The Construction Products Association (CPA) says that the construction industry will experience an acute recession this year driven by double-digit falls in private housing new build and private housing repair, maintenance, and improvement (RMI) – the two largest sectors of the construction industry in the UK.

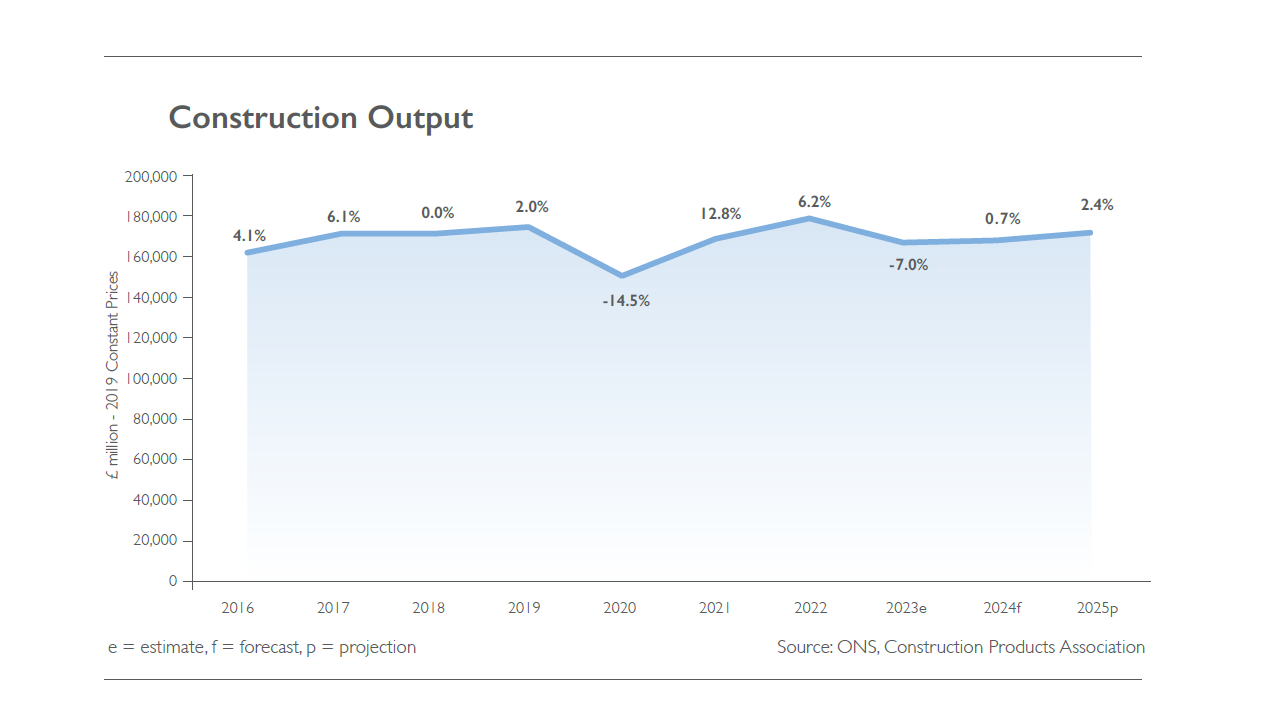

UK construction output to fall by 7.0% in 2023 before recovering slowly in 2024 with growth of just 0.7%, according to the CPA’s Summer Forecasts published today.

These latest forecasts are in stark contrast to what the CPA was predicting this time last year. Twelve months ago the CPA said that construction output would grow by 1.6% in 2023 and a further 2.5% in 2024. But that was before Liz Truss had a go at being prime minister and before Russia invaded Ukraine – two economic shocks that no one had predicted.

Since last summer the CPA’s quarterly forecasts have got successively gloomier. In February this year it was saying that output would decline by 4.7%, then by 6.4% in May and now 7.0%.

The lesson being that all economic forecasts should be taken with a bag of salt.

With the UK economy as it now is, the CPA says that demand for both new housing and improvements works will continue to be hit hard. Infrastructure activity, by contrast, is expected to remain at high levels due to major projects already down on the ground. Even in this sector, however, output is likely to fall marginally compared to last year following the government announcing delays to roads and rail projects.

