A list of the Top 100 contractors without Carillion on it seems strange. A year ago, turnover of £5.2bn easily made Carillion the UK’s second-biggest contractor. But we all know the old stock market adage that “turnover is vanity; profit is sanity” and Carillion failed to heed it. The company imploded spectacularly at the start of this year and is now gone.

The shockwaves from Carilion’s collapse continue to reverberate and while, at a glance, the results of this year’s Top 100 suggest steady trading at the top end, the underlying picture is more complicated.

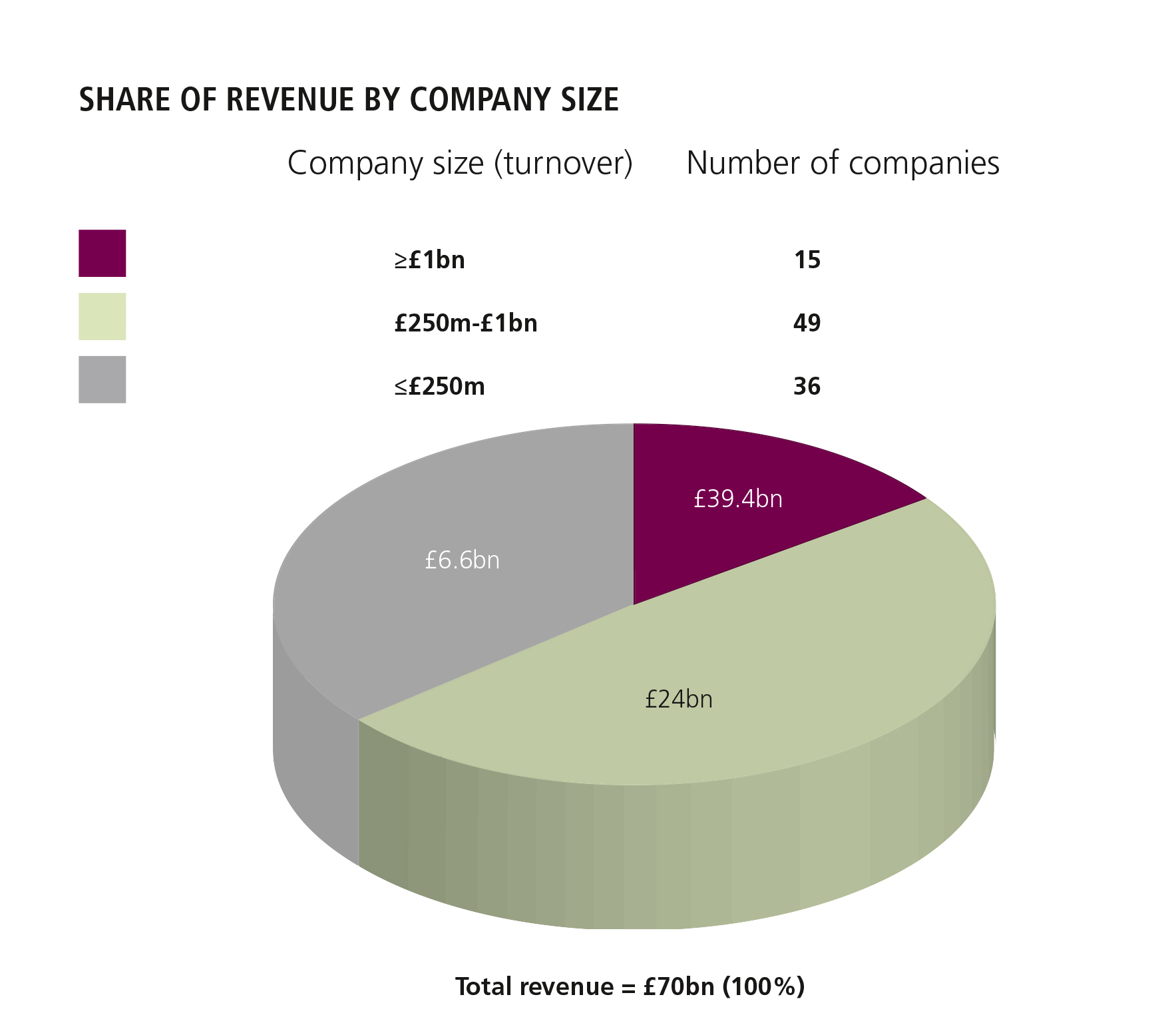

Overall, total turnover of the Top 100 was just over £70bn, 8% higher than last year. However, only 98 of this year’s Top 100 have filed accounts at Companies House for the last two years and combined revenue at those companies was up 7%.

