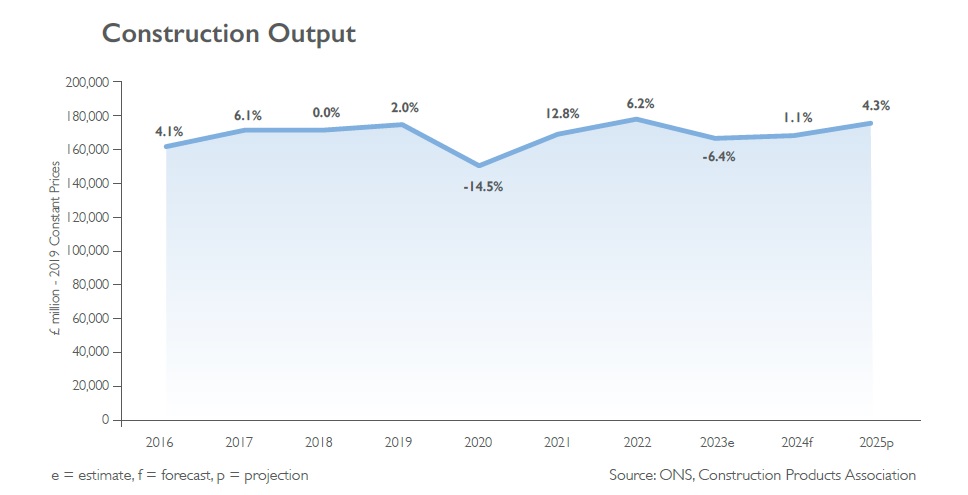

The Construction Product Association’s 2023 Spring Forecasts predict GB construction output will fall by 6.4% this year and rebound by just 1.1% next year.

Three months ago, the Construction Products Association (CPA) was forecasting a 4.7% fall this year and a 0.6% rebound in 2024.

The past few CPA forecasts have seen each gloomier than the one before.

The CPA says that its latest forecasts downgrade is driven primarily by sharp falls in the two largest construction sectors – private new housing and private housing repair, maintenance and improvement (RM&I) – together with recent government announcements of delays to major infrastructure projects.

Private housing new build, and private housing RM&I account for around 40% of total construction output and are forecast to be the sectors in which demand is most affected by a macroeconomic backdrop of falling household incomes and higher interest rates. In infrastructure, the third-largest sector, growth is expected but has been downgraded from the Winter Forecasts owing to government delaying HS2 work at Euston station and work on major road schemes.

A wider recovery in economic growth in 2024 is expected to boost demand for both new build housing and RM&I activity, and total construction output is forecast to return to growth, although rising by only 1.1%.

Private housing is the sector forecast to experience the sharpest contraction in 2023, with a 17.0% fall in output in 2023. Following the Liz Truss/ Kwasi Kwarteng mini budget in October 2022, which led to interest rates rising to a 14-year high, prompted a significant weakening in homebuyer sentiment and a sharp drop in demand. Continued pressure on household budgets and the absence of stimulus for homebuying in the March 2023 budget means that demand from a key segment of the market will remain subdued, the CPA says.

Before that seminal mini budget last autumn, the CPA had been forecasting a mere 0.4% decline in GB construction output in 2023.

The latest forecasts assume a pick-up beginning in the traditional spring selling season with mortgage interest rates settling at current levels – lower than at the end of 2022 but still higher than 12 months ago and the ultra-low rates of the last decade. However, a gradual improvement in demand will need to be maintained throughout the summer and beyond to give house-builders confidence to start new developments and drive a recovery in building activity in 2024.

Private housing RM&I is hit by the twin effects of inflation – causing a fall in real incomes – and the fading impact of the one-off boost to activity during and immediately after the pandemic. During the pandemic lockdowns, many people had more time for home improvements and a desire to create home-office space.

A drop in planning applications in the second half of 2022 and the return of competing spending decisions such as overseas holidays point to a reduced pipeline of improvements work and discretionary R&M projects for this year. This is partly offset by strong activity on energy efficiency retrofit and solar/PV work.

As a result, output is forecast to fall 9.0% in 2023 before a broader economic recovery that should drive output growth of 2.0% in 2024, the CPA predicts.

In infrastructure, forecast growth rates have been downgraded in the Spring Forecasts to 0.7% for 2023 and 1.2% for 2024, down from 2.4% and 2.5% respectively in the Winter Forecasts three months ago. Activity on regulated frameworks in water & sewerage, road works and railways provides sizeable activity, but growth in the sector tends to be driven by large projects, most recently by HS2, the Thames Tideway Tunnel and Hinkley Point C. Nonetheless, in the space of six months the UK government has gone from announcing it would bring forward 138 infrastructure projects to start by the end of this year to cancelling this and delaying HS2 Phase 2a and Euston station, the Lower Thames Crossing and other roads projects by two years in an attempt to reduce near-term government spending. HS2 Phase 2a is beyond the scope of the forecasts and previous forecasts had factored in delays and cost overruns on current phases, but the pause of work at Euston, for which preparatory work had begun, will adversely affect activity during the forecast period, the CPA says.

Construction Products Association head of construction research Rebecca Larkin said: “Despite the improvement in the outlook for the UK economy compared to six months ago, the headwinds of falling real incomes and interest rate rises remain. For construction, the most acute effects of this will be felt in the two largest sectors of activity and those that are most exposed to a slowdown in discretionary household spending: private housing and private housing RM&I. The sharp falls that are forecast for housing in 2023 mean that overall, a construction recession will be unavoidable. However, it is important to emphasise that the starting point is a record-high level of activity and the 6.4% contraction expected is smaller than during the construction recessions of 2008/09, 2012 and 2020.

“In previous years, infrastructure activity has helped cushion falls elsewhere, but recent government announcements delaying HS2 work at Euston station and on major roads schemes including the Lower Thames Crossing have weakened the near-term growth prospects for the third-largest sector of construction. Unlike the relatively fast bounce back that is expected in housing in 2024, the prospect of delays leading to even greater cost overruns on large infrastructure projects poses a risk to longer-term activity. This shines a light on the government’s decision to keep capital spending budgets unchanged in cash terms from 2024/25.”

Got a story? Email news@theconstructionindex.co.uk