The problem is less about the lack of supply, it seems, and more about the excess demand.

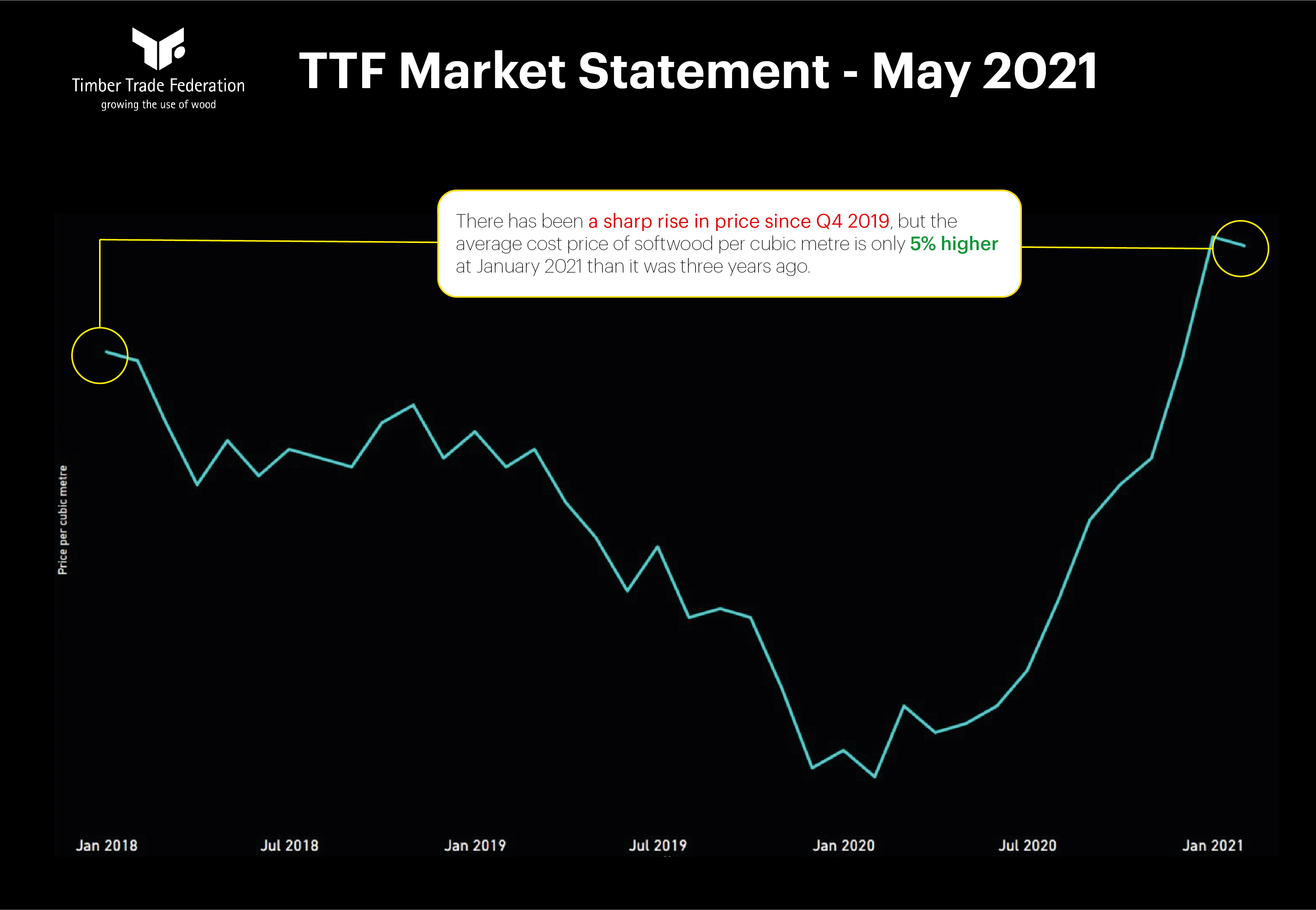

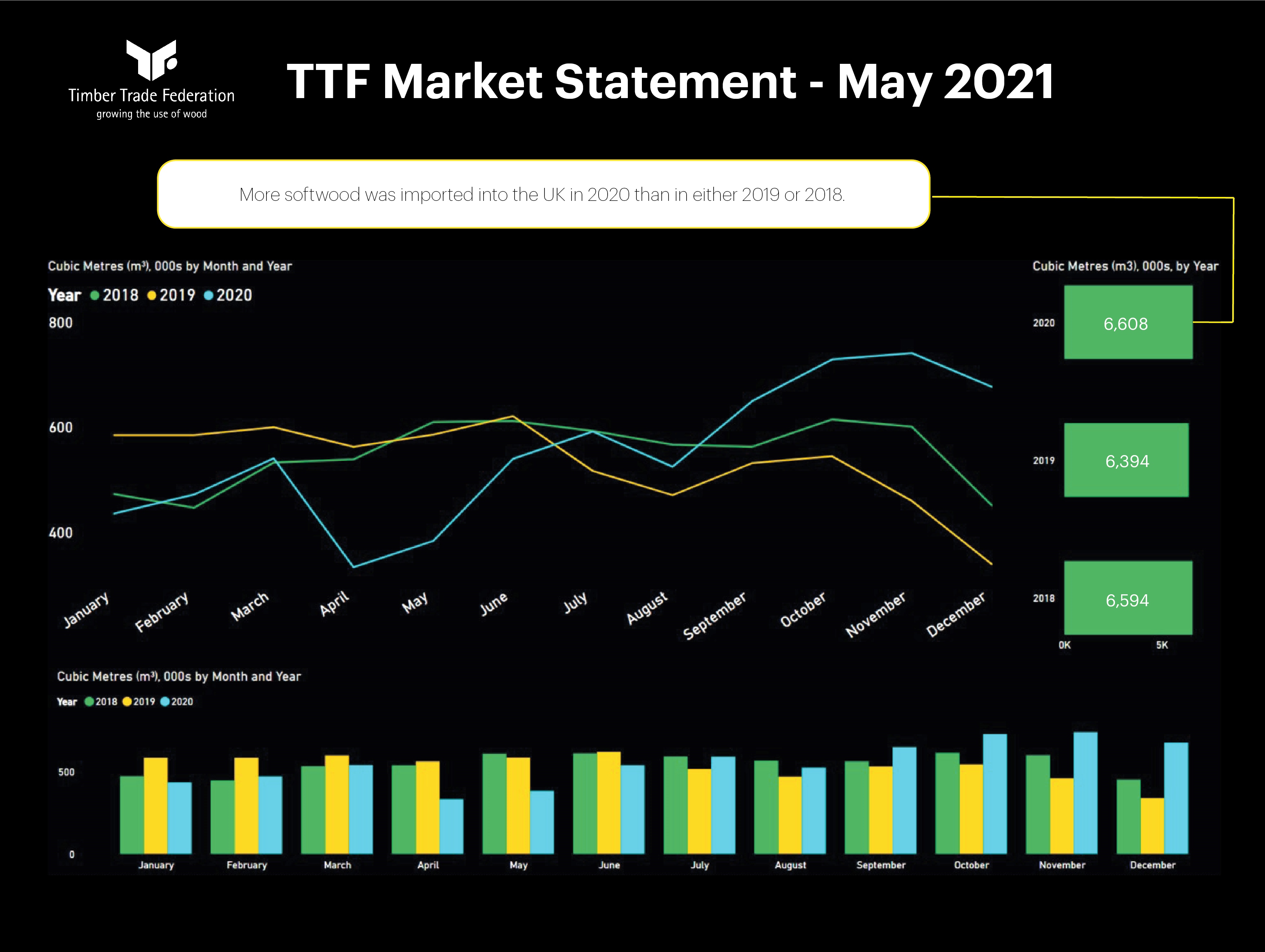

Timber Trade Federation (TTF) statistics show more softwood was imported into the UK in 2020 than in either 2019 or 2018. And while the price has risen sharply in the past year, it is actually still only 5% higher than it was three years ago.

However, shortages are set to continue for the foreseeable future and prices are set to rise further.

TTF chief executive David Hopkins said: “We hope by sharing this information it may help our members in their conversations and business activity by placing our current situation into a wider context. In our view the market position should be phrased as a demand rather than as a supply situation. Timber is still being imported and produced at high volumes. However, the surge in demand for construction materials this year means customers may not be able to purchase timber as readily off the shelves as they have been used to.

“We advise users of timber to work closely with suppliers on their purchasing strategies, and to take a forward-looking perspective on securing supplies. This approach will remain important, as recent reports have shown we can expect demand to continue to be high, particularly for structural and other softwood materials. We also know that traditionally sawmills in Europe normally enter a period of shut-down for repair, maintenance and holidays in June and July, and this will keep supply tight.”

Timber Trade Federation Market Statement May 2021

Where are we now?

Timber is still being imported and produced in the UK; customers with forward purchasing strategies are receiving their materials. Regular dialogue on forward requirements is encouraged between purchasers and their suppliers, wherever they sit in the supply chain.

Due to pandemic-driven factors and high domestic and international demand, the formerly-abundant stock levels enjoyed by buyers in the UK have not been able to be re-built since the beginning of the pandemic in 2020.

Supply will tighten as 2021 progresses: sawmills in Europe normally enter a period of shut-down for repair, maintenance and holidays in June/July. Demand continues to be high, particularly for structural and other softwood materials, panel products and hardwoods, across the world. This will exacerbate the supply situation.

Across the globe, lockdowns and the consequent move to home-based working have altered market dynamics: unprecedented international demand continues for house-building, DIY projects, garden improvements, home extensions, home offices and other refurbishments.

House-building in the UK was initially shut down by the pandemic in 2020 and is now moving swiftly to catch up, further pressuring supplies. Government emphasis on revival in construction as a lead into expanding the economy is also influencing the demand curve.