The industry’s 10 biggest contractors generated about £32bn of revenue – 46% of the total for the Top 100 – which is broadly similar to the same ratio a year earlier.

The biggest riser was Irish contractor McAleer & Rushe, which broke into the top 50 after surging 14 places into 47th spot.

There was evidence of a tightening in social housing as two major social housing contractors – Mullaley and Durkan - nearly fell out of the latest Top 100.

Two contractors among the top 10 (Amey and Mace) recorded marginal declines in revenue, but three leading companies – Interserve, Amey and Laing O’Rourke – traded in the red.

While 77 companies of the industry’s Top 100 contractors grew turnover year-on-year in the latest set of annual results, an analysis of profitability showed a different picture.

Total pre-tax profits of this year’s Top 100 is £946.5m, compared to £833.6m last year – an aggregate rise of 15% among those companies reporting two years’ figures.

| Latest Rank By Turnover | Latest Rank By Profit | Company | Reporting Period | Latest Turnover (£m) | Previous Turnover (£m) | Change (%) | Latest Pre-tax Profit (£m) | Previous Pre-tax Profit (£m) | Change (%) | Latest Margin | Previous Margin |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1 | Balfour Beatty plc | Dec-17 | 8,234 | 8,215 | 0.2 | 165 | 62 | 166.1 | 2 | 0.8 |

| 2 | 17 | Kier Group plc | Jun-17 | 4,282.2 | 4,082.3 | 4.9 | 25.8 | -34.9 | 173.9 | 0.6 | -0.9 |

| 3 | 100 | Interserve plc | Dec-17 | 3,250.8 | 3,244.6 | 0.2 | -244.4 | -94.1 | -159.7 | -7.5 | -2.9 |

| 4 | 6 | Galliford Try plc | Jun-17 | 2,820 | 2,670 | 5.6 | 58.7 | 135 | -56.5 | 2.1 | 5.1 |

| 5 | 4 | Morgan Sindall | Dec-17 | 2,793 | 2,562 | 9 | 64.9 | 43.9 | 47.8 | 2.3 | 1.7 |

| 6 | 99 | Amey UK plc | Dec-17 | 2,581.3 | 2,591 | -0.4 | -189.8 | -43.9 | -332.6 | -7.4 | -1.7 |

| 7 | 3 | Keller Group plc | Dec-17 | 2,070.6 | 1,780 | 16.3 | 110.6 | 73.9 | 49.7 | 5.3 | 4.2 |

| 8 | 22 | Mace Ltd | Dec-17 | 2,036.9 | 2,041.1 | -0.2 | 23 | 10.7 | 114.4 | 1.1 | 0.5 |

| 9 | 98 | Laing O’Rourke plc | Mar-17 | 2,034.2 | 1,629.7 | 24.8 | -80.8 | -267.2 | 69.8 | -4 | -16.4 |

| 10 | 35 | Skanska UK plc | Dec-17 | 1,802.7 | 1,650.6 | 9.2 | 13.5 | 23.6 | -42.9 | 0.7 | 1.4 |

| 11 | 10 | Costain Group plc | Dec-17 | 1,728.9 | 1,658 | 4.3 | 38.9 | 30.9 | 25.9 | 2.2 | 1.9 |

| 12 | 48 | ISG plc | Dec-17 | 1,708.8 | 1,329.3 | 28.5 | 9.1 | 4.8 | 89.6 | 0.5 | 0.4 |

| 13 | 13 | Wates Group Ltd | Dec-17 | 1,622 | 1,531.9 | 5.9 | 32.9 | 32.9 | 0.1 | 2 | 2.1 |

| 14 | 11 | Willmott Dixon Holdings Ltd | Dec-17 | 1,296.4 | 1,223 | 6 | 33.5 | 28 | 19.8 | 2.6 | 2.3 |

