However, business expectations reached a six-month high on hopes of a boost from infrastructure work.

After the problems of spring, the IHS Markit/CIPS UK construction total activity index reached a near five-year high of 58.1 in July but slid back to 54.6 in August. Survey respondents mostly suggested that a lack of new work to replace completed contracts had acted as a brake on the speed of expansion.

Any figure above 50.0 indicates growth in output over the previous month and each the past three months has seen output grow, but the latest expansion was the weakest over this period.

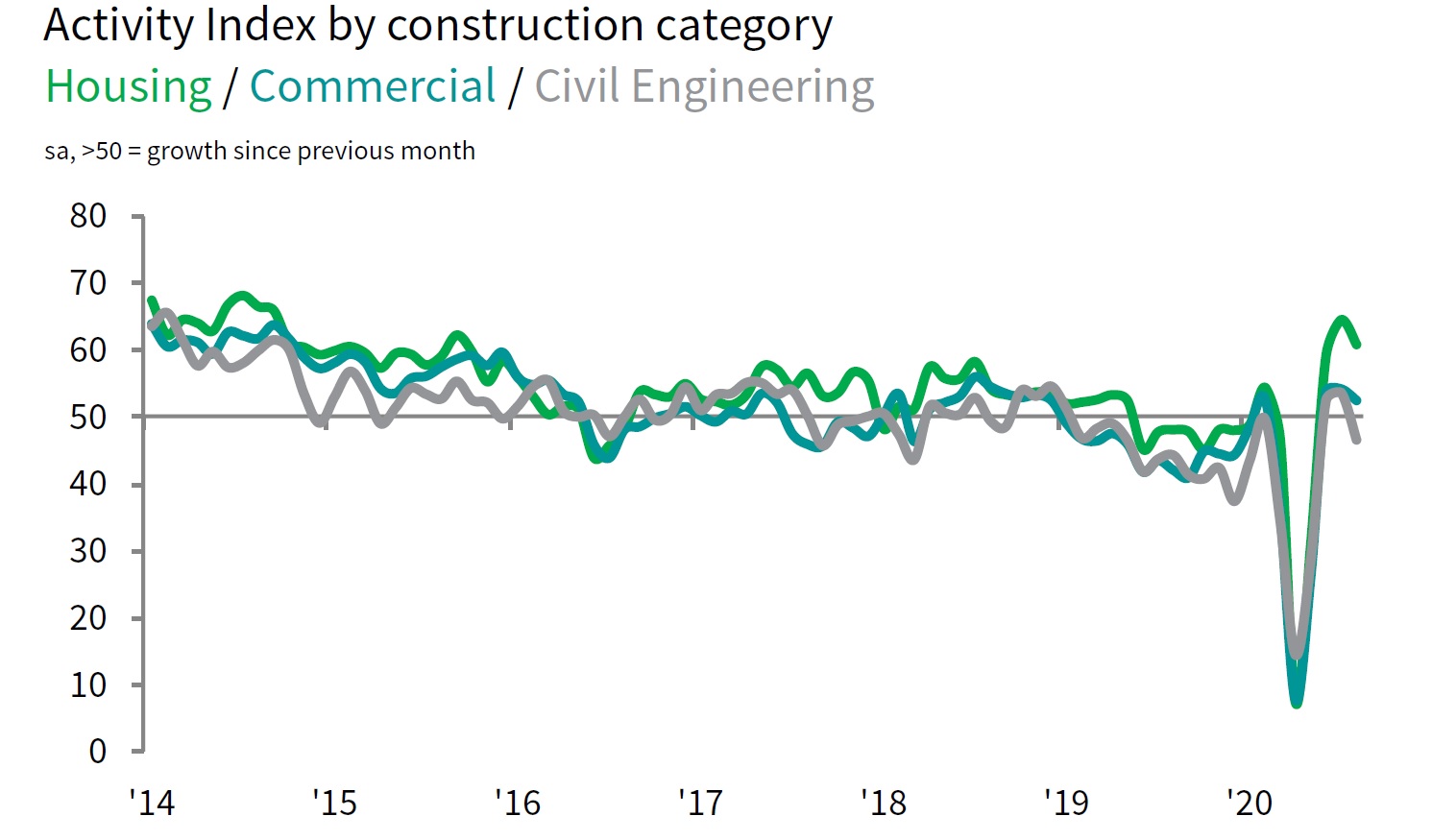

House-building has registered the strongest rebound since the stoppages of work on site in late-March due to the coronavirus pandemic, but then it was also hardest hit by the lockdown. This trend continued in August, with the seasonally adjusted Housing Activity Index posting well inside expansion territory (60.7). The equivalent figures for commercial work (52.5) and civil engineering activity (46.6 – hence a decline on July) were notably weaker than the headline index in August.

