The companies in the latest Construction Index Top 100 had aggregate revenue in their most recent accounts of £70.6bn. That figure is down by 4.8% on the total turnover at same 100 companies in their previous accounts.

Amongst the top 10 contractors, only the top-ranked company Balfour Beatty, whose revenue is more than twice that of second-placed Kier, managed to increase its turnover.

Annual revenue fell away at a total of 53 companies in the latest top 100. While changes in accounting periods produced a bigger rise at a handful of companies, the largest year-on-year increases came mostly at smaller members of the Top 100.

J Murphy drove revenue up by 27%, while Caddick and Ardmore increased turnover by 43% and 30% respectively. Further down, Worcestershire-based Speller Metcalfe enjoyed a 56% leap in revenue but was one of 26 companies to trade in the red.

Overall, profitability worsened at a total of 57 companies in the Top 100 compared with a year ago.

Kier suffered the biggest deficit, posting a pre-tax loss of £225.3m in the year to June 2020 – the most recent annual figures available at the time of going to press – as the lockdown took its toll, but that performance was actually marginally better than in the previous year.

Both Multiplex Construction Europe and Costain also suffered significant reverses in profitability. The pressure that the industry is under is perhaps best illustrated by Balfour Beatty, where pre-tax profits slumped 65% but whose earnings were still the fourth best of the Top 100.

A year ago, combined profits at the Top 100 companies had fallen by 38% despite overall revenue edging up 2.7% but this year there was a double whammy. With combined revenue down nearly 5%, profitability in the TCI Top 100 crashed by 82%.

Profit margins reduced at 61 companies and the average profit margin across the Top 100 was just 0.8% compared to 2.3% at the same 100 companies in the previous accounts.

A year ago, three companies had double-digit profit margins but this time around only transport and waste management specialist HW Martin Holdings achieved that level.

The company was one of a number of new entrants to the Top 100 along with HG Construction, formerly known as Hunting Gate. Speller Metcalfe also broke into the Top 100 but many regional contractors continue to face stiff competition from large national contractors for work.

South-west-based Midas, one of the UK's largest and most successful regionally focused contractors, lost money for the first time in 40 years. Readie held onto the place in the Top 100 that it achieved last year, but Oxfordshire-based contractor EW Beard and Stepnell, headquartered in Rugby, both dropped out.

Government intervention such as the Coronavirus Job Retention Scheme (CJRS) helped reduce insolvencies and compulsory administrations. As a result, large main national contractors survived and payment times to subcontractors have actually improved.

During the first half of this year, the 32 leading main contractors settled with subcontractors within 34 days, which is 11 days quicker than when trade body Build UK first started collating payment data in July 2018.

The fastest payers were Vinci, Sir Robert McAlpine, Costain, Morgan Sindall, ISG, McLaren, Willmott Dixon, VolkerWessels and Robertson. On average, leading contractors paid 94% of invoices within 60 days – up from 82% three years ago – and 79% of their invoices were paid within terms, compared with 61% in 2018. This shows cash moving down the supply chain, a healthy development.