| 15 | 66 | Multiplex Construction Europe Ltd | Dec-17 | 1,155.4 | 1,035.9 | 11.5 | 4.2 | 16 | -73.6 | 0.4 | 1.5 |

| 16 | 28 | BAM Construct UK Ltd | Dec-17 | 957.5 | 1,072.2 | -10.7 | 19.3 | 26.2 | -26.3 | 2 | 2.4 |

| 17 | 95 | Sir Robert McAlpine (Newarthill Ltd) | Oct-17 | 942.5 | 869.6 | 8.4 | -20.2 | -43.2 | -53.2 | -2.1 | -5 |

| 18 | 5 | Bowmer & Kirkland Ltd | Aug-17 | 928.3 | 930.7 | -0.3 | 64.4 | 61.5 | 4.8 | 6.9 | 6.6 |

| 19 | 15 | Mears Group plc | Dec-17 | 900.2 | 940.1 | -4.2 | 26.5 | 29.4 | -9.8 | 2.9 | 3.1 |

| 20 | 2 | Homeserve plc | Mar-18 | 899.7 | 785 | 14.6 | 123.3 | 98.3 | 25.4 | 13.7 | 12.5 |

(See Page 39 in the September issue of The Construction Index magazine)

Ranked fifth by profit a year ago, Balfour Beatty is now the most profitable contractor in the Top 100. In the aftermath of Carillion’s collapse, it is sobering to consider how differently things might have turned out when, three years ago, Balfour Beatty was staring disaster in the face.

Back then, Balfour Beatty was fighting off a hostile takeover bid from Carillion which, at that time, was widely assumed to be in rude financial health.

Balfour’s saviour was chief executive Leon Quinn, who came on board in 2015 to rescue the ailing giant. The latest figures show that Balfour’s pre-tax profit surged from £62m in 2016 to £165m last year, an increase of more than 166%.

Nevertheless, profitability suffered at 38 of the Top 100 contractors and some companies that featured in the Top 100 by turnover a year ago have since fallen out. Revenue halved at Canary Wharf and Solar Century, with the latter suffering from the government’s decision to cut support for renewables projects from March 2017.

With Carillion’s failure still reverberating, Brexit looming and economic uncertainty stalking the business community, the construction industry looks unlikely to lose its tag as one of the worst sectors for insolvencies.

The rising cost of materials, a worsening skills shortage, and the perennial curse of problem contracts are haunting the industry. Companies in the Top 100 are increasingly looking for a better source of income than contracting, as signs of tightness are evident throughout the industry.