Total new business volumes increased for the third month running during August, but the rate of expansion remained only modest and slowed since July, the survey found.

Supply chain disruption persisted across the construction sector, which led to another sharp downturn in vendor performance. Stock shortages and an imbalance of supply and demand for construction inputs contributed to higher purchasing costs. The overall rate of input price inflation was the highest since April 2019.

Despite reporting subdued new business intakes since the start of the pandemic, construction companies reported an improvement in their business expectations for the year ahead. More than twice as many survey respondents (43%) expect a rise in construction output over the next 12 months as those that anticipate a fall (19%). This was often linked to hopes of a boost from major infrastructure projects and resilient public sector construction spending.

However, an expected rise in business activity could not prevent a further drop in staffing numbers. The rate of job shedding eased only slightly since July and remained among the fastest seen over the past decade.

Tim Moore, economics director at IHS Markit, which compiles the survey, said: “The latest PMI data signalled a setback for the UK construction sector as the speed of recovery lost momentum for the first time since the reopening phase began in May. House building remained the best-performing area of construction activity, with strong growth helping to offset some of the weakness seen in commercial work and civil engineering activity. The main reason for the slowdown in total construction output growth was a reduced degree of catch-up on delayed projects and subsequent shortages of new work to replace completed contracts in August.

“Another month of widespread job shedding highlighted the ongoing difficulties faced by UK construction companies, with order books often depleted due to a slump in demand from sectors of the economy that have experienced the greatest impact from the pandemic.

“More positively for the employment outlook, business expectations climbed to a six-month high in August as construction firms turned their hopes towards a boost from major infrastructure work and reorienting their sales focus on new areas of growth in the coming 12 months."

Chartered Institute of Procurement & Supply director Duncan Brock said: "The momentum in the sector’s recovery hit a bump in the road in August with a sudden slowdown in output growth and tender opportunities, while employment trends remained the most fragile in a decade.

"This stalled progress was not a surprise given the warning signs last month that any hard-won progress could start to fizzle out. As new order gains slowed across all sectors, continuing COVID-19 anxiety amongst clients meant many projects still remained on ice. Though residential building remained the strongest, it too was showing signs of strain.

"In addition, there were ongoing difficulties in supply chains which hampered the sourcing of raw materials. Delivery times lengthened in August as a result of stock shortages at suppliers and cost increases were the highest since April 2019.

"Even with all these obstacles, builders were at their most optimistic since the beginning of the year. This glass half full attitude will have to carry companies into the autumn as the UK economy remains delicate and susceptible to more turbulence."

Jan Crosby, UK head of infrastructure, building and construction at KPMG, said: “August’s construction PMI may have pointed to an easing of output growth, but at least the positive momentum continues and there remains a sense of optimism.

“As is clear in the latest figures, residential continues to be buoyed by the underlying demand for housing, driven by moves as families grow, moves to rural rather than urban living and the massive need for affordable key worker housing. Pricing levels are being maintained and in some areas are even rising, with rates of sale at high levels too. How long this will last is of course a key question, but notwithstanding the rising unemployment levels, people still need accommodation and if history is anything to go by, wholesale planning changes are likely to temporarily slow land release in the short term and keep pricing stable even if demand slows. The stamp duty holidays were not needed, instead the focus should be on shovel ready infrastructure projects, including hospital builds as well as key worker and affordable housing programmes facilitated with rapid modular builds.

“Logistics and infrastructure construction, such as highways and rail, still remain hot sectors and increasingly we may see opportunities in regeneration too – both of our high streets and converting bricks and mortar retail to other use classes, for example. Contractors are also looking at partnerships with institutions to develop core investment buildings, whether it be student accommodation, build to rent, senior living, affordable housing, data centres or logistics facilities.”

Got a story? Email news@theconstructionindex.co.uk