Exceptionally high global demand for timber, as its carbon storage potential in construction is grasped and embraced across construction, combined with supply pipeline restrictions, are motivating pricing upwards: demand is outstripping current production capacity.

Other countries internationally are prepared to pay higher prices than traditionally agreed by UK timber purchasers, heightening the perception of value. UK-grown timber supplies are insufficient to replace the level of imported timber demanded by UK construction and refurbishment.

Brexit-related factors are also affecting the ability of importers to import. Around 80% of the softwood used in Britain’s building, fit-out and refurbishment sectors comes in from countries in the European Union and further afield on the Continent. This rises to around 90% in new-build housing.

How did we get here? Timber in 2020

Prior to 2020, the two abortive attempts at Brexit had seen both suppliers and wood users respond to uncertainty by stock-piling large volumes of timber and wood products in case of disruption. This created artificially-high stock availability. As each attempt at Brexit failed, it created artificially-low pricing, reflecting the extreme over-supply in the marketplace, which then passed through the supply chain.

Pre-pandemic, UK wood buyers, from major house-builders to householders, benefitted from abundantly-available supplies, available from many points along the supply chain, of which the builders’ merchant sector was just one.

Despite the pandemic-driven disruptions throughout 2020, the actual volume of softwood timber imported during 2020 was more than the total for the economically active year of 2019 (see graphic two). The market dynamics, however, changed substantially in 2020.

With the UK, Europe, the USA, China and much of the rest of the world on lockdown, furlough and/or working from home, savings gained from commuting to work, and the need for better domestic spaces, created with unprecedented demand for timber for DIY projects and home/garden refurbishments.

Initial COVID-forced shutdowns in some European sawmills, combined with a high global demand for timber in general, meant that normally-abundant stocks on the ground here in Britain could not be re-built.

Unprecedented demand continued throughout winter 2020 – a time at which companies would normally replenish stocks for the new building season following on in spring. This replenishment was not able to take place. Though material was coming into the UK regularly,

By the end of 2020, no unsold stock existed in Britain: a situation never before seen in the trade. Those customers with forward planning and purchasing strategies were able to receive their materials, thus much of the major housebuilding sector was still able to function, despite the massive uplift in demand.

Those less able to hold stocks or less willing to plan their needs in advance were unable to spot-purchase quantities: this was a particular problem for builders’ merchants, whose purchasing strategies and stock-holding patterns have only now begun to adapt to the new reality.

What lies ahead? Timber in 2021

By the last quarter of 2020, imports of timber were already reaching record levels and there was no unsold stock in the UK. Imports continued at record levels through Q1, 2021, with all stock presold on customer allocations.

Timber suppliers are doing their best to service customers but the level of demand is currently higher than can be swiftly gratified by existing production facilities and available input supplies across the UK and Europe. This applies to both timber and panel products.

The Builders Merchants Building Index (BMBI) showed sales of timber & joinery products up over 18% in January 2021 compared to January 2020. Indicating the continuing strength of domestic refurbishment and building demand.

House-builders continue to ramp up work on site. The value of construction projects (under £100m) starting on site in the three months to April 2021 was 30% higher than the same period last year, according to industry analysts Glenigan. The Federation of Master Builders’ Q1 State of the Trade report shows the fastest rise in enquiries for 10 years; repair, maintenance and refurbishment work is seeing the strongest revival. These factors in turn impact demand and thus supply.

Some timber-producing countries traditionally supplying the UK have instituted log export bans, which puts additional pressure on supplies. The Republic of Ireland, the nearest supplier to Britain, is having its own internal difficulties over log harvesting, impacting the UK construction supply chain. Higher log prices are already being paid by sawmills at home and abroad; higher costs are then passed through national and international supply chains.

Brexit-related issues, including logistics, will continue to play a part in supply problems while difficulties with due diligence paperwork and new plant health requirements, plus the situation with movements to and from Northern Ireland continue unabated. All these factors contribute to making it more difficult to import timber products in order to fulfil demand.

The Timber Trade Federation’s UK Softwood Conference in March revealed that softwood demand is forecast to increase worldwide at least until 2025, and will likely continue upwards for some years to come. The situation for buyers, both on upward price trajectories and on tight supplies, is thus unlikely to change at any time in the near future.

Swedish Wood

Swedish Wood, which represents the Swedish sawmill industry and is part of the Swedish Forest Industries Federation, has also commented on the issue of shortages.

It attributed the global shortage of wood products to lower production in other parts of the world. Several wood product manufacturers that usually have high output, temporarily scaled back their activity in 2020, leading to a major shortfall in the international market.

It said that Swedish sawmills were able to keep production going during the Covid-19 pandemic but increasing demand for wood products globally had seen stocks at the

Swedish sawmills run down to their lowest stock levels for more than 20 years. Production is continuing at full throttle and March became the best production month ever for the Swedish sawmill industry.

Got a story? Email news@theconstructionindex.co.uk