Concerns about wider economic prospects led to a drop in business confidence and slower job creation across the industry, while construction purchasing activity declined.

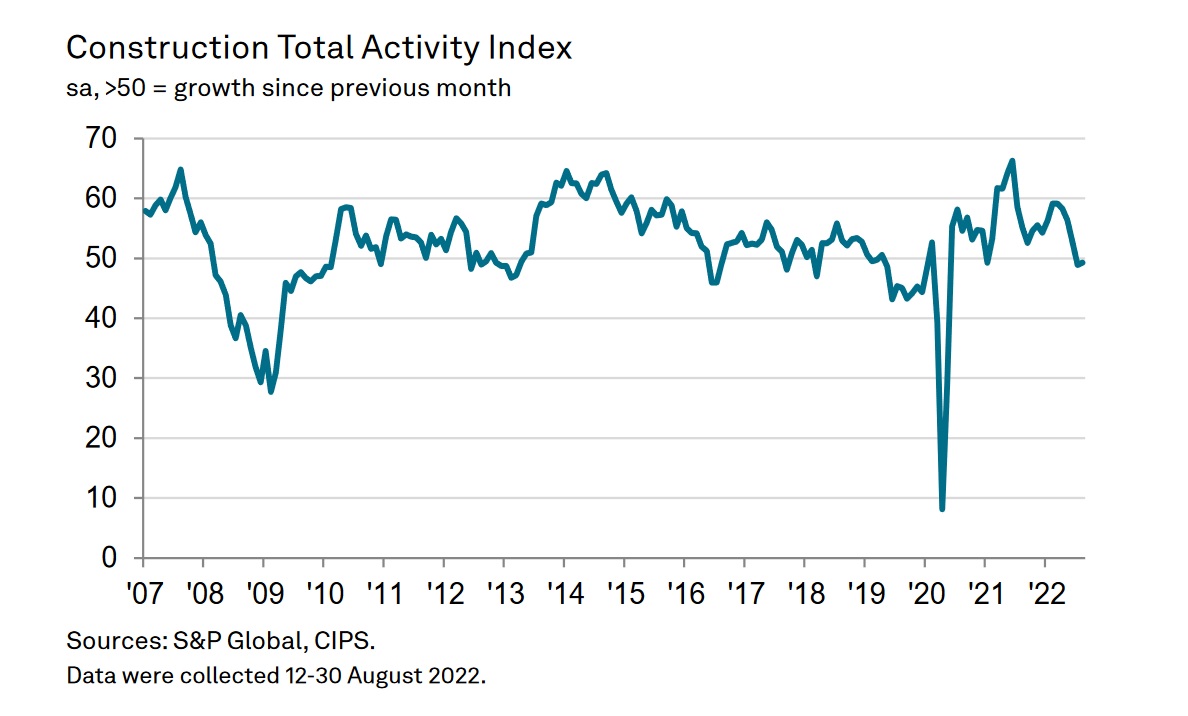

The headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) – which measures month-on-month changes in industry activity – was at 49.2 in August, up fractionally from 48.9 in July but still below the 50.0 no-change mark and thus signalling a reduction in construction activity over the month. Activity has now decreased in two consecutive months.