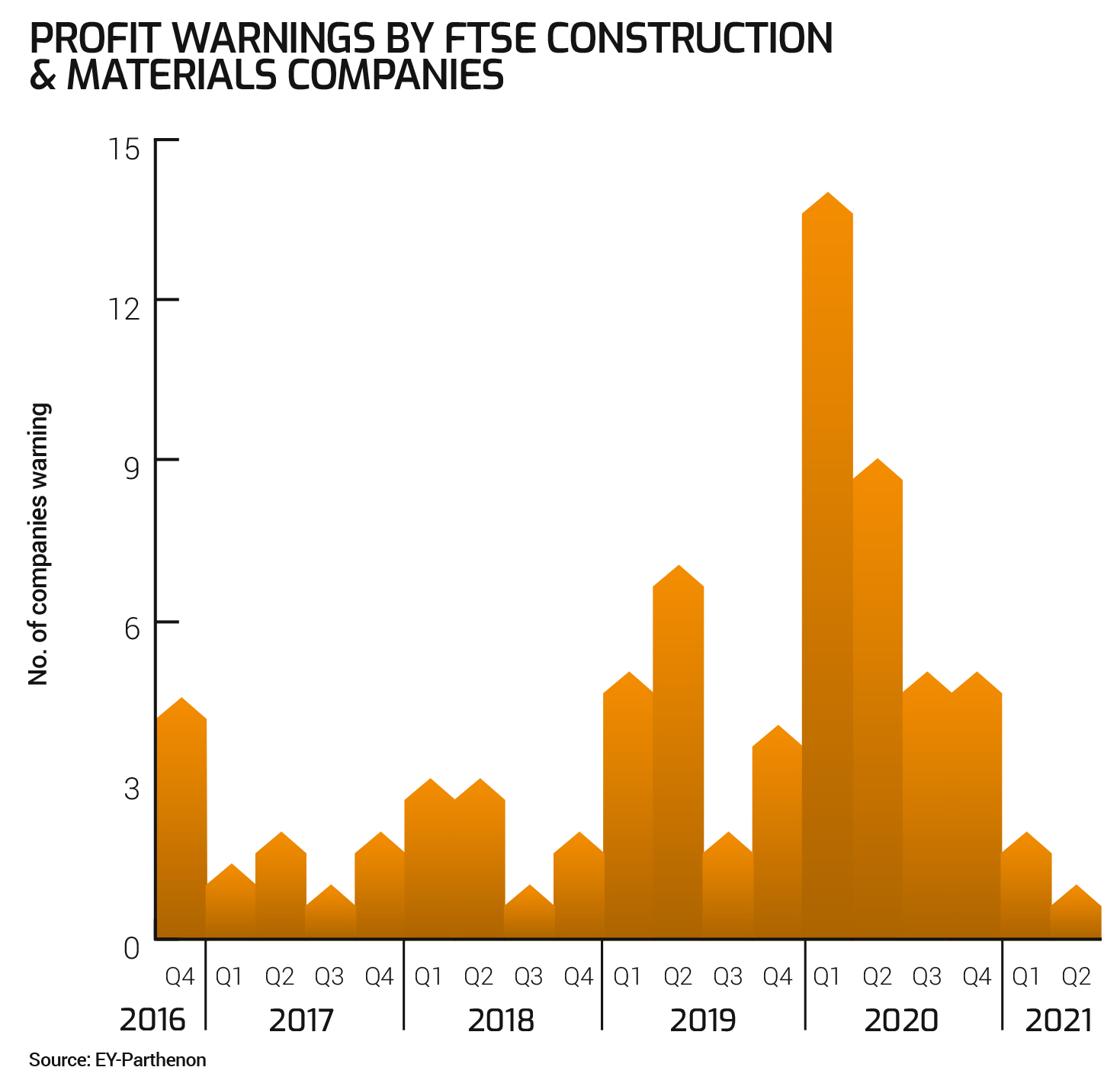

The number of construction companies warning of lower-than-expected profits also hit a five-year low in 2021 due to government support, according to EY-Parthenon, the global strategy consulting arm of accountancy firm Ernst & Young.

Despite the improved payment practices, the worst of the coronavirus-induced economic pain was felt further down the supply chain by smaller contractors whose revenues are not quite big enough to break into the TCI Top 100.

Brian Berry, chief executive of the Federation of Master Builders, said: "The past year has been enormously challenging for small to medium-sized [SME] construction firms. The pandemic has caused builders to face many operational challenges, including ensuring that sites are Covid-secure, and dealing with the shortage of construction materials which is, in part, precipitated by the lockdown restrictions."

In the second quarter of this year, there was a 42% rise in the number of building contractors going bust, according to the Insolvency Service.

In April, £40m-turnover regional civil engineering contractor Paul John Construction (Leicester) went into administration. A month later Merseyside-based highways and utility contractor Vital Infrastructure Asset Management, which claimed to be turning over £55m, fell into administration. VIAM was swiftly joined by local rival Nobles, which turned over £25m.

In June, Welsh outfit WRW, which had annual revenues of £64m, disappeared and in July Cleveland Bridge, a name synonymous with bridge building but with turnover of only £48m, was put up for sale by administrators.

As these companies collapse, there are few new companies emerging to fill the gap and start to rival the leading main contractors in the Top 100.

Many contractors are still relying on the CJRS. Rebecca Liddle, development manager for trade credit at risk managers Marsh, said: "Provisional figures show that 30% of construction companies, amounting to 72,800 entities, were still using the Coronavirus Job Retention Scheme on 30th April. This translates to 166,600 workers, or 13% of the sector's workforce, relying on the scheme. The industry also made £1.9bn of claims through the Self-Employment Income Support Scheme [SEISS]."

