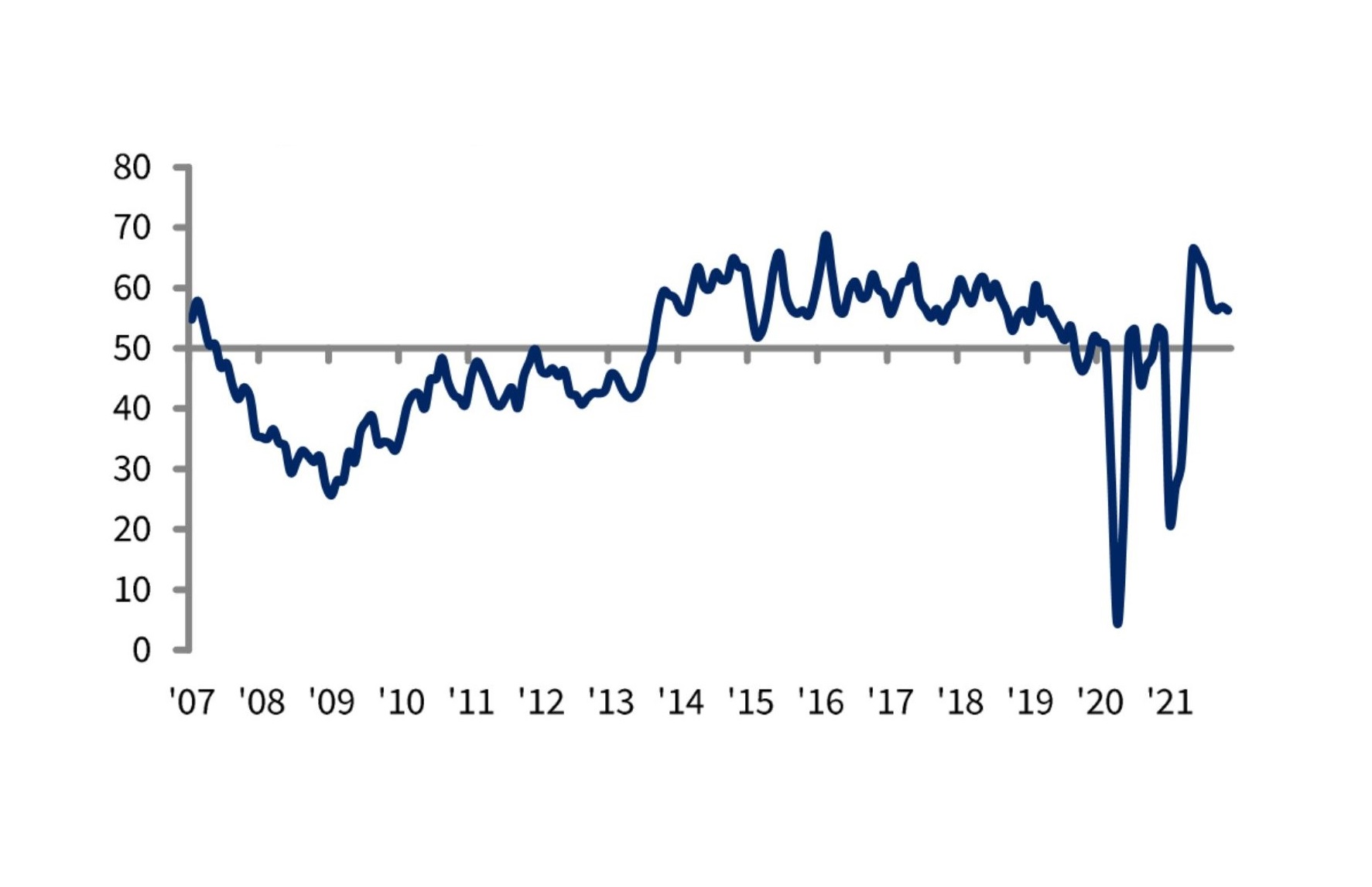

The Ulster Bank Construction Purchasing Managers’ Index (PMI) – a seasonally adjusted index designed to track changes in total construction activity – posted 56.3 in November, down marginally from 56.9 in October but still indicative of a sharp monthly increase in total activity. The latest rise was the seventh in as many months. Index readings above 50 signal an increase in activity on the previous month and readings below 50 signal a decrease.

Simon Barry, chief economist Republic of Ireland at Ulster Bank, said: “The recent quarterly national accounts from the Central Statistics Office indicated that construction was one of the fastest-growing sectors of the Irish economy in the third quarter of this year. The latest results of the Ulster Bank Construction PMI survey highlight that construction firms have continued to experience strong growth through the middle of the fourth quarter. The headline PMI eased slightly in November, but at 56.3 remains at elevated levels consistent with a strong pace of activity expansion, albeit one which has decelerated from the exceptional, post-lockdown snap-back growth registered earlier in the year. The pace of growth moderated somewhat from a very rapid pace in commercial activity, while housing and civil engineering both registered improvement last month to leave all three sub-sectors in expansion territory.

“The overall sector’s ongoing recovery momentum was again evident in very healthy readings in employment and new orders, both of which recorded accelerating growth in November which resulted in a three-month high in each case. Growth in new business was partly linked to opportunities across the housing, healthcare and renewable energy areas.

“However, the November results again make clear that the sector continues to face highly testing supply-chain challenges linked to a variety of factors which continue to result in delivery delays and marked input cost pressures, including the pandemic, Brexit, higher global and domestic prices for energy and other materials and rising freight charges. And yet there was just a hint that the intensity of supply-chain disruptions may be easing a little as input price inflation and the pace of lengthening of supplier lead times eased to the weakest in six and seven months respectively.”

For the first time in four months, all three monitored categories of construction posted increases in activity as civil engineering returned to growth. In fact, civil engineering posted the fastest expansion of the three categories in November. Nonetheless, rates of growth in housing and commercial activity remained marked.

In line with the picture for activity, improving demand resulted in higher new orders midway through the final quarter of the year. Among the projects secured were those for work on housing, hospitals and renewable energy.

Construction firms responded to higher workloads by expanding their staffing levels for the eighth month running, with the marked pace of job creation the sharpest since August.

There was little sign of respite for firms trying to purchase inputs in terms of supply-chain disruption. Delivery times continued to lengthen substantially amid pressure on supplier capacity and delays caused by the Covid-19 pandemic and Brexit.

In turn, input costs continued to rise at a considerable pace in November, and one that was only slightly weaker than the series record posted in October. A range of factors reportedly added to inflationary pressures, including higher material costs, rising freight charges and Brexit. Firms also indicated that the carbon tax had contributed to higher input prices. Close to 68% of respondents indicated that their input costs had risen over the month.

Companies remained optimistic that activity will continue to rise over the coming year. Although sentiment dipped from the previous month, it remained above the series average as close to 45% of panellists predicted an expansion in activity. Expectations of further improvements in customer demand were central to hopes for growth of activity.

Got a story? Email news@theconstructionindex.co.uk