The monthly survey of construction purchasers indicates a slight increase in industry activity in March, ending a six-month period of decline.

Survey respondents often commented on a turnaround in sales pipelines and greater new business enquiries linked to the improving economic outlook and more stable financial conditions. New orders also appear to have expanded at the fastest pace since May 2023. However, construction companies remained cautious about hiring staff, with employment numbers falling for a third consecutive month.

The headline S&P Global UK Construction Purchasing Managers’ Index (PMI) rose from 49.7 in February to 50.2 in March. Any reading above 50.0 indicates an overall expansion of construction output. Although signalling only a fractional rise in business activity, the index was in positive territory – indicating growth – for the first time since August 2023.

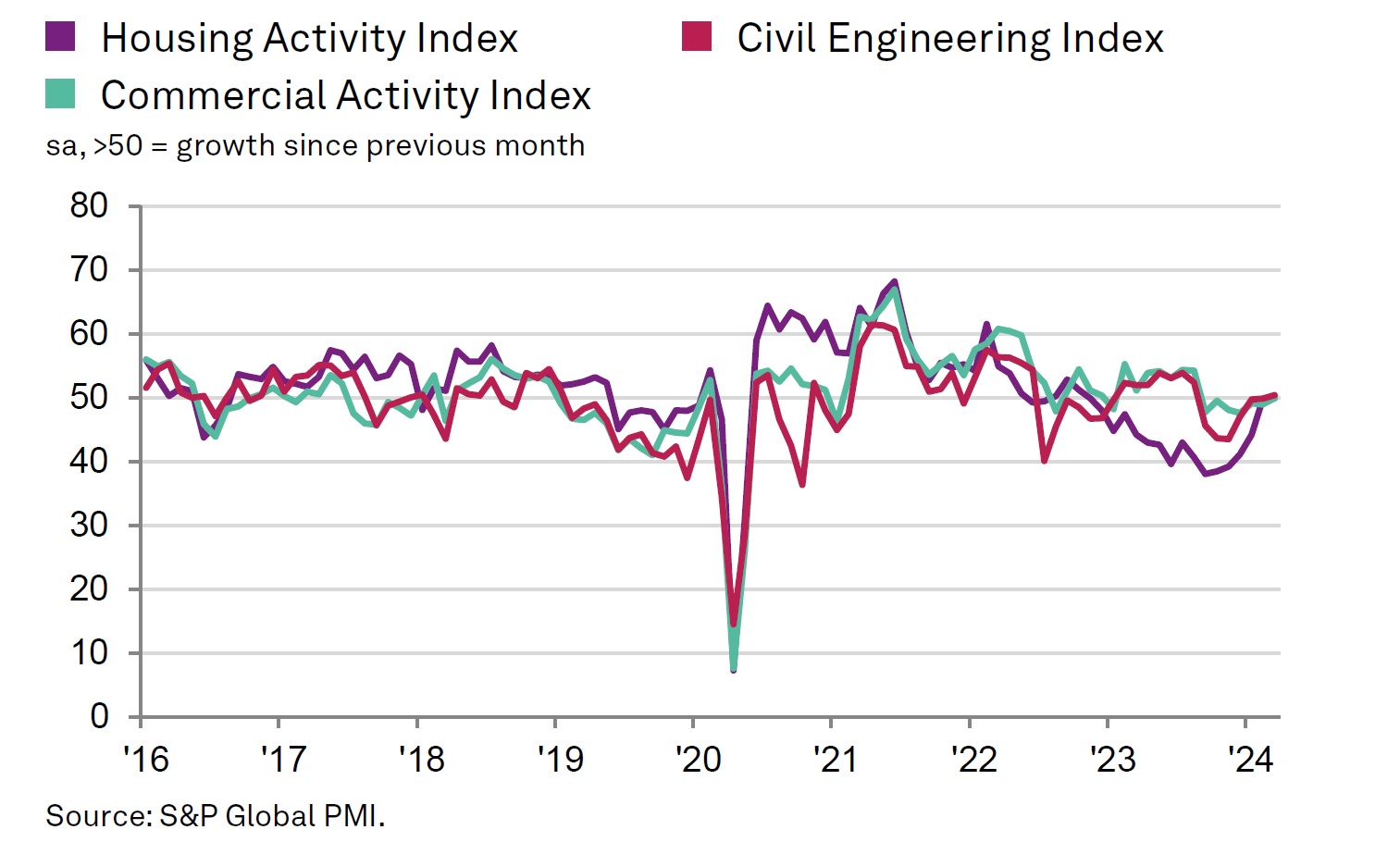

Civil engineering was the best-performing segment in March, as output levels increased at a marginal pace. Panel members cited increased work on infrastructure projects and resilient demand in the energy sector.