Just over 260,000 people were employed at the Top 100 companies according to the latest available accounts.

A significant proportion of employees at big contractors such as Keller, Interserve and ISG are based overseas, but this figure still shows the scale of employment provided by the industry's leading companies.

Overall, the total number of employees at the Top 100 was down by 3.7%. Wages and salaries also reduced but the decrease was far smaller at 1.4% as companies sought to use the CJRS to retain their workforce.

The average annual wage across the Top 100 companies was £44,396, which is actually up by 2.4% on the median (£43,332) for the previous year at the same companies.

This can be partly explained by the 27 companies with accounts available for 2019 as The Construction Indexwent to press. There were also 14 companies that had filed accounts up to the first quarter of last year, when the impact of the Covid-19 pandemic was just becoming evident and the notion of being put on furlough was still in its infancy.

Working out which companies used the CJRS the most will only become apparent further down the line but during 2020 Morgan Sindall claimed £9.5m from HMRC then repaid £7.7m later last year.

Such is the nature of the government tax system that Morgan Sindall paid £1.8m in corporation tax on receiving the furlough but the £7.7m repayment is not tax deductible. A fuller financial picture will emerge both when the government support ends and when more recent accounts appear.

Another impact of the pandemic was that some major contractors, such as Osborne and Robertson, took the opportunity to extend or change their reporting period to further digest the impact of the pandemic.

"We are mindful that like many other organisations the impact of Covid-19 has significantly impacted auditors' resources and their ability to complete work, having a backlog of audits to complete for other clients," explained a spokesperson for Osborne.

"We have therefore taken the prudent measure of extending our accounts filing deadline to the end of September 2021."

Most of that period will include the strongest spurt of economic growth since the bounce-back after World War Two, according to the Bank of England. However, if the bank's forecast of 7.25% growth in 2021 materialises, this will follow in the wake of a 9.9% slump in 2020, which was the economy's sharpest contraction in 300 years.

Next year's Top 100 will include many more accounts for companies caught in the eye of the Covid-19 storm and show an industry that appears to have weakened further, while demand has bounced back rapidly.

In June 2021, the industry grew at its fastest rate in 24 years according to the bellwether IHS Markit/CIPS UK Construction PMI Total Activity Index.

The Glenigan Construction Industry Forecast 2021-2023 predicts that the industry is set to return to pre-Covid levels by 2022 with underlying project starts (under £100m) up 3% above 2019 levels.

Private and public housing, hotel and leisure and government-backed spending on schools and health are all expected to produce strong growth next year.

In the short term, inflationary pressures are lingering that could wreak further short-term financial damage. The Chartered Institute of Purchasing & Supply (CIPS) index recorded its first slowdown of the year in July as materials shortages and a lack of subcontractors hampered growth.

CIPS director Duncan Brock said: "The pervasive weaknesses in supply chains along with a lack of staff and contractor availability were laid bare as construction lost some of its get-up-and-go. The rampant rise in prices for raw materials and transportation continued to be the construction's heavy load along with historically long delivery times."

At the coalface, leading main contractors agree that inflation and shortages pose the biggest threat to immediate financial performance.

Karen Booth, chief financial officer at ISG, says: "Short term, it's the inflationary pressure from material shortages that is causing some issues across the industry. Much of this is directly linked to the impact of Covid-19, and production lines either being halted or significantly impacted by necessary restrictions.

"The more positive news is that we believe that by Q4 we should start to see reducing pressure as production facilities revert to normal operating conditions. We may also see wage inflation depending on the precise nature of the EU withdrawal deal, that currently remains under negotiation, and how this impacts the ease of movement for European workers.

"This could have a direct impact on certain disciplines within the supply chain. A further area we are closely monitoring relates to insurance costs. Professional indemnity costs are rising as a result of widespread cladding remediation claims and this is having a disproportionate impact on the supply chain, which may result in suppliers being forced to operate without PI cover – something that we are closely monitoring with our supply chain partners."

Another concern is the impact on cash balances of the changes to VAT repayments, which started in March. Since the implementation of the reverse-charge VAT rules, main contractors have had to pay the VAT on their subcontractors' bills directly to HMRC. Previously, they would have paid this amount to the subcontractors, who were then responsible for paying HMRC.

"That would have provided subcontractors with one to three months cash before they started to pay it back," explains Graham Dundas, chief financial officer at Willmott Dixon, who worries about the impact of the new VAT rules as well as other looming financial pressures.