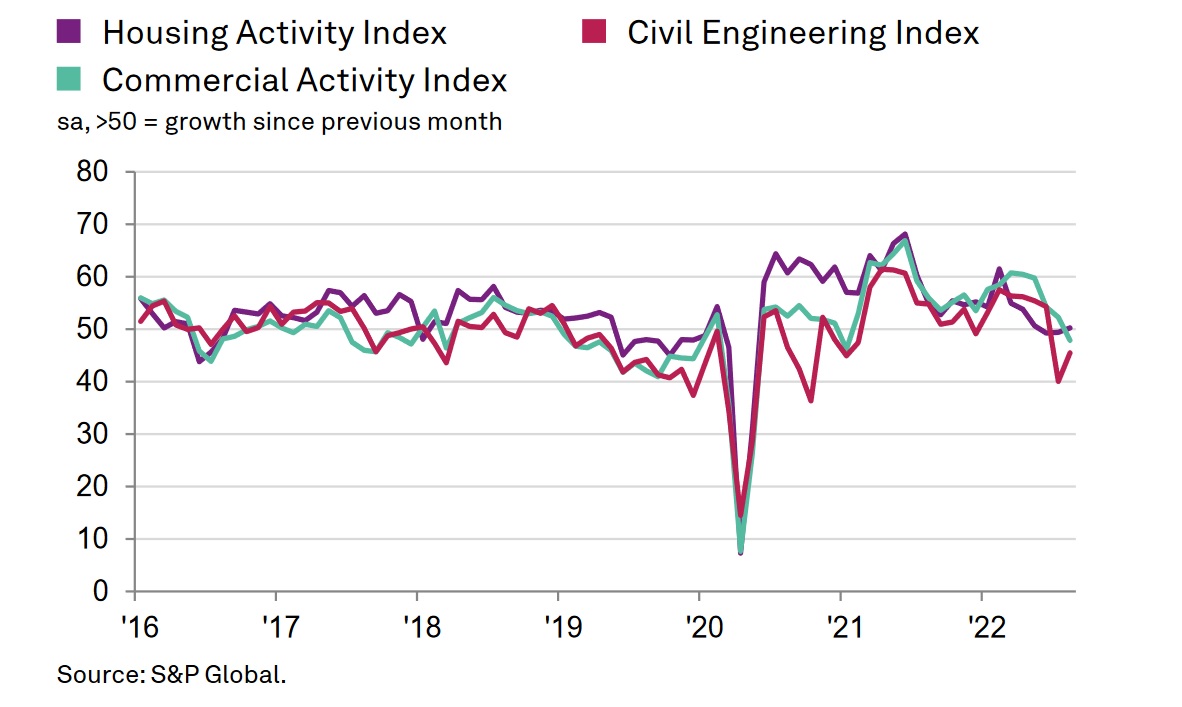

As was the case in July, civil engineering posted the sharpest decline in activity of the three broad categories, seeing output fall markedly over the month, but its decline in August was not as steep as it had been in July (see second graph below). Commercial activity also declined, thereby ending a period of growth stretching back for a year-and-a-half. On a more positive note, activity on housing projects increased for the first time in three months month-on – but only just.

New orders increased marginally in August, and to the least extent since June 2020. Respondents indicated that customers were holding back on committing to new orders amid cost pressures. While some firms increased activity in response to ongoing growth of new orders, this was outweighed by those that saw output decline as firms adjusted to signs of demand weakening.

Alongside inflationary pressures, concerns around the potential for a wider economic downturn also impacted the sector in August. Business confidence dropped in July and was well below the series average.

In some cases, concerns around the wider economic environment impacted hiring decisions. Although rising new orders, the clearing of backlogged work and the filling of previously vacant positions kept employment rising solidly, the rate of job creation eased to the softest since March 2021.

Construction firms scaled back their input buying for the first time since the initial wave of the covid-19 pandemic, again reflecting signs of a slowdown. There were also some reports that less pronounced price and supply pressures reduced the need to build inventories.

There were also signs of inflationary pressures moderating midway through the third quarter. Input costs continued to increase sharply, often due to higher fuel prices, but the rate of inflation softened to the weakest since February 2021. Similarly, the pace of increase in subcontractor rates also softened, and was the slowest in 16 months.

As well as scaling back purchasing and slowing the rate of job creation, construction firms kept their usage of subcontractors unchanged in August. This ended an 18-month sequence of expansion. Meanwhile, the rate of subcontractor availability continued to fall sharply, and to the largest degree in six months.

Andrew Harker, economics director at S&P Global Market Intelligence, which compiles the survey, said: "The UK construction sector looks set to be in for a challenging period, according to the latest PMI data. Not only did construction activity fall for the second month running, but a range of indicators from the survey pointed to further weakness ahead. New orders slowed to a crawl, while concerns about the sector and the wider economy led to a drop in confidence.

"Activity weakness was broad-based in August, with none of the three monitored categories immune to the wider slowdown. Commercial activity dropped into contraction for the first time in just over a year-and-a-half, and while housing activity ticked higher, the segment has been in broad stagnation over the past three months.

