Ever since economic growth returned in 2012, pundits have been warning of a false dawn, pointing out that while activity has been increasing, productivity has stagnated. On several occasions in this very publication we have reported a guarded appraisal of positive business trends, often with the caveat that a slowdown is likely to be just around the corner.

No such hedge-betting is required when assessing the state of the demolition industry, though. Last year’s summary of the performance of the UK’s top 20 demolition contractors showed robust business across the board, despite some mild misgivings concerning the low price of scrap – an essential string to any demolition specialist’s bow.

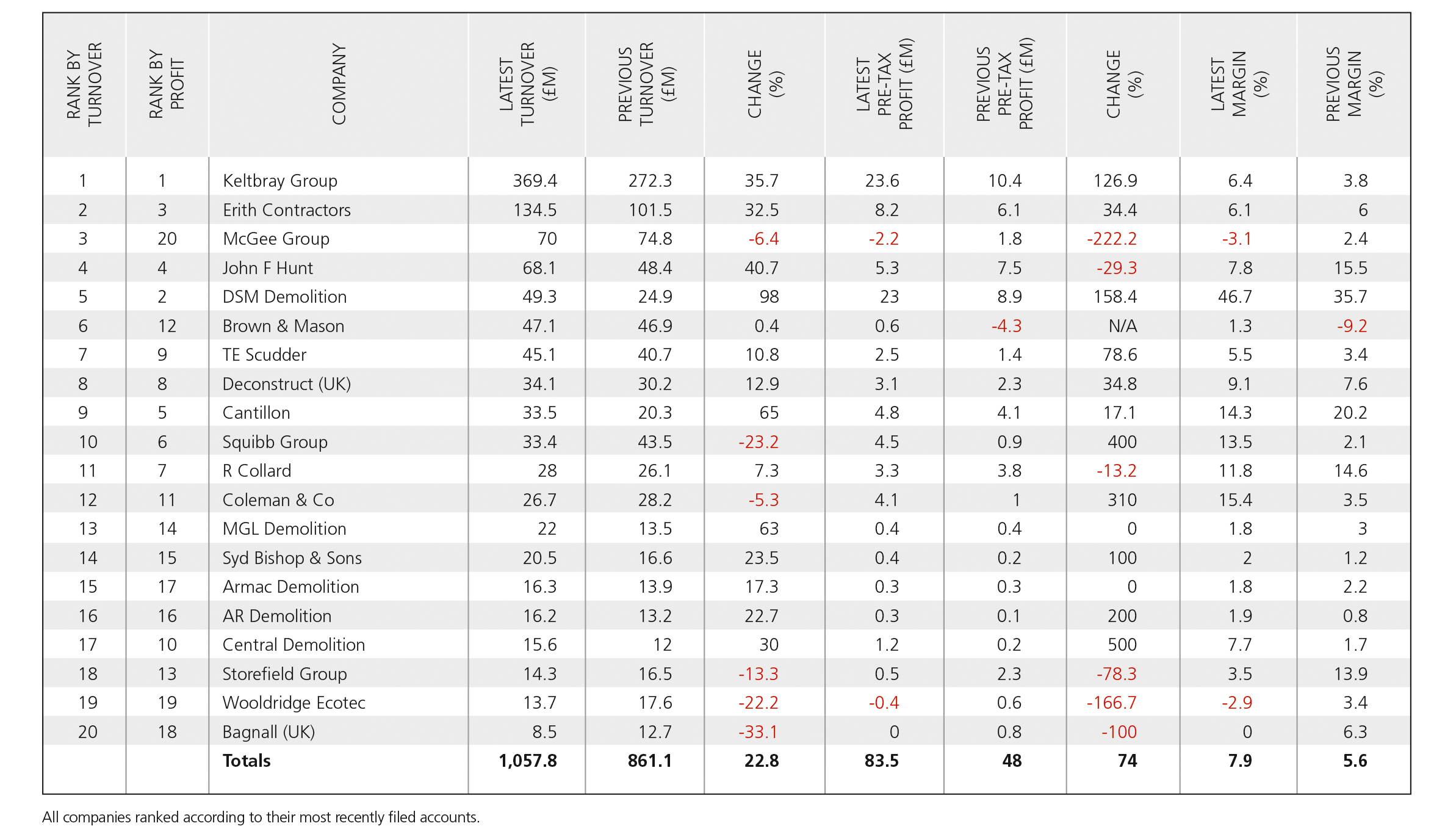

Back then we recorded a near 25% increase in collective turnover for the top 20 demolition firms in the year 2015/16. This year it’s the same story: revenue earned by the 20 biggest contractors once again rose by almost 23% and broke through the £1bn barrier for the first time.

And they’re not just a bunch of busy fools, either. Overall profitability has improved immensely, up 74% with average margins of 7.9% (2016: 5.6%).

As ever, some companies have performed extremely well; others less so. Six of the 20 firms have seen turnover fall while seven recorded a reduction in pre-tax profits. However, only two actually made a pre-tax loss.

All the figures reproduced here are taken from each company’s most recent annual results filed at Companies House and cover a trading period from June 2015 to November 2016.