He adds: "People have to start repaying furlough loans so we could have some challenging times. The industry needs a healthy pool of supply chain partners."

There are just eight subcontractors on the latest Top 100 and little sign of any other sizeable specialists waiting in the wings.

The old industry adage of cash being king will never be more important than in the months ahead at all levels of the industry from sub to main contractors, particularly as the industry's risk levels and low margins are not encouraging lenders.

Dundas adds: "Generally lenders are looking to reduce the debt they are owed from construction. There have been some high-profile failures in the past and those people that have been hurt are less keen to underestimate construction debt."

As the government takes away the blanket that has supported the industry through the worst of the Covid-19 pandemic, meeting the demand that appears to be out there will be the challenge in the immediate future.

Profit warnings

The number of warnings by companies that profits will be lower than expected has hit a five-year low due to a combination of strong demand and the government's furlough scheme.

More than 40% of listed construction companies issued a profit warning in the 12 months to Q1 2021, but there were only three alerts in the first half of 2021 and only one – from contractor NMCN – in the second quarter according to research by Ernst & Young's strategy consultancy EY-Parthenon.

"In just over a year, we've recorded both the lowest and highest quarters of profit warnings in over 21 years of EY analysis," says Alan Hudson, head of UK & Ireland turnaround and restructuring strategy at EY-Parthenon.

"EY recorded similar dips in 2002/3 and 2009 after 9/11 and the global financial crash, respectively. Markets tend to over-correct and last year's drastic expectations reset, combined with a better-than expected recovery and government support, have helped all but a handful of companies to beat depressed forecasts. But history also shows us that companies and markets can also underestimate the challenges of recovery."

EY is warning about demand outstripping the supply of raw materials, haulage, shipping, and labour. A mild Baltic and Scandinavia winter reduced timber availability, while high levels of demand for long-steel have combined with Covid-19 production constraints — including high oxygen demand — to create a global shortage.

"Existing projects are continuing, but a near doubling of prices year-on-year — and the move by suppliers to 'order by allocation' — puts new projects at risk," warns EY in its latest profit warning report.

Inflation clauses in contracts can help companies weather short-term price increases but, if prices stay high and shortages continue, pressure will grow on cash reserves and credit insurance.

Ian Marson, construction leader at EY-Parthenon UK&I, says: "The government's 'build back better' initiative will help underpin recovery in the sector, but the end of other support measures could put extra pressure on some suppliers' working capital. The recently introduced domestic reverse VAT charge for construction services, IR35 tax changes for employing contract workers, and the tightening of supply chain credit financing could also add further strain. Large contractors will need to maintain visibility over key parts of their supply chain."

With furlough starting to unroll and prices rising, the number of profit warnings may not stay at such a low level over the rest of this year.