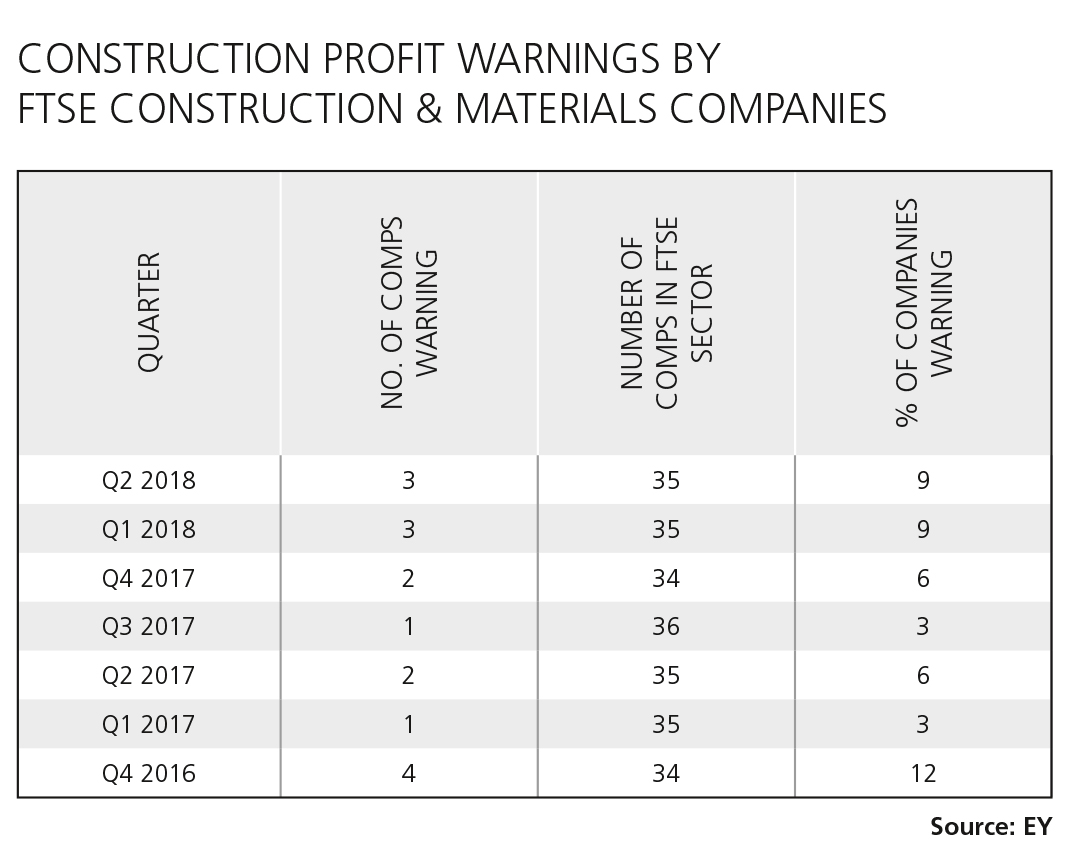

In the second quarter of this year, three of the 35 companies in the FTSE Construction & Materials sector issued warnings over reduced profits according to research from consultants Ernst & Young (EY).

EY’s head of restructuring for UK & Ireland, Alan Hudson, said: “Construction sector growth is notoriously hard to assess at any point, but especially after such a cold and wet winter. With the outlook in question, it feels like a good time to take stock and think about how construction companies can improve resilience and meet the challenges that lie ahead.”

EY was warning about legacy contracts a year ago and there has been a steady stream of profit warnings since the second half of last year, due in part to Carillion and, more recently, problems at Interserve.

At one point, Interserve – the victim of costly legacy contracts in the energy-from-waste sector – looked like following Carillion down the slippery slope. But it seems that disaster has been averted and there has since been some progress.

In the 12 months to 31st December 2017, Interserve made a massive loss – £244m – on turnover of £3.25bn. But in the first half of 2018, the company reported a pre-tax loss of just £6m, but an operating profit of £5.6m, from ongoing revenues of £396m.

Interserve has had to cut costs. The latest interim results show a £6.6m loss resulting from its exit from the London new-build construction sector, £10.8m in restructuring costs and £32.1m in ‘professional adviser fees’ connected to a refinancing deal.

Even businesses in better shape than Interserve are making significant but costly changes.

Before underlying items, Kier made a pre-tax profit of £126m in the 12 months to June 2017, which was up 8% on the previous year. However, exceptional items – mainly a £75m hit from selling consulting business Mouchel and exiting the Caribbean and Hong Kong markets – dogged the bottom line and after exceptional items the profit was £25.8m, although this was still a big rise on 2016.

In the second half of last year and free of exceptional items, these changes showed through and with no overseas work to dog the business, Kier grew profits 4%.

With the unknown intricacies of Brexit looming, working overseas seems less attractive for most major UK-based contractors these days. And while five of the UK’s top 20 contractors (Amey, Skanska, Bouygues, Multiplex and Vinci) and 17 of the Top 100 are foreign-owned, working overseas is increasingly uncommon for British contractors.

Laing O’Rourke, which has a substantial presence in the Australian market, recently sold the rail sleeper manufacturing business it had out there for £30m. Just over two years ago, the company put its entire Australian construction business up for sale, only to take it off the market again when no buyer came forward.

Asia, Europe and the Middle East provided 16% of ISG’s revenue, Dawnus works in Africa and nearly half of Keller’s annual turnover comes from North America but the ground-engineering specialist is rare in overseas outpacing UK work.

Only Balfour Beatty and Mace are looking for expansion overseas. Balfour Beatty made a £41m profit from the US in 2017 compared to £16m from the UK and £15m from its Hong Kong subsidiary Gammon.

At Mace, international revenue provided £665m of the group’s turnover of just under £2bn in 2017 and helped secure a place among the top 25 privately-owned companies in The Sunday Times Top Track 100.

Mace chief financial officer Dennis Hone said: “By the end of last year we had secured over 80% of our work for 2018, and 30% of our company-wide turnover is now generated by our international businesses. The next five years will be some of the most exciting and transformational in the company’s history, as we become the global company of choice for complex and iconic projects.”

A closer look at profit figures reveals that the average margin at the 79 contractors that recorded a pre-tax profit last year was 2.44%. At those companies that filed two sets of results, the average margin rose to 2.59% from 2.48% in the previous year. However, 13 main contractors traded in the red in their latest results and profitability suffered at 31 of the Top 100 firms.

Of the four main contractors to boast double-digit margins, three (Watkin Jones, Henry Boot and Marshall) all have property development operations, which can boost the bottom line.

Bowmer & Kirkland has a development operation, Peveril, and construction provided just 20% of turnover at Henry Boot with the balance coming from property investments. Morgan Sindall’s urban regeneration arm brought in a £6.1m operating profit on £62m of revenue in the first half of this year alone.

Earlier this year, North Midland Construction launched its own development operation, NM Investments, to utilise some ‘free-flow cash’.

With profit margins tightening, development is looking like a safer option to boost the bottom line than acquisitions, but corporate activity aimed at boosting profits has still been in evidence and not just divestments such as Kier’s sale of Mouchel. Last year, Kier bought £180m-turnover utilities contractor McNicholas and it continues to expand via acquisition in the US.

Similarly, electrical contractor TClarke uses its spare cash to fund buyouts, including a £2m acquisition of building management specialist ETON.

Like Keller, TClarke is a rarity in that it is a specialist contractor listed on the stock market; it can therefore raise funds without recourse to lenders.

The other 19 specialist contractors in our Top 100 are all privately owned. And life for them, further down the supply chain, is not getting any easier.

Back in 2013, Mears offloaded its mechanical & electrical arm Haydon to the management for £1 and three years ago had to write off £8m in expected payments from the deal. In the 12 months to June 2017, profits and turnover both fell at Haydon M&E, making Mears’ exit look timely despite the hit.

Other specialist contractors have suffered more seriously, with £50m-turnover M&E outfit Vaughan Engineering going under in June. Last month, demolition firm Cuddy entered administration and details emerged that SES Engineering – the specialist group bought by Wates from Shepherd in 2015 – is taking a hit from Carillion’s demise.

Six of the 21 specialist companies in the latest Top 100 suffered reduced profits. Utilities specialist J Murphy, for example, which is the UK’s 25th biggest contractor by turnover, saw profits virtually halved in 2017.

With turnover of £139.9m, Lorne Stewart (another M&E specialist) was one place off the Top 100 but also traded in the red; group chief executive officer Mathew Puliyelethu recently told staff: “We must continue to challenge why we are tendering projects. If we have doubt, we simply stay out.”

The Specialist Engineering Contractors group was hoping that in the aftermath of Carillion’s demise, payment conditions would improve. But despite encouraging noises coming from government, it has so far been disappointed.

SEC chief executive Rudi Klein says: “Cash flow is getting tighter and payments are getting longer. There is a lot of abuse associated with early payment and people looking to get a discount for placing bulk orders.

“Given the Carillion effect, we were hoping for some dramatic changes in payment security but nothing’s happened. The government has come out with the new construction sector deal – and no-one is complaining about that – but the industry needs to invest in skills and training. But where is the money coming form? Only the supply chain invest.”

At the 21 specialist contractors, the average margin from the latest results edged up to 2.59% from 2.56% a year earlier. As subcontractors are starting to experience slower payments, reductions in earnings and tighter margins are likely to become more common as the impact of Carillion’s collapse and other economic factors have a continued effect on a traditionally tough sub-sector.

“Construction has always been a fiercely competitive sector, which impacts on margins,” says Chris Radford, local chair at R3 (better known as the Association of Business Recovery Professionals).

“There are increases in prices of materials, particularly if they are imported,” he says. “At the same time, some of the migrant labour may be choosing to work elsewhere due to the weak pound.”

Given that most forecasts for construction growth this year are negative, the prospects for growing margins or even earnings in 2018 look slim without resorting to cutting costs or pushing up bid prices, both of which will have severe implications.

Radford adds: “Companies are set up to turn over a certain amount. A company turning over £100m but only bringing in £50m of work then has to make cuts and there are costs to those cuts. Construction companies will try to protect themselves against risk. If that continues, then the prices they are offering start to get unattractive.”

As the industry enters a period of wider economic uncertainty, achieving that balance looks set to be harder than ever and margins may be set to come down further, certainly amongst main contractors, unless attempts to grow earnings elsewhere pay off.

NOTE – The comparisons made in the text are against figures from the previous set of results, which may – due to the timing of Company’s House filings – be different to those used in last year’s Top 100. Rankings may also differ from a year ago as the previous year’s figures are restated to take into account the absence of Carillion and the inclusion of other companies.

Insolvencies are on the rise

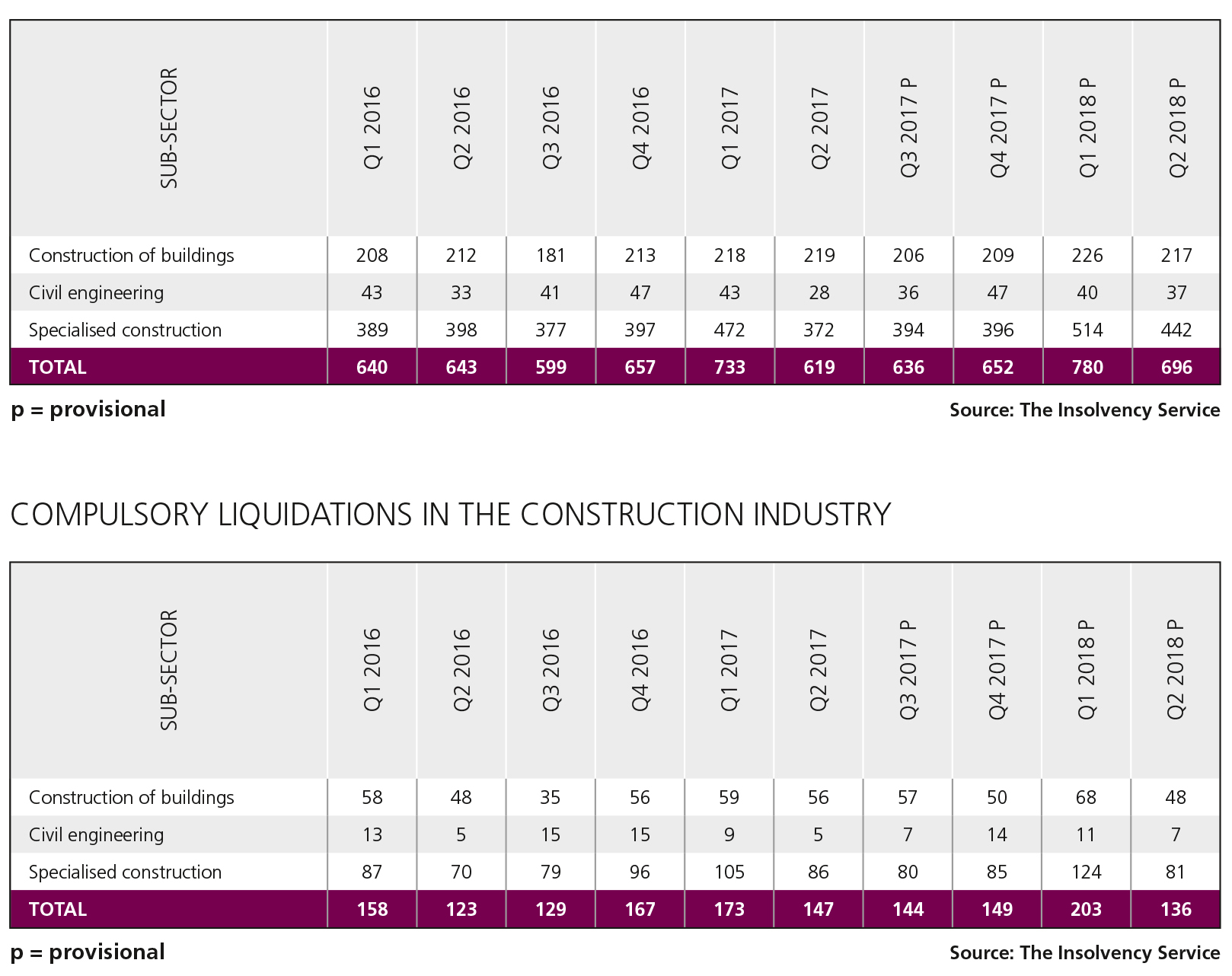

Carillion is the most obvious absentee from the latest TCI Top 100 after going bust at the start of this year. But thousands of other construction companies have also gone under in the past 12 months.

According to data from the Insolvency Service, over the 12 months to Q2 2018 there were 2,764 insolvencies in the English and Welsh construction industries, which is a rise of 3% on the preceding 12 months.

Chris Radford, local chair at R3, the Association of Business Recovery Professionals, says: “The Carillion effect goes beyond unpaid contractors. Carillion’s failure has affected the decision-making process at banks and credit insurers and suppliers are enforcing stricter credit terms.”

Construction remains the worst industry sector in the UK for companies being compulsorily liquidated.

Graham Bushby, head of financial consultancy RSM Restructuring Advisory says: “Despite a seemingly never-ending demand for new housing, not all is as rosy as it seems. Material prices have been increasing on the back of a weaker pound, and labour costs have also risen, in part due to Brexit.

“Meanwhile, property prices in many areas appear to have started to flatten. This appears to be contributing to yet another increase in the level of failures in the sector.”

The number of companies forced into liquidation is also rising, with 632 companies compulsorily liquidated in the 12 months to Q2 2018 – a rise of 3%.

Civil engineering companies appear to fare better than builders, with insolvencies virtually static, while the number of compulsory liquidations dropped 13% over the past 12 months. In contrast, specialist contractors are faring worst with a 7% rise in insolvencies and an 8% rise in compulsory liquidations.

Radford says: “A lot of construction companies rely on other construction companies. Sub-contractors are reliant on main contractors. In a normal supplier-customer relationship, there’ s a bit more stability. In construction, the supply chain is a lot more fragile. If there’s disruption to the supply chain, construction is reactive and there’s a risk to that.”

The latest data from the Insolvency Service shows that the worst affected sub-sector amongst the specialist trades is building completion and finishes, where insolvencies have leapt 13% in the last year.

Profit warnings

More profit warnings are expected from construction companies in the second half of 2018.

In the first six months of this year 17% of companies in the FTSE Construction & Materials sector warned about lower than expected profits according to research from consultant Ernst & Young (EY).

EY, which recently launched a new ‘stress index’, said: “If decision-making stalls under the weight of rising uncertainty, we expect to see further stress in FTSE Support Services and FTSE Construction & Materials, where companies would also be vulnerable to delays in government contracts and tighter labour markets.

“This would keep profit warnings at relatively high levels throughout the third quarter.”

These problems began emerging back in late 2016, when EY warned of the ‘calm before the storm’ after identifying the largest amount of profit warnings for two years amongst FTSE construction companies.

“The construction sector is vulnerable to rising costs and falling confidence, so it’s no wonder that it now finds itself in the spotlight,” cautioned EY at the time.

That spotlight has not shifted.

Quoted companies are obliged to inform the stock exchange if profits are expected to fall. Carillion warned on profits twice before collapsing. Interserve has also issued profit warnings and in Q2 2017 EY highlighted “contract issues” in the FTSE Construction & Materials sector.

“Risk has largely been transferred to contractors and more trying industry conditions are exposing problem contracts,” warned EY.

In the third quarter of 2017, EY noted a divergence between profit warnings from companies exposed to domestic pressures and those benefitting from growth in overseas markets.

“Industrial sectors would seem to be the greatest beneficiary, not just from the currency impact of Brexit but also a steadier oil price,” said EY. “The clear outliers amongst industrials are FTSE Support Services and FTSE Construction & Materials, two sectors that we’ve highlighted previously as having significant domestic contract and pricing pressures.”

This article was first published in the September 2018 issue of The Construction Index magazine, which you can read for free here

UK readers can have their own copy of the magazine, in real paper, posted through their letterbox each month by taking out an annual subscription for just £50 a year. Click for more details.

Got a story? Email news@theconstructionindex.co.uk