The construction industry continues to climb steadily out of the slough of recessionary despond, with the latest update by the Office of National Statistics to its initial Q4 2013 estimates suggesting that output had risen by a slender 0.2% compared with the previous quarter, confounding expectations of a fall.

For the whole of 2013, output rose by £1.5bn or 1.3%, entirely driven by new work rather than repair and maintenance. Added evidence of expansion has come from the Mineral Products Association statistics for 2013, showing single digit volume growth for aggregates and asphalt, while concrete sales were up 11%.

Within new work, the overwhelmingly dominant driver was house building, which soared by a startling 10.4% year on year. One after the other, the listed house builders have been reporting significantly increased profits, the most recent being Bellway off the back of unit volumes rising by 25% and average selling prices escalating 13%. For them as well as their competitors, much of the boost has come from the Help to Buy Scheme, over which there is increasing uncertainty because of the distortion it is creating in the housing market just as the 2015 General Election starts to dominate political thought and debate.

Alongside the growth in revenues and aside from the profit windfalls enjoyed by the house builders, there is increasing evidence that ‘busy fool’ syndrome is beginning to bite into contractors’ profitability. The most recent example is Morgan Sindall which maintained revenues, but saw profits tumble by 59%. Overly competitive pricing has always been an issue in the industry, but the factors now squeezing margins are the rising input costs for materials and labour. It seems doubly ironic that there is simultaneously a shortage of both bricks and bricklayers.

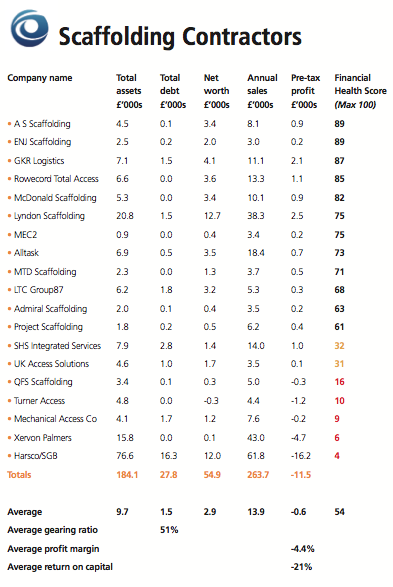

The companies we have analysed for this month’s report are those scaffolding contractors with turnover of £3m or more in their latest published accounts. Companies House records show that there are 1,816 UK-registered companies claiming that their principal activity is scaffolding-related. Even setting the turnover cut-off point as low as £3m still only produced a sample of just 19 companies, which confirms the highly fragmented nature of this sub-sector.

Within this meagre population, one company stands out: Harsco Infrastructure Services, previously part of the Harsco Corporation and operator of the SGB scaffolding brand in the UK. Its operations here have suffered severe commercial difficulties over a number of years, as highlighted in its December 2012 accounts. In September 2013 Harsco spun out its infrastructure businesses into a new joint venture entity, Brand Energy & Infrastructure Services.

Harsco Infrastructure declared a pre-tax loss for 2012 of £32.3m, which included exceptional restructuring costs and goodwill impairment charges totalling £16.1m, leaving an operating loss of £16.2m, which is the figure we have used for our analysis. Unfortunately, this scale of loss dwarfs the results of the remainder of the larger scaffolding contractors. Throughout this review, we quote the relevant sector statistics both including and excluding Harsco to provide clarity on the true financial state of the sector. Unfortunately, it is not possible to ignore the performance of Harsco/SGB, since it is a significant part of the scaffolding industry in the UK.

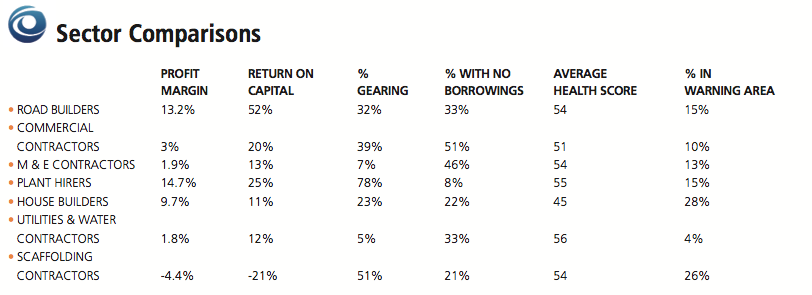

The Company Watch research shows a level of profitability for the sector of 2.3% excluding Harsco but average losses of 4.4% including it. Without Harsco, the scaffolding sector is broadly in line with other sub-sectors such as commercial builders (3%), M&E contractors (2%) and those specialising in the utilities and water sectors (also 2%). By contrast, it lags well below the 15% earned by plant hire companies, 13% by road builders and 10% by house builders.