Regional contractors

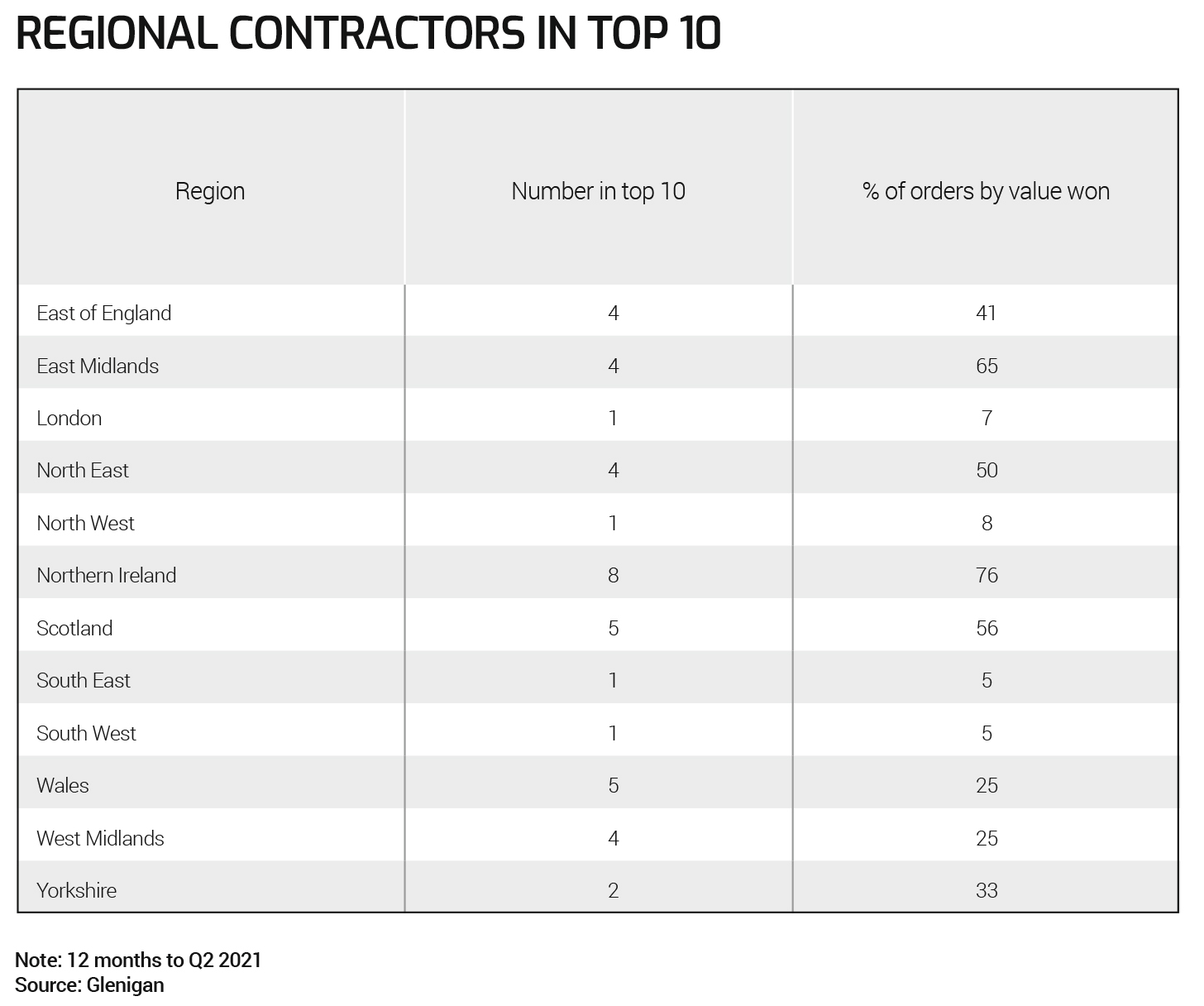

Regional contractors are being squeezed by national contractors in the race for work as the industry emerges from the worst of the pandemic.

Two thirds of the companies ranked among the top 10 contractors in the UK's dozen economic regions are national contractors according to research by building information specialist Glenigan.

"The past year has been enormously challenging for small to medium-sized (SME) construction firms," says Brian Berry, chief executive of the Federation of Master Builders.

In some regions, such as the north-west and the south-east, nine out of 10 contractors in the regional top 10 by orders in the 12 months to Q2 2021 were national players, such as Balfour Beatty, Kier and Morgan Sindall.

Glenigan's research shows that only a third of the work won by the top 10 contractors in this period has been awarded to regional contractors.

Some regional players have succeeded in growing into sizeable companies, such as Elgin-based Robertson, which tops the table in Scotland. Here, half the top 10 contractors are native outfits.

In Northern Ireland, the Ulster construction scene remains dominated by native firms; Welsh contractors also appear to be competitive although WRW – a fixture in the top 10 construction companies in Wales – collapsed into administration in July.

The plethora of major projects in London means that the capital is unsurprisingly dominated by national players but in areas such as Yorkshire and the south-west only a handful of local contractors are retaining market share.

Midas is one of the most successful contractors in the south-west but posted a loss for the first time in 40 years in its latest accounts.

In the north-east, regional lobbying group Construction Alliance North East has updated its Intelligent Procurement policy to encourage clients to create fairer processes to allow local SME contractors to win more work.

In addition to fairer procurement processes, regional SMEs are also asking not to be overlooked in favour of national contractors in the battle for essential materials.

"The materials shortage is the biggest headache for small building firms, with 93% of my members reporting material price increases," adds Brian Berry. "It is essential that materials are made available to the small, independent builders merchants in addition to larger infrastructure projects so that all parts of the construction sector are supported."

Insolvencies

Industry experts warn that contractors that have neglected to keep a tight rein on their cashflow will be in urgent need of finance as government support that kept them afloat throughout the pandemic winds down.