Most of the annual reports have something to say about the impact of the Brexit vote in June 2016, many of them noting a slowdown in orders during the build-up to the referendum and a tentative return of confidence in the months following the result. Not surprisingly, given the agonising progress of ongoing Brexit negotiations, some uncertainty remains on this score.

Keltbray remains at the top of the list with a substantial lead over its nearest competitors. Group turnover for the year to 31st October 2016 was up 35.7% to £369.4m and pre-tax profit surged ahead to £23.6m, a more than 125% increase on 2015’s figure of £10.4m.

The secret of Keltbray’s recent success appears to be its strategic diversification into new sectors. Since its acquisition by chief executive Brendan Kerr in 2003, the company has grown from a £22m demolition company into a £370m leading specialist, providing engineering, construction, demolition, decommissioning, remediation, rail and environmental services across the country.

Keltbray has recently branched out into contract lifting services and has greatly increased its piling activities. In August 2016 the company became a significant player in the concrete structures sector, having acquired the assets of Dunne Building & Civil Engineering, a major reinforced concrete specialist.

Keltbray now comprises four divisions: demolition & civils, rail, environmental materials management, and services. Even when the latter three divisions are factored-out, the demolition & civils division remains the dominant UK demolition contractor with £248m of revenue in 2016.

Trailing Keltbray in second place is Erith which also put in a sold performance in 2016. Turnover increased by more than 30% (to £134.5m) and Erith made pre-tax profit of £8.2m, a margin of 6.1%. Company secretary Steve Darsey commented that the market for demolition remains highly competitive with smaller businesses fostering strong local reputations and larger PLCs competing on price.

Although McGee rose one place in the rankings this year – pushing John F Hunt into fourth position – 2016 was not a good year for the business. Turnover actually fell slightly, to £70m from £74.8m in 2015, and McGee was one of only two companies in the top 20 this year to make a pre-tax loss.

While the parent company, McGee Group Holdings, reported record results for the year (turnover up almost 25% to £125m and profit doubling) the demolition division put in a decidedly lacklustre performance, making a pre-tax loss of £2.2m on its reduced turnover.

Brexit remains an unknown quantity for the McGee board, which said: “On the one hand there is evidence of a reduced flow of projects as clients reappraise their plans in the context of Brexit, whilst on the other a weakened currency increases the attractiveness of sterling investments”.

John F Hunt, meanwhile, might have slipped a place in the rankings this year, but it still managed to increase revenues by more than 40% to £68.1m. Profitability suffered somewhat, falling 30%, but Hunt was still in the black with a pre-tax profit of £5.3m.

The company says that the Brexit vote temporarily put a brake on business enquiries but that the directors are “confident that

with the expansion of activities both by discipline and geographical location the UK construction sector will provide significant opportunities for the group.”

Birmingham-based DSM Demolition had a very good 2016, almost doubling turnover to £68.1m (2015: £24.9m) and boosting pre-tax profits by 158%. In fact, DSM’s £23m pre-tax profit is the largest of our entire selection with the exception of Keltbray’s £23.6m – and on little more than one-eighth of the latter’s turnover. These results take DSM up the table to fifth place from number 11 last year.

Just one month after DSM filed its annual report it was announced that the Kelly family, which owned the business, had sold out to a management team backed by investor Metric Capital Partners.

The business has now been merged with brownfield land developer St Francis Group. The new owners believe that the combined businesses have a “clear competitive edge”, with DSM’s technical remediation capability and St Francis’ planning expertise combining to allow the group to “unlock the value of purchased land assets”.

In contrast to DSM’s sparkling performance, Storefield Group, Wooldridge Ecotec and Bagnall languish at the bottom of the table with significant reductions in both turnover and profit margin.

Storefield recorded turnover down just over 13% but managed to scrape a pre-tax profit of half a million (from £2.3m last year). Bagnall broke even on a turnover down 33% to £8.5m from £12.7m last year. And Wooldridge – the only other loss-maker apart from McGee this year – lost £387,248 before tax on a turnover of just under £14m. The previous year the company had made a pre-tax profit of £600,000 on revenues of over £17.5m.

Meanwhile, sitting in the middle of the table at number 10, Squibb Group congratulated itself on “a robust set of results” that saw it deliver £4.5m of pre-tax profit – up from less than £1m the previous year – on a reduced turnover of £33.4m (2015: £43.5m).

The company might have slipped five places on our table, but in terms of financial security, Squibb is looking very comfortable. “Tight cost control” has been a priority, say the directors, and has been instrumental in the improved profit figure.

Squibb says it started the current financial year with “a strong pipeline of projects and contractual entitlements to scrap with a value of in excess of circa £10m”. In this, the company is typical of the sector. Even those that saw turnover and profits falter in 2016 seem undaunted and nearly all report a very healthy volume of work for the current financial year.

This article was first published in the April 2018 issue of The Construction Index magazine, which you can read for free at http://epublishing.theconstructionindex.co.uk/magazine/april2018/

UK readers can have their own copy of the magazine, in real paper, posted through their letterbox each month by taking out an annual subscription for just £50 a year. See www.theconstructionindex.co.uk/magazine for details.

Got a story? Email news@theconstructionindex.co.uk

.gif)