The trade-off between risk and reward varies across the construction industry, particularly when profits and borrowing levels are compared. For our 19 scaffolding contractors, gearing is at 51% including Harsco and 27% excluding it. The latter number makes them more conservatively financed than plant hirers, commercial contractors and road builders, but more highly geared than house builders, M&E contractors and utilities/water contractors. Five of the companies (26%) have no external borrowings at all. The average return on capital for the sample is of course negative to the tune of 21% including Harsco, but a respectable and positive 11% without it.

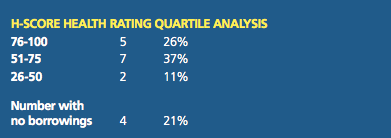

Looking next at the overall financial health of our sample, Company Watch calculates a health rating (H-Score) for every UK company, based on the interaction between seven key financial ratios involving profitability, funding and asset management. These are extracted from published financial information and processed through a mathematical model which compares this data with the characteristics of companies that fail and those that survive. This produces an H-Score out of a maximum of 100. Scores between 76 and 100 are in the financial Premier League. Between 51 and 75 is more akin to Championship form. A score between 26 and 50 indicates a company which is financially off colour.

Those that cause concern have scores of 25 or below, which is the Company Watch warning area indicating abnormal financial vulnerability. Over the past 15 years, a very high percentage of UK companies which filed for insolvency or underwent a financial restructuring were in this warning area of 25 or below at the time. Not every company in this red zone fails, because of remedial management action, but it is a clear indication of heightened financial risk for their clients, suppliers and service providers alike.

Looking at the profile of the 19 scaffolding contractors on this measure, their average H-Score is 54, which is significantly above the norm of 45 for all UK companies of similar size. The relatively low levels of debt play a part in this outcome, as does there being only one company with negative net worth (liabilities greater than assets). This ranks below two of the other six sub-sectors we have analysed previously for The Construction Index and alongside two others.

Five of the sample (26%) are in the Company Watch warning area, the second worst outcome so far on this test. Across the economy as a whole, the expectation would be that around 25% of any sample would be in this financial twilight zone. Looking at the better performers, 63% of the sample have H-Scores of 51 and above, as compared to around 50% for all UK companies. As noted above, only one company has negative net worth, but five including Harsco are loss-making.

Harsco apart, the results of our research are modestly encouraging, especially in terms of overall financial strength. But it is worth repeating yet again the comments from our previous reports that our figures cover only the few major players out of a market which also features thousands of smaller, generally undercapitalised and almost exclusively family-owned SMEs, either companies or the host of unincorporated sole traders.

Many spend their time dealing with the negative financial implications of operating within potentially abusive relationships as subcontractors to more powerful and far bigger main contractors. Much more caution is needed about their finances.

One of the realities of any growth phase after a recession is that insolvencies have peaked after every major recession for the past 40 years somewhere between 15 and 18 months after sustained recovery takes hold, as it now seems to have done at last. The counter-intuitive reason is that having burnt through their reserves during the recession, survivor companies then struggle to raise the extra working capital they need to fund increased sales and investment as things pick up.

This effect is likely to be particularly marked as we move into the middle of 2014, because crucially the financial services sector has taken such a severe hammering from the recession and its own mis-selling excesses. Many banks and other lenders are still busy repairing their own balance sheets. Put simply, they have less money to lend and will be far choosier about who they will help to expand, which is bad news for small subcontractors.

But overall, the short to medium term prospects for scaffolding contractors seem likely to be more curates’ egg than the smell of roses. The major threats are that pricing pressure will increase still further at a time when contractor margins are shrinking, while the fear is that a knee-jerk closing of the Help to Buy scheme, prompted either by the politicians or the Bank of England, may choke off the recent expansion of house building too precipitously for the financial health of many scaffolding businesses.

Got a story? Email news@theconstructionindex.co.uk