UK construction activity decreased for the fourth consecutive month in April as rising business uncertainty led to delayed decision-making on new projects.

That is according to the latest monthly survey of construction purchasing managers, which also indicates further declines in total order books and cutbacks to staffing numbers.

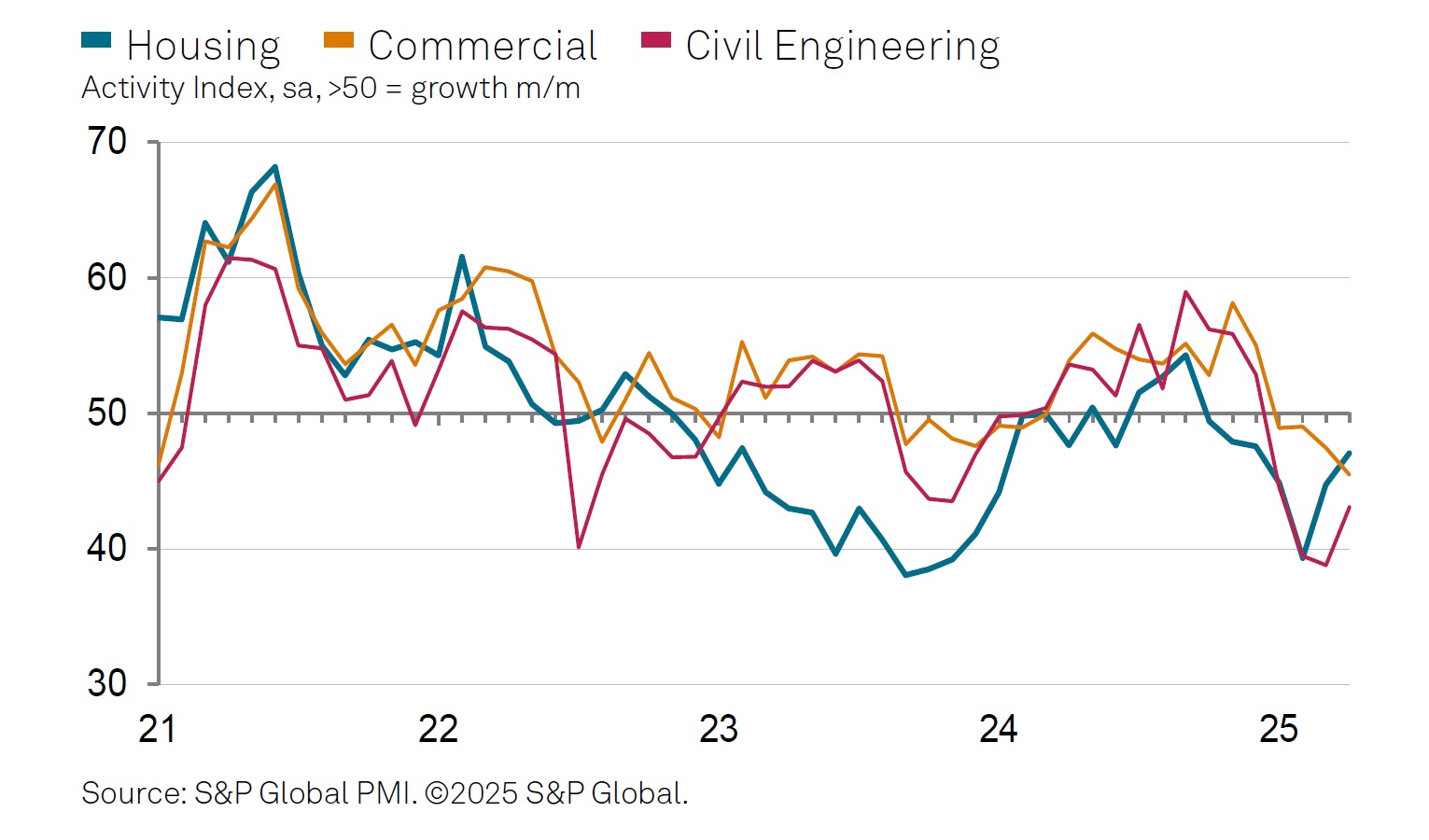

At 46.6 in April, the headline S&P Global UK Construction Purchasing Managers’ Index (PMI) remained below the 50.0 no-change value – it has been in this negative territory every month of 2025 so far – but was at least up slightly from March’s 46.4 reading and February’s 44.6. (The lower the number, the worse things are.)

