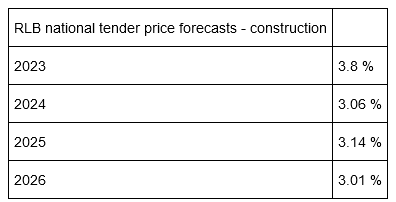

Also out this week are Rider Levett Bucknall’s latest forecasts. RLB provides its forecasts for construction tender price inflation, without segmentation. Overall it sees inflation easing a little more over the coming years than Turner & Townsend predicts. In 2026, for example, RLP predicts 3.01% construction tender price inflation, which is below the 3.5% that Turner & Townsend predicts for real estate and well below its 5% for civil engineering.

Rider Levett Bucknall research & development manager Roger Hogg said: “Although commodities and materials prices have been noted across the regions as having moderated, construction costs have risen significantly over the last couple of years and have consequently brought viability issues into sharp focus. Just as contractors’ margins can be squeezed in competitive circumstances, so too can client business cases suffer when cost imposts exceed value growth. What we have previously referred-to as ‘sticky’ inflation, is persisting and there is no real prospect of actual falls in construction prices.

“Weakness in new orders statistics in some regions, together with a broad body of project work having reached and about to reach completion, will continue to attract the attention of main contractors and sub-contractors. The replacement of the tail of existing workload is even more of an issue in light of the continued, though now more moderate, levels of materials price inflation and labour cost inflation. All of this is surrounded by the wider performance levels of the general economy and in particular, inflationary effects on labour operating in construction, who have to be compensated in sufficient terms for them to stay in the sector. The fact of the continuing shortages of labour, with no obvious solution in terms of growing numbers of operatives, may yet drive further production off-site, but that process is no overnight solution. In the meantime, cost imposts from the labour component of the build-up will become an even more relevant issue and proportion of the whole.”

Got a story? Email news@theconstructionindex.co.uk