"Price and supply pressures showed further signs of easing as waning demand throughout the sector lifted pressure on suppliers. Meanwhile, the main positive from the latest survey was a solid increase in employment. That said, hiring at least in part reflects an ongoing catch-up following the pandemic. If activity continues to fall, firms will likely soon feel that their staffing capacity is sufficient and pause hiring."

Dr John Glen, chief economist at the Chartered Institute of Procurement & Supply, said: "The UK construction sector is poised for contraction once again as rising prices for raw materials worldwide filtered into UK supply chains. Just 14 months since the sector’s recent peak as part of the recovery from the pandemic, inflation is seeing housing and commercial building stagnate with civil engineering activity dropping significantly.

"There is some consolation for the sector as it readies itself for a future of high energy costs, however. Lower demand is leading to fewer purchases, downward pressure on input costs and more responsive supply chains. Together, these trends could eventually help to reverse inflation, but a prolonged dip in new orders will be a bitter pill for the sector to swallow."

Fraser Johns, finance director of regional construction contractor Beard, said: “Economic uncertainty both in the UK and abroad is clearly having an impact on confidence which is starting to affect the construction market.

“The positives in the data are that new orders continue to increase, if marginally, and a number of construction firms are still reporting increasing activity with a rise in the number of new orders still coming in.

“Demand for both new employees and subcontractors remains strong, while the availability of both fell sharply. This supports the importance for contractors to treat subcontractors fairly and pay them promptly, something the industry has significantly improved on in recent times.

“All firms are impacted by the continued rise in costs, and looking ahead, given the sheer scale of these cost rises we have seen, we are likely to see a softening of demand. As always strong relationships and open conversations between all stakeholders will go a long way to the industry working through the challenges we face.”

Gareth Belsham, director of the property consultancy and surveyors Naismiths, said: “As the recessionary vice begins to close on the UK economy as a whole, the construction industry’s brakes are being squeezed harder and faster than most.

“The industry has now spent two months in contraction territory, with both infrastructure and commercial property construction activity shrinking in August. House-builders provided a rare glimmer of light after residential activity ticked up for the first time in three months.

“But the flood of new orders seen at the start of the year is slowing to a trickle. New orders barely rose in August, and growth is now at the lowest level seen since the depths of the 2020 summer lockdown.

“Business confidence among construction firms, which typically provide a canary in the coalmine for the wider economy, continues to decline and August saw Britain’s builders reduce their orders for materials and scale back recruitment.

“This cooling of demand did ease some of the inflationary pressure though, and input cost inflation has now dipped to its lowest level for 18 months.

“Looking ahead, rising interest rates are likely to make some developers reassess their plans and will eventually cool demand from housebuyers too. For now, most construction firms are busy and order books remain relatively full – but the picture for 2023 is looking increasingly grim.”

Max Jones, director in Lloyds Bank’s infrastructure and construction team, said: “Despite output remaining in contraction, many larger contractors are feeling more confident than they were earlier in the year.

“Recent financial results from tier one firms showed healthy balance sheets and strong pipelines of new work. Others priced in jobs at a high point and are buying materials now as prices cool. As was the case during the pandemic, sensible balance sheet management has and will continue to be crucial.

“While there has been some relief in recent weeks on the fuel price front, a cold snap this winter could prove problematic. All eyes will be further down the supply chain. If smaller players begin to struggle to deliver work, it will fall to the rest of the industry to ensure they are supported with prompt payments and fair practices.

“The new prime minister will bring their own spending priorities, but contractors are hoping for a refocus on the government’s original objectives: the UK’s infrastructure and its net zero targets. This will give construction firms confidence to invest in their businesses and workforces.”

Federation of Master Builders chief executive Brian Berry said: “This new construction data shows that the industry has returned to its pandemic levels of activity. As the cost-of-living crisis deepens, consumers are cutting back, but builders also face increased costs on materials. This creates a difficult and clearly damaging situation. Bold solutions are required by the new government under Liz Truss. Delivering a UK wide retrofit strategy to improve the efficiency of the nation’s homes would be a huge boost for local builders and local economies alike. It would also cut homeowners bills and help ensure the UK’s energy security. More immediately we urge the government to remove VAT on repair, maintenance and improvement work so that savings can be passed on to cash strapped consumers.”

Got a story? Email news@theconstructionindex.co.uk