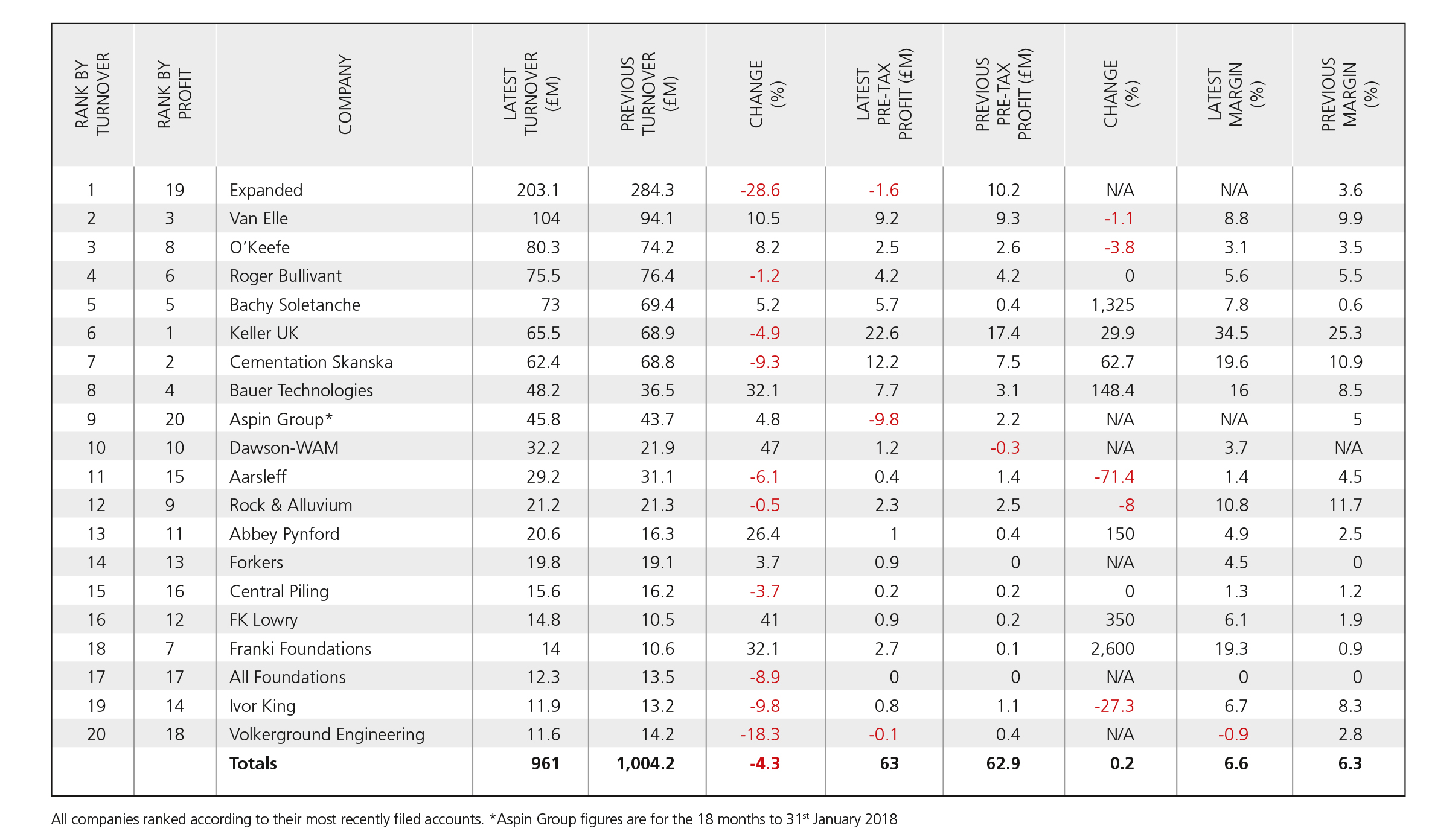

Last year’s analysis of the 20 leading piling and ground engineering specialists detected a slowdown in the rate of growth; this year, we can see an actual reversal. For the first time since we began tracking the fortunes of the sector, workloads have fallen.

In 2016/17, the top 20 piling firms notched up a total collective revenue of just over £1bn. They have been unable to sustain that, however, and that figure has since fallen back below the £1bn threshold – down 4.3% to £961m.

This decline is due in no small part to the poor performance of the sector’s leading player, Laing O’Rourke subsidiary Expanded. Still by far the largest business in the UK piling sector (and twice the size of its nearest competitor, Van Elle) Expanded saw turnover fall by almost 30%, from £284.3m to £203.1m, in the 12 months to March 2018.

“The directors are disappointed with the financial result for the year but expect the company to return to profitability in the future,” said the company in its financial report for 2017/18.