Private housing output is worth £41bn a year to the UK economy and is forecast to be the worst affected construction sector in 2023. In this sector, activity was already forecast to fall due to the lagged impacts of the Truss/Kwarteng mini budget in September 2022 and the resultant spike in mortgage rates, which led to a 30-40% fall in demand in the final quarter of the year. Demand started to recover during the first quarter of this year as mortgage rates fell, but then the Bank of England raised interest rates once again.

The CPA says that house-builders are likely to continue focusing on completions to meet the lower levels of demand rather than start new developments. House-builders are not only facing reduced demand but also planning impediments, including nutrient neutrality demands. Overall, private housing starts will fall by 25% in 2023, the CPA predicts. Completions and output are expected to fall by 19% before a recovery starting in the second half of next year, which will see a rise of 2% in 2024 overall.

Private housing RMI is worth £29bn each year to the UK economy and activity reached historic highs between 2020 and early 2022 due to increased working from home and the so-called ‘race for space’. Since March 2022, however, activity has been falling due to persistent inflation, rising interest and mortgage rates, and falling real wages. Fewer people have the spare cash to fix up the house. Evidence of this comes from the monthly reports of sales from members of the Builders Merchant Federation. Sales volumes are down this year and while initially revenue continued to rise because of rising prices, this is now in decline.

The decline in private housing RMI has been softened by growth in energy-efficiency activity, such as insulation and solar panels, as homeowners with substantial savings take action to combat spiralling energy bills. This work is also likely to remain strong this year, the CPA says, although government schemes for energy-efficiency retrofit of the existing housing stock such as ECO4 and ECO+ – now rebranded as the Great British Insulation Scheme – appear to be missing their targets once again. Larger home improvement activity remained strong last year but planning applications for new larger home improvements fell by 19% in 2022, suggesting a fall in activity this year. Overall, private housing RMI output is forecast to fall by 11% this year before growth of 2% in 2024, in line with an expected recovery in household finances.

Infrastructure activity remains strong due to major projects such as HS2, the Thames Tideway Tunnel and Hinkley Point C. These projects are all late and overbudget, the CPA notes, but continue to provide growth to a sector worth £28bn a year. Higher activity from these projects is likely, however, to be offset by government delays to new roads and rail projects. In addition, budgetary constraints for councils, combined with cost inflation issues, are likely to mean a decline in the volume of local transport work.

Due to recent concerns over the quality of rivers across the country, water companies intend to accelerate delivery on 31 investment schemes between 2023 and 2025, which may contribute activity to the sector. The CPA is sceptical, however. “There remain serious questions over whether this will see a major uplift to infrastructure output in the near-term given skills and products availability as well as financial issues at companies such as Thames Water,” it says.

As a result, infrastructure output will fall by 0.5% in 2023, before growth of 1% in 2024.

CPA economics director, Professor Noble Francis said: “More than half of construction activity is provided by the three largest sectors: private housing new build, private housing RMI and infrastructure. Both housing new build and RMI had already taken a hit in 2022 Q4 due to falling real wages, the rising cost of living, economic uncertainty, and the effect of the government’s calamitous mini budget on mortgage rates. Further interest rate and mortgage rate rises this year, as well as falling real wages, are likely to lead to sharp falls in demand within the house building and improvements sectors. Exacerbating this for the construction industry are government announcements of delays to roads and rail projects, despite infrastructure activity remaining relatively high.

“The government’s previously stated ambitions – building 300,000 net additional homes per year, investing £600bn in an infrastructure pipeline, delivering Levelling Up, and transitioning to net zero – all sound like hollow soundbites now given its lack of commitment and investment. It is essential that government uses its autumn statement later this year to invest in UK construction – an industry that employs more than three million people across its supply chain and provides the homes and infrastructure that are so vital for the country’s near-term needs and long-term productivity growth.”

But while the CPA is getting more pessimistic about the health of the UK construction industry, other indicators emphasise its resilience. Over the first half of the year the monthly survey of construction purchasing managers has shown them to be marginally more positive than negative, with an average Purchasing Managers’ Index (PMI) score of 50.9 so far this year. Anything over 50 indicates growth. If the CPA is right, and the PMI is an accurate barometer, expect to see that barometer plummet in the coming months. If it does not, some economists somewhere have got it wrong again.

Got a story? Email news@theconstructionindex.co.uk