All three broad categories of the industry – house-building, civil engineering and commercial construction – remain in decline.

The house-building sector’s reading of 47.1 was as good as it has been all year. Civil engineering remained the weakest performer at 43.1 (up from 38.8 in March), with a distinct lack of new work to replace completed projects.

But while house-building and civil engineering have at least moved in the right direction, the decline of commercial work has been accelerating: 49.0 in February, 47.4 March and now 45.5 in April, its worst reading since May 2020. Construction companies widely noted that heightened business uncertainty and worries about the broader UK economic outlook had weighed on client demand.

April data indicated a steep reduction in total new work and the pace of decline was the second-fastest since May 2020. Survey respondents typically commented on the impact of subdued business and consumer confidence.

Lower workloads resulted in the fastest decline in purchasing activity for nearly five years in April. For those with work, however, it has meant materials are easier to source. Wait times for suppliers' deliveries have now improved in each of the past three months, although some firms continued to report international shipping delays.

Despite weaker demand conditions, latest data indicated another sharp increase in average cost burdens. Construction companies noted that a wide range of items had risen in price, particularly concrete products, insulation and timber, but some firms noted lower fuel costs. Many firms reported that suppliers had also sought to pass on rising payroll costs.

Staffing numbers across the construction sector meanwhile decreased for the fourth consecutive month, but the rate of job shedding eased slightly since March. Subdued demand and rising pay pressures were cited as reasons for the non-replacement of voluntary leavers.

Looking ahead, construction firms are optimistic on balance about their prospects for the next 12 months. Around 41% of the survey panel forecast a rise in output, while only 18% predict a decline. This signalled a slight improvement in business optimism to its highest since December 2024. A number of firms commented on positive expectations for residential building work, despite ongoing domestic economic headwinds and fragile client confidence.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the monthly survey, said: "UK construction companies have endured a bumpy ride since the start of the year as domestic economic headwinds and hesitancy among clients led to a lack of new work to replace completed contracts.

"Output levels continued to slide in April, but the rate of decline eased to its slowest for three months. This was helped by slower reductions in residential building work and civil engineering activity.

"Commercial construction was a weak spot and lost momentum since March. Output decreased at the fastest pace for nearly five years amid reports of greater risk aversion among clients and a wait-and-see approach to major spending decisions.

"Despite a sharp and accelerated fall in input buying, strong cost pressures persisted in April. Overall input price inflation eased only slightly from March's 26-month peak. Survey respondents commented on rising prices paid for a range of raw materials, as well as efforts by suppliers to pass on greater payroll costs.

"An encouraging development in April was a slight improvement in business activity expectations for the year ahead. Output growth projections improved to the highest level so far this year, with a number of survey respondents citing the prospect of a turnaround in

workloads across the residential building segment."

Lauren Pamma, head of energy & infrastructure at Aldermore Bank, said: “Businesses are feeling the burden of April’s rises in national insurance contributions and the national minimum wage, which has meant rising payroll costs. Stagnant demand, rising interest rates and delayed decision making on new projects seem to be continuing to take its toll as well. We’re beginning to see the fallout from the ongoing cross-border tariff war which will no doubt disrupt supply chains and impact prices further moving forwards.”

However, Brian Smith, head of cost management and commercial at Aecom, was more optimistic. “It’s encouraging to see that the pace of decline is slowing,” he said, “as we hope to see activity and order levels continue to recover through the summer.

“The government has made it clear how important new infrastructure and house-building will be in catalysing growth, and the sector stands ready to deliver. But what’s less clear is how this is going to be funded. Next month’s spending review is a real opportunity for policymakers to set out a clear roadmap for public-private partnerships that draw in private investment to provide the much-needed backing for large-scale projects.

“Contractors and developers are under no illusion of there being a single silver bullet to get more spades in the ground though. A cut in interest rates this month is one of a number of more longer-term factors that will support growth, while we await further progress on planning reform."

Got a story? Email news@theconstructionindex.co.uk