While Expanded is listed as a separate business, its parent company, Laing O’Rourke, doesn’t like to comment on the performance of specific business units. Instead, the directors “believe that analysis of the company’s risks should be viewed in the context of the Group”.

Looking at group performance, then, Laing O’Rourke reported a loss of £60.6m after tax during the year to March 2018. It was late filing its financial results due to problems refinancing – provoking fears among clients and staff of a possible Carillion-like crash.

That didn’t happen and, in fact, the £60.6m loss came as a relief after the previous year’s loss of £219.9m.

Laing O’Rourke has not registered a profit for several years. It reported a pre-tax loss of £81m in the year to 31st March 2017, a loss of £267m in fiscal 2016 and a loss of £59m in fiscal 2015.

Expanded, on the other hand, had a good 2016/17 and made a pre-tax profit of £10.2m. Exactly what led to the slump in turnover and the £1.6m loss in 2017/18 is not clear.

Van Elle, the UK’s second-largest piling contractor, has also had an interesting

couple of years (for a full commentary, see the feature on page 41 of this issue). But despite boardroom upheavals and shareholder rebellions, the business filed very acceptable financial results for the year ending 30th April 2018.

Turnover was up 10.5% to £104m (2017: £94.1m) and pre-tax profit remained more or less static at £9.2m. In its strategic report, Van Elle admitted that 2017/18 had been a “difficult” year despite a good overall performance in the first half. The collapse of Carillion – a major client – and poor weather in early 2018 were the main culprits, said the company.

Another leading contractor with an interesting recent history is Cementation Skanska. Despite being a famous name in the sector with an illustrious track record to commend it, Cementation is not wanted by its parent company and has had difficulty finding anybody willing to take it on.

Skanska put the business up for sale in May 2018 and it is thought to be up for sale still after a deal with concrete frame contractor Morrisroe fell through earlier this year. Morrisroe is understood to have considered the £55m asking price to be too high.

Meanwhile, as we report on page 37 of this issue, key Cementation personnel have decided to get out and pursue opportunities with rival contractors. Shane Baker, who ran Cementation’s London projects is now head of piling at McGee; he is joined by former Cementation colleagues Julian Mansfield and Darren Smallman.

Of course, none of this is discussed in Cementation’s financial report for the 12 months to 31st December 2018, filed at Companies House in March this year. The company says that it “continued to invest in the business during the year to ensure that it continues to build upon its place in the piling, foundations and ground engineering market”.

The figures themselves shouldn’t look too discouraging to any potential buyers: although turnover was down 9.3% to £62.4m (2017: £68.8) the business recorded pre-tax profits up more than 60% to £12.2m (2017: £7.5m) – a pre-tax profit margin of almost 20%.

If it’s margin you’re interested in, look no further than Keller UK. With a pre-tax profit of £22.6m for the year to 31st December 2017, Keller takes the number one spot for profitability. Pre-tax profit margin is an impressive 34.5%.

There are, of course, exceptional reasons for this. Keller UK (the UK operation of Keller Group, the world’s biggest piling specialist with an annual turnover of more than £2bn) actually registered an operating profit of £2m on a turnover of £65.5m in 2017. But that was before exceptional items:

“An exceptional credit of £16.7m arose as a further part reversal of a £54m exceptional charge taken in 2014 for a contract dispute relating to a project completed in 2008. The project was in connection with the construction of a major warehouse and processing facility in Avonmouth, near Bristol,” explained Keller.

As part of the settlement agreement, Keller subsequently bought the property in May 2016 for £65m, selling it for the same price a year later. “The sale therefore realised an exceptional profit before cost of £8m,” said Keller.

Although growth rates fluctuate in every industry sector due to the interaction of various economic factors, it is seldom that our sector analysis detects an actual reduction in workloads year-on-year.

But in April this year we saw the combined turnover of the top 20 demolition specialists level-off at just over £1bn (our figures actually showed a marginal 0.3% reduction) as growth stagnated.

A 4.3% fall in revenues is not marginal, though. Piling contractors are among the first to start work on any project and if they are seeing workloads falter, following trades are likely to feel the effect further down the line.

Contract awards, chronicled every month in this magazine, have been riding high for over a year in defiance of expectations. But as the Builders’ Conference CEO Neil Edwards reports in his commentary to this month’s Contracts League, there are signs of potential storms ahead.

And when activity in the piling and foundations sector starts to fall, it’s a sign to sit up and take notice.

This article was first published in the June 2019 issue of The Construction Index magazine

UK readers can have their own copy of the magazine, in real paper, posted through their letterbox each month by taking out an annual subscription for just £50 a year. Click for details.

Got a story? Email news@theconstructionindex.co.uk