House-building and commercial construction activity were both broadly unchanged in March. The stabilisation in residential work represented the best performance for this category since November 2022.

March data pointed to a modest increase in new work received by construction companies. The rate of expansion accelerated since February and was the strongest for 10 months. Anecdotal evidence pointed to a general rise in new project starts and greater tender opportunities across the construction sector so far in 2024.

In contrast to the positive trends for output and new orders, the March survey signalled another reduction in staffing numbers. That said, the rate of job shedding was only marginal and was less bad than in February . At the same time, subcontractor usage was stable in March. Rates charged by subcontractors increased at the fastest pace since August 2023.

Purchasing costs rose for the third month running in March. However, the rate of inflation was only marginal and the weakest seen over this period. Survey respondents noted increasing transport costs, but others suggested that strong competition among suppliers had constrained the overall rate of input price inflation.

Suppliers' delivery times shortened for the 13th consecutive month in March, albeit only moderately. Anecdotal evidence suggested that improving materials availability and subdued demand had contributed to improving vendor performance.

Construction companies remain upbeat about their prospects for business activity in the next 12 months. Nearly half (49%) of the survey panel anticipate a rise in output levels, while only 11% predict a decline. However, expectations have deteriorated noticeably: in February, 51% said they expected a rise and only 6% predicted a decline. Political uncertainty, squeezed margins and financial pressures were cited as factors weighing on optimism.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said: "UK construction output returned to growth in March as a renewed expansion of civil engineering work was supported by more stable conditions in the housing and commercial building segments. The marginal overall rise in total construction activity ended a six-month period of contraction.

"The near-term outlook for construction workloads appears increasingly favourable as order books improved again in March and to the greatest extent for just under one year. Construction companies generally commented on a broad-based rebound in tender opportunities, helped by easing borrowing costs and signs that UK economic conditions have started to recover in the first quarter of 2024.

"Staff hiring was a weak spot for the construction sector in March amid lingering concerns about margin pressures and continued risk aversion among major clients. Construction firms often reported delays with replacing departing staff, which led to a decrease in total employment numbers for the third month in a row.

"Supply chain pressures eased across the construction sector as subdued purchasing activity helped to alleviate strains on capacity. Improved supply conditions also led to a slowdown in the rate of cost inflation, which slipped to a three-month low in March."

Brian Smith, head of cost management at Aecom, said: “The construction industry’s slump has thankfully stopped short of the seven-month mark, in time for more favourable weather conditions and with some of the financial pressures it has faced in recent times easing.

“With inflation continuing to fall, the Bank of England has opened the door to rate cuts anticipated in the next few months, easing finance costs which will boost the willingness of developers to push forward with paused projects.

“There remain challenges for construction firms in the short term. An increasingly competitive tendering market is expected to remain for rest of this year and, although some input costs are falling, labour shortages and the resulting price rises are challenges that will remain.”

Atul Kariya, head of real estate and construction at accountancy group MHA, said: “While the slight rise in today’s construction PMI data is positive news and reflects improved sentiment from an admittedly low base, it is certainly not a sign of sustained recovery in the sector, and conditions remain challenging.

“Activity in the commercial sector is picking up steadily although typically contracts are continually being deferred to later in the year. Housebuilders have had a mixed 2024, with the year starting well but a subsequent dip in February and March. Despite the drop in house prices last month reported this morning by Halifax our clients are anticipating that sentiment will improve as we head into late Spring and early Summer, as it typically does every year, as pressures are easing with interest rates probably peaking, mortgage rates falling again, and material and labour costs stabilising, offering a window of opportunity to the sector.

“However, to ensure a sustained recovery for the housing industry the basic fundamentals have to change. The lack of political stability, relatively high corporation tax in comparison with competitors like Ireland, and the associated cost of capital in the UK are making it a less favourable option for real estate investors. The next government, of whatever political persuasion, needs to set out a five-year plan to support the industry and make the UK attractive to investors once again.”

Got a story? Email news@theconstructionindex.co.uk