There was a 35% fall in the number of construction companies in England and Wales becoming insolvent in the 12 months to Q2 2021; just 1,801 companies were declared insolvent over this period according to the Insolvency Service. But the most recent quarter, ending in June 2021, saw a 48% surge in solvencies and worse could follow.

Rebecca Liddle, development manager for trade credit at risk manager Marsh, warns: "The construction industry is … likely to face significant financial pressures in the coming months as government interventions introduced in the pandemic end.

"The construction sector has heavily utilised government financial provision during the pandemic. HMRC said construction companies claimed just under £1.2bn for furloughed staff over six months to April 2021.

"Without this help, it is likely that a large number of building companies would have collapsed, as the pandemic took hold. Therefore, the unwinding of this support will present the sector with huge challenges, with ready and affordable finance needed to replace this borrowing to aid short-term liquidity."

A rise in construction insolvencies had been widely expected but compulsory liquidations, which shrank by two thirds in the 12 months to Q2 2021, remain low. Just 24 contractors were compulsorily liquidated in the latest quarter, but increased borrowing may be all that's keeping some companies afloat.

Julie Palmer, a partner at business advisor Begbies Traynor, says: "Covid has dramatically accelerated the UK's zombie business population, with many businesses taking on unsustainable government-backed debts during the pandemic in order to survive. With constant changes to the UK roadmap out of lockdown, many remain in a precarious position, with any future lockdowns likely to impact insolvency rates."

Begbies Traynor's red alert system, which monitors companies in financial distress found that the number of construction contractors in significant distress in the 12 months to Q2 2021 was up 26% on a year earlier.

Zombie contractors with no cash are more likely to take on work on wafer thin margins and would struggle to survive any contractual disputes, which would have a knock-on effect on both insolvencies and compulsory liquidations.

The TCI share index

Shares in contractors quoted on the UK stock markets remain below pre-pandemic levels according to exclusive research for The Construction Index.

Contracting shares enjoyed a strong run at the end of 2019 and hit a high point in February last year, just as the coronavirus was spreading across the world and into the UK.

The first lockdown then hit the wider UK economy and the TCI share index, which is produced exclusively by Refinitiv, collapsed by 40% over the next month.

A subsequent rally over the next 12 months saw the index leap by 57% but investor sentiment in quoted contractors has subsequently weakened.

More lockdowns, fears over Brexit, material delays, skills shortages and the suspension in trading of shares in NMCN in June after the civils contractor delayed posting its annual results have all dogged contracting share prices.

By this summer, the TCI share index was down by 13% on last year's high and still 5% below the level at the start of last year before the pandemic emerged to savage the economy.

The construction rich list

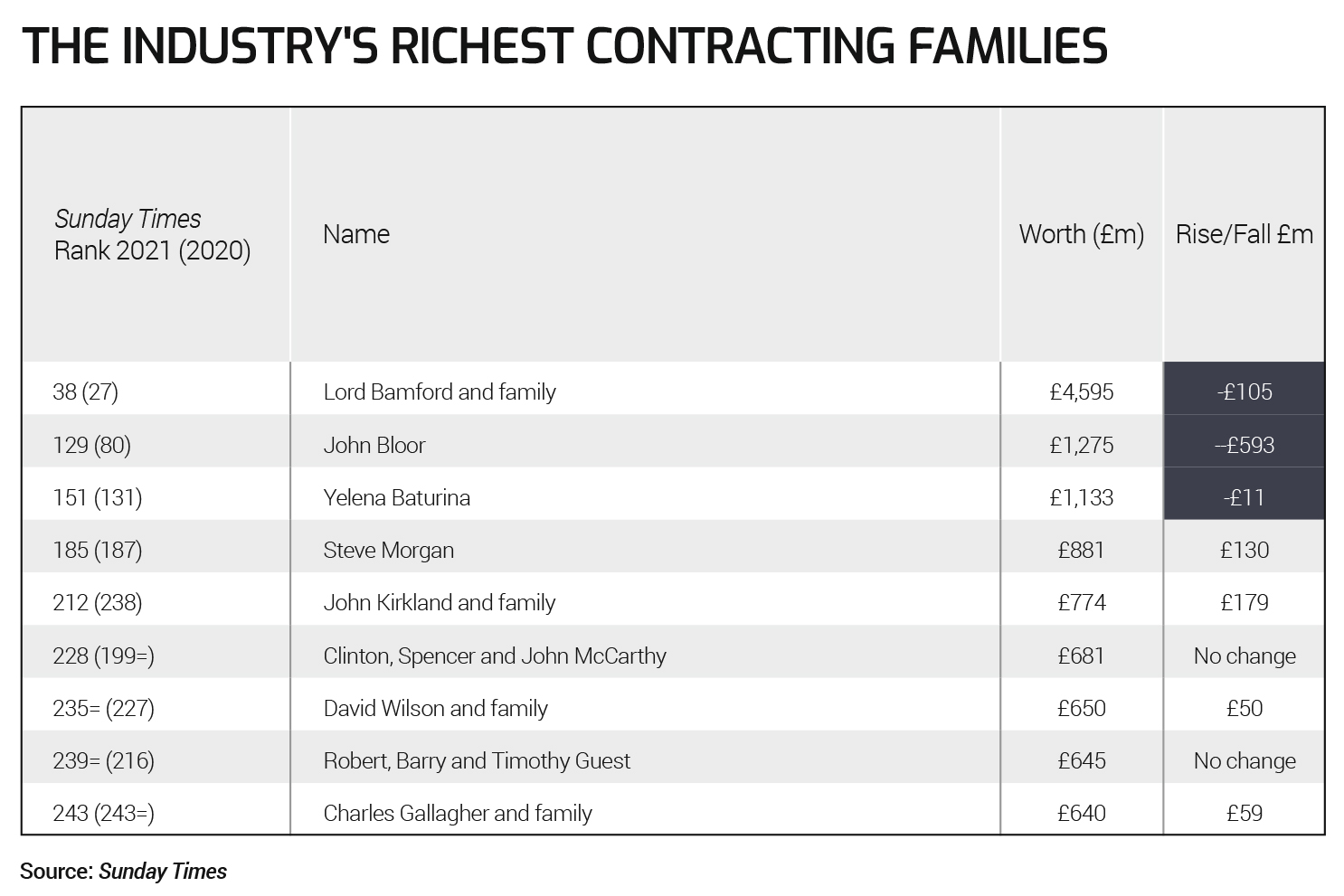

Just nine of the UK's 250 richest people have derived their wealth from the construction industry according to the latest Sunday Times Rich List.

There is now only one person with a construction connection in the top 100, and just one contractor in the entire top 250.

John Kirkland and his family, who control Bowmer & Kirkland, remain the richest contracting family. Their wealth grew by £179m to £774m last year meriting a rise of 26 places on the Sunday Times list to 212.

The only person in the top 100 who can be said to derive his wealth from the construction industry is Lord Bamford (and his family) of construction equipment manufacturer JCB.

Nevertheless, Lord Bamford's wealth shrank last year, as did that of John Bloor, who owns the Triumph motorcycle business as well as the house-building company that bears his name. Bloor tumbled out of the Top 100 after his wealth shrank by £592m to £1.275bn.

There has been a mixed impact on the wealth of people involved in the construction industry from the Covid-19 pandemic. The three richest construction families all endured a reduction in their wealth, but Moscow-born construction magnate Yelena Baturina suffered far less than Lord Bamford or John Bloor.

Baturina – who's that? If you're unfamiliar with the name, that's because most of Baturina's wealth comes from a Moscow-based construction firm, Inteco, and a manufacturer of construction membranes, Hightex, based in Germany. But Baturina is a UK resident and for that reason, she makes the cut. Baturina's wealth (around £1.2bn) declined by only 1% last year.

Meanwhile, the booming UK housing market helped a number of house-builders onto the Sunday Times' list of the 250 richest people.

Redrow founder Steve Morgan was £130m richer at the end of last year with a fortune of £881m. The wealth of McCarthy & Stone co-founder John McCarthy and his sons Clinton and Spencer was unchanged, but Wilson Bowden founder David Wilson and house-builder Charles Gallagher were both better off.

The wealth of the Guest family, who sold their plumbing supplies business, John Guest, to Reliance Worldwide Corporation in 2018, was also static for a second year at £645m.

With the Rich List now reduced to 250 people, the current wealth of Kathy and John Murphy of the eponymous contracting group remains unassessed. In 2020, the Murphys' wealth was rated at £440m and they were on the verge of the top 300. Their wealth has not increased enough to join the new abbreviated Rich List.

Read more in the September magazine order online.

Got a story? Email news@theconstructionindex.co.